Get 14653 Form in PDF

Get 14653 Form in PDF

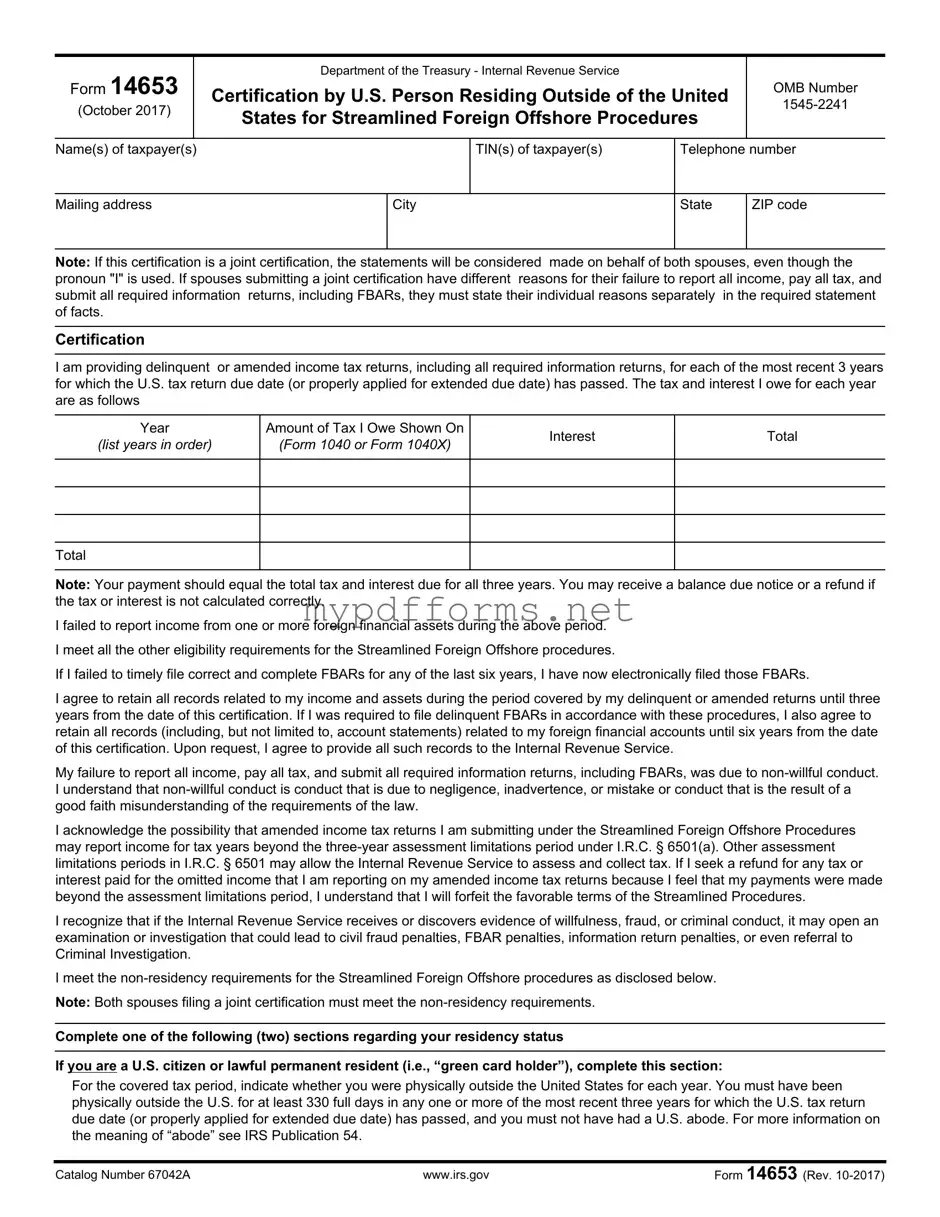

The 14653 form is a crucial document for U.S. citizens and residents living abroad who wish to rectify their tax obligations under the Streamlined Foreign Offshore Procedures. Designed by the Internal Revenue Service (IRS), this form provides a pathway for individuals who may have unintentionally failed to report foreign income or file required information returns, including Foreign Bank Account Reports (FBARs). By submitting the 14653, taxpayers can certify their compliance with tax laws while demonstrating that their previous oversights were due to non-willful conduct—such as negligence or misunderstanding. The form requires detailed personal information, including taxpayer identification numbers, contact details, and an explanation of the reasons behind any past failures to report income. Additionally, it mandates that individuals provide delinquent or amended tax returns for the previous three years, along with a comprehensive statement of facts outlining their circumstances. Importantly, both spouses must meet certain residency requirements if filing jointly, and the form also emphasizes the need to retain pertinent records for a specified duration. Understanding the implications of the 14653 form is essential, as it not only helps individuals come into compliance but also protects them from potential penalties associated with willful non-compliance.

Do's when filling out Form 14653:

Don'ts when filling out Form 14653:

Texas Temporary Tag - Use black or blue ink to fill out the form legibly.

To facilitate your transaction, be sure to review the guidelines on the accurate Maryland Trailer Bill of Sale process, which helps ensure compliance with state requirements for trailer sales.

Cash Receipt Template Pdf - Useful for maintaining trust between parties involved in transactions.

When filling out and using Form 14653, there are several important considerations to keep in mind. This form is specifically designed for U.S. persons residing outside the United States who wish to certify their eligibility for the Streamlined Foreign Offshore Procedures.

Completing Form 14653 accurately and thoroughly is vital for ensuring compliance with U.S. tax laws while seeking relief under the Streamlined Foreign Offshore Procedures. Take your time to gather all necessary information and provide a comprehensive explanation of your situation.

Filling out Form 14653 is an important step for U.S. persons residing outside the United States who want to participate in the Streamlined Foreign Offshore Procedures. This form requires careful attention to detail to ensure that all information is accurate and complete. Below are the steps to guide you through the process of completing the form.

Once you have completed the form, review it for accuracy and ensure all required attachments are included. Submitting a complete and accurate Form 14653 is crucial for your participation in the Streamlined Foreign Offshore Procedures.

Form 14653 is a certification form used by U.S. persons residing outside the United States who wish to participate in the Streamlined Foreign Offshore Procedures. This form allows individuals to certify their compliance with U.S. tax obligations while providing a streamlined process for addressing any past non-compliance.

This form is intended for U.S. citizens or lawful permanent residents (green card holders) who have failed to report income, pay taxes, or submit required information returns, including FBARs. It is specifically for those who meet the eligibility criteria for the Streamlined Foreign Offshore Procedures.

Taxpayers must provide personal information such as names, taxpayer identification numbers (TINs), and contact details. Additionally, they must disclose the years for which they are submitting delinquent or amended tax returns, the amounts of tax owed, and the interest due. A narrative statement explaining the reasons for non-compliance must also be included.

To qualify, individuals must have been physically outside the United States for at least 330 full days in one or more of the most recent three years for which the U.S. tax return due date has passed. They must not have had a U.S. abode during this period. Both spouses filing jointly must meet these non-residency requirements.

If a narrative statement explaining the failure to report income or file returns is not included, the submission will be considered incomplete. This could result in the denial of the streamlined penalty relief and may lead to further scrutiny of the taxpayer's compliance status.

If the IRS discovers evidence of willful conduct, fraud, or criminal activity, it may initiate an examination or investigation. This could lead to civil fraud penalties, FBAR penalties, or even criminal charges. It is essential to demonstrate that any failure to comply was due to non-willful conduct, such as negligence or misunderstanding of the law.

Form 1040 is the standard individual income tax return form used by U.S. taxpayers to report their annual income. Like Form 14653, it requires taxpayers to disclose their income, deductions, and tax liability. Both forms aim to ensure compliance with U.S. tax laws, although Form 1040 is used for general reporting while Form 14653 specifically addresses issues related to foreign income and the Streamlined Foreign Offshore Procedures.

Form 1040X serves as an amended U.S. individual income tax return. This form allows taxpayers to correct errors on a previously filed Form 1040. Similar to Form 14653, it requires a detailed explanation of the changes made and the reasons for those changes. Both forms emphasize the importance of accurate reporting and compliance with tax obligations.

Form 8938, Statement of Specified Foreign Financial Assets, is required for certain U.S. taxpayers to report their foreign financial assets. This form is similar to Form 14653 in that it addresses foreign income and assets, requiring detailed disclosures. Both forms aim to ensure transparency regarding foreign financial holdings and compliance with U.S. tax laws.

In considering important legal documents, it is vital to also address the implications of a Last Will and Testament. A Illinois Forms serves as a significant step in ensuring that one's wishes regarding asset distribution and dependents are formally recognized after their passing, thereby offering peace of mind to individuals and their families.

FBAR (FinCEN Form 114) is used to report foreign bank and financial accounts. It is similar to Form 14653 in that it focuses on foreign financial assets. Both forms require taxpayers to disclose information about foreign accounts and emphasize the importance of reporting foreign income to the IRS.

Form 8854, Initial and Annual Expatriation Statement, is required for U.S. citizens and long-term residents who expatriate. This form shares similarities with Form 14653 in that it involves reporting on tax obligations and foreign assets. Both forms are designed to ensure compliance with U.S. tax laws when dealing with foreign financial matters.

Form 5471 is used by U.S. citizens and residents to report information about foreign corporations in which they are shareholders. Like Form 14653, it requires detailed disclosures about foreign financial interests. Both forms aim to ensure proper reporting and compliance with U.S. tax laws related to foreign entities.

Form 8865, Return of U.S. Persons With Respect to Certain Foreign Partnerships, is similar to Form 14653 in that it requires U.S. taxpayers to report their interests in foreign partnerships. Both forms focus on foreign financial matters and require comprehensive information to ensure compliance with U.S. tax regulations.

Form 8938 and Form 1040 both require taxpayers to report their income and assets, but Form 8938 specifically targets foreign financial assets. Similar to Form 14653, it is part of the IRS's effort to ensure that U.S. taxpayers disclose all sources of income, including those from foreign accounts.

Form 3520, Annual Return to Report Transactions with Foreign Trusts and Receipt of Certain Foreign Gifts, is similar to Form 14653 in that it requires reporting of foreign financial interests. Both forms aim to ensure that U.S. taxpayers are compliant with reporting requirements related to foreign assets and income.

Form 990 is used by tax-exempt organizations to provide information about their activities, governance, and finances. While it differs in purpose, it shares a common goal with Form 14653: ensuring transparency and compliance with tax laws. Both forms require detailed disclosures to facilitate proper reporting to the IRS.

The Form 14653 is an important document for U.S. persons residing outside the United States who are seeking to rectify their tax reporting obligations under the Streamlined Foreign Offshore Procedures. However, several other forms and documents are often used in conjunction with it to ensure compliance and facilitate the process. Below are five key documents that are frequently associated with Form 14653.

Understanding these documents and their purposes can significantly ease the process of rectifying tax reporting issues for U.S. persons living abroad. Proper preparation and submission of these forms, along with Form 14653, can help ensure compliance with IRS requirements and facilitate a smoother resolution of tax obligations.

Misconceptions about Form 14653 can lead to confusion and complications in the filing process. Here are four common misconceptions explained: