Business Bill of Sale Template

Business Bill of Sale Template

The Business Bill of Sale form serves as a crucial document in the transfer of ownership for business assets, ensuring that both buyers and sellers have a clear record of the transaction. This form typically outlines key details such as the names and addresses of the parties involved, a comprehensive description of the assets being sold, and the agreed-upon purchase price. It may also include terms regarding warranties, liabilities, and any contingencies that could affect the sale. By providing a written account of the transaction, the Business Bill of Sale helps protect the interests of both parties and can serve as evidence in case of future disputes. Additionally, it often requires signatures from both the buyer and seller to validate the agreement, making it an essential part of the business transfer process. Understanding the components and significance of this form is vital for anyone engaged in buying or selling business assets, as it lays the groundwork for a smooth and legally sound transaction.

When filling out the Business Bill of Sale form, it is important to follow certain guidelines to ensure accuracy and compliance. Here are four things you should and shouldn't do:

Furniture Bill of Sale - The Furniture Bill of Sale promotes accountability in private transactions.

When engaging in personal property transactions, utilizing a thorough General Bill of Sale template ensures clarity and legal validity, benefiting both buyers and sellers in the agreement process.

Rv Bill of Sale Pdf - Completing an RV Bill of Sale is a step toward a smooth and legal transaction between buyer and seller.

Simple Bill of Sale for Motorcycle - This form is typically required for title transfers in many states.

Filling out a Business Bill of Sale form is an important step in transferring ownership of a business or its assets. Below are key takeaways to consider when using this form:

Once you have your Business Bill of Sale form ready, it’s time to fill it out accurately. This form is essential for documenting the sale of a business and ensuring both parties are clear on the terms of the transaction. Follow these steps to complete the form correctly.

After completing the form, ensure that both parties retain a copy for their records. This documentation will serve as proof of the transaction and can be important for future reference.

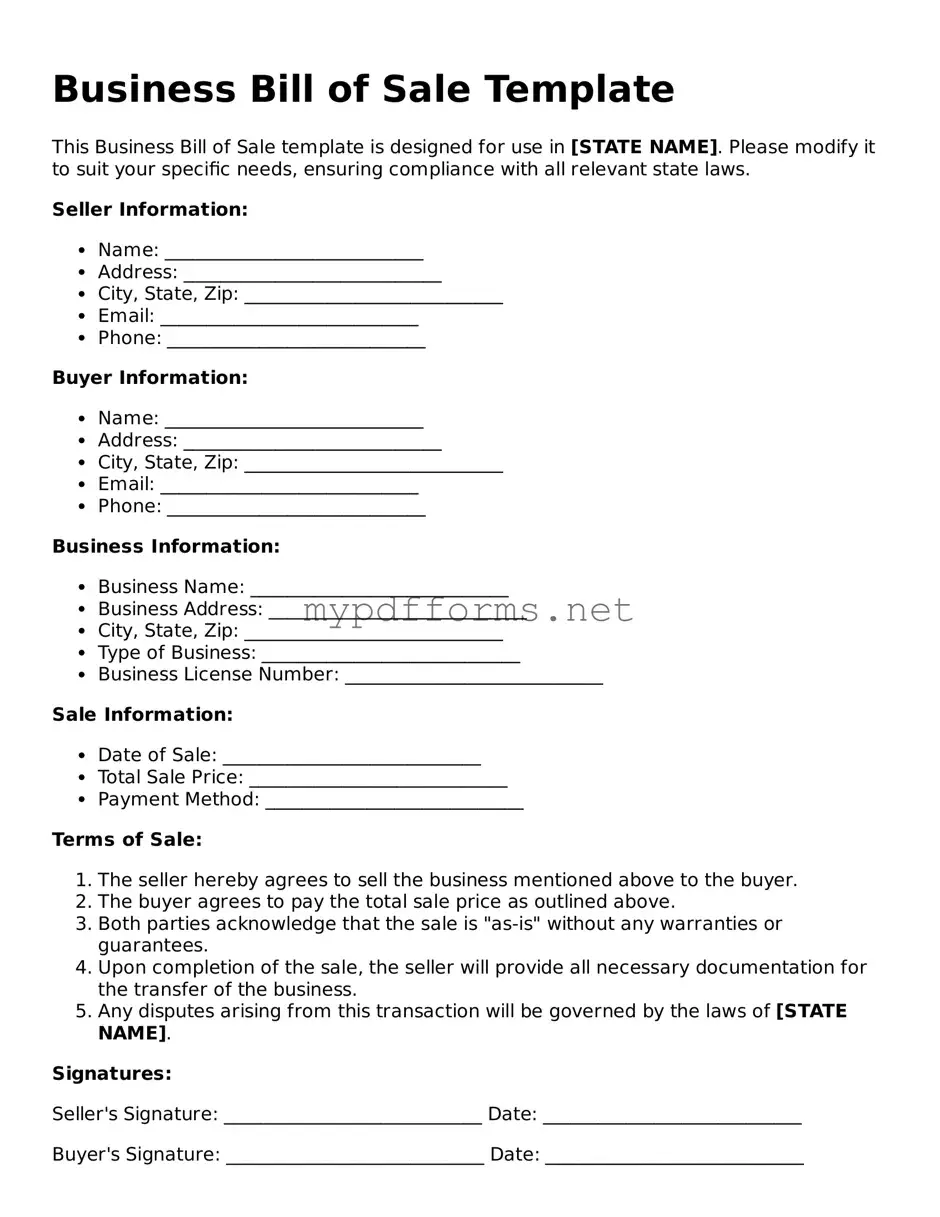

A Business Bill of Sale is a legal document that transfers ownership of a business from one party to another. It outlines the details of the transaction, including the names of the buyer and seller, the purchase price, and a description of the business being sold.

This document serves as proof of the transaction. It protects both the buyer and seller by clearly stating the terms of the sale. Having a formal record can help prevent disputes in the future regarding ownership and the terms of the sale.

Key information typically includes:

While it may not be legally required in every state, it is highly recommended. Having this document can provide legal protection and clarity for both parties involved in the sale.

Yes, you can create your own Business Bill of Sale. However, it is important to ensure that it includes all necessary information and complies with state laws. Consulting with a legal professional can help ensure that your document is valid and enforceable.

After completing the document, both the buyer and seller should sign it. It is advisable to keep copies for your records. Depending on the nature of the business, you may also need to notify local or state authorities about the change in ownership.

The Business Bill of Sale is similar to a Personal Bill of Sale. Both documents serve as a formal record of the transfer of ownership from one party to another. A Personal Bill of Sale is typically used for individual transactions involving personal property, such as vehicles or equipment. Like the Business Bill of Sale, it includes details about the item being sold, the purchase price, and the identities of the buyer and seller. Both documents aim to protect the interests of both parties and provide proof of the transaction.

Another document comparable to the Business Bill of Sale is the Asset Purchase Agreement. This agreement is often used in business transactions to outline the terms under which one party purchases specific assets from another. While the Business Bill of Sale focuses on the transfer of ownership, the Asset Purchase Agreement provides a more detailed framework, including representations and warranties, liabilities, and conditions for the sale. Both documents facilitate the legal transfer of assets, but the Asset Purchase Agreement usually covers more complex transactions.

The Equipment Bill of Sale is also similar to the Business Bill of Sale. This document specifically pertains to the sale of equipment, such as machinery or tools. It includes essential details about the equipment, such as its condition, model, and serial number, along with the purchase price and buyer-seller information. Like the Business Bill of Sale, it serves to confirm the transfer of ownership and can be used for record-keeping purposes. Both documents help clarify the terms of the sale and protect the rights of both parties involved.

A Vehicle Bill of Sale shares similarities with the Business Bill of Sale as well. This document is specifically designed for the sale of motor vehicles. It includes information such as the vehicle identification number (VIN), make, model, year, and odometer reading, along with the sale price and buyer-seller details. Both documents provide a legal record of the transaction and can be used for title transfer and registration purposes. They help ensure that both parties are protected and that the transaction is conducted fairly.

The Real Estate Purchase Agreement is another document that bears resemblance to the Business Bill of Sale. This agreement is used when transferring ownership of real property, such as land or buildings. It outlines the terms of the sale, including the purchase price, contingencies, and closing date. While the Business Bill of Sale is typically simpler and more straightforward, both documents serve the same fundamental purpose of formalizing the transfer of ownership and protecting the rights of the involved parties.

In New Jersey, having the right documentation is paramount when engaging in various sales transactions, as these documents not only provide clarity but also protect the interests of all parties involved. For those looking to simplify the process, resources such as NJ PDF Forms can be invaluable in ensuring that the required paperwork is readily accessible and compliant with state laws.

Lastly, the Lease Agreement can be compared to the Business Bill of Sale in certain contexts. While a Lease Agreement does not transfer ownership, it establishes the terms under which one party rents property from another. Both documents require clear identification of the parties involved, the property in question, and the terms of the agreement. They serve to protect the rights and responsibilities of both parties, ensuring that there is a mutual understanding of the terms involved, whether for a sale or a lease arrangement.

When engaging in a business transaction, the Business Bill of Sale form serves as a critical document to formalize the transfer of ownership. However, it is often accompanied by several other forms and documents that help clarify the terms of the sale and protect both parties involved. Here are four commonly used documents that complement the Business Bill of Sale:

Incorporating these additional documents alongside the Business Bill of Sale can significantly enhance the clarity and security of the transaction. Each form plays a vital role in ensuring that both buyers and sellers understand their rights and obligations, ultimately leading to a smoother and more successful business transfer.

When it comes to the Business Bill of Sale form, several misconceptions can lead to confusion and potential issues. Understanding these misconceptions is crucial for anyone involved in a business transaction. Here’s a look at some of the most common misunderstandings:

Being aware of these misconceptions can help ensure that business transactions are conducted smoothly and legally. Always consider consulting a legal professional to clarify any doubts regarding the use of a Business Bill of Sale form.