Get Business Credit Application Form in PDF

Get Business Credit Application Form in PDF

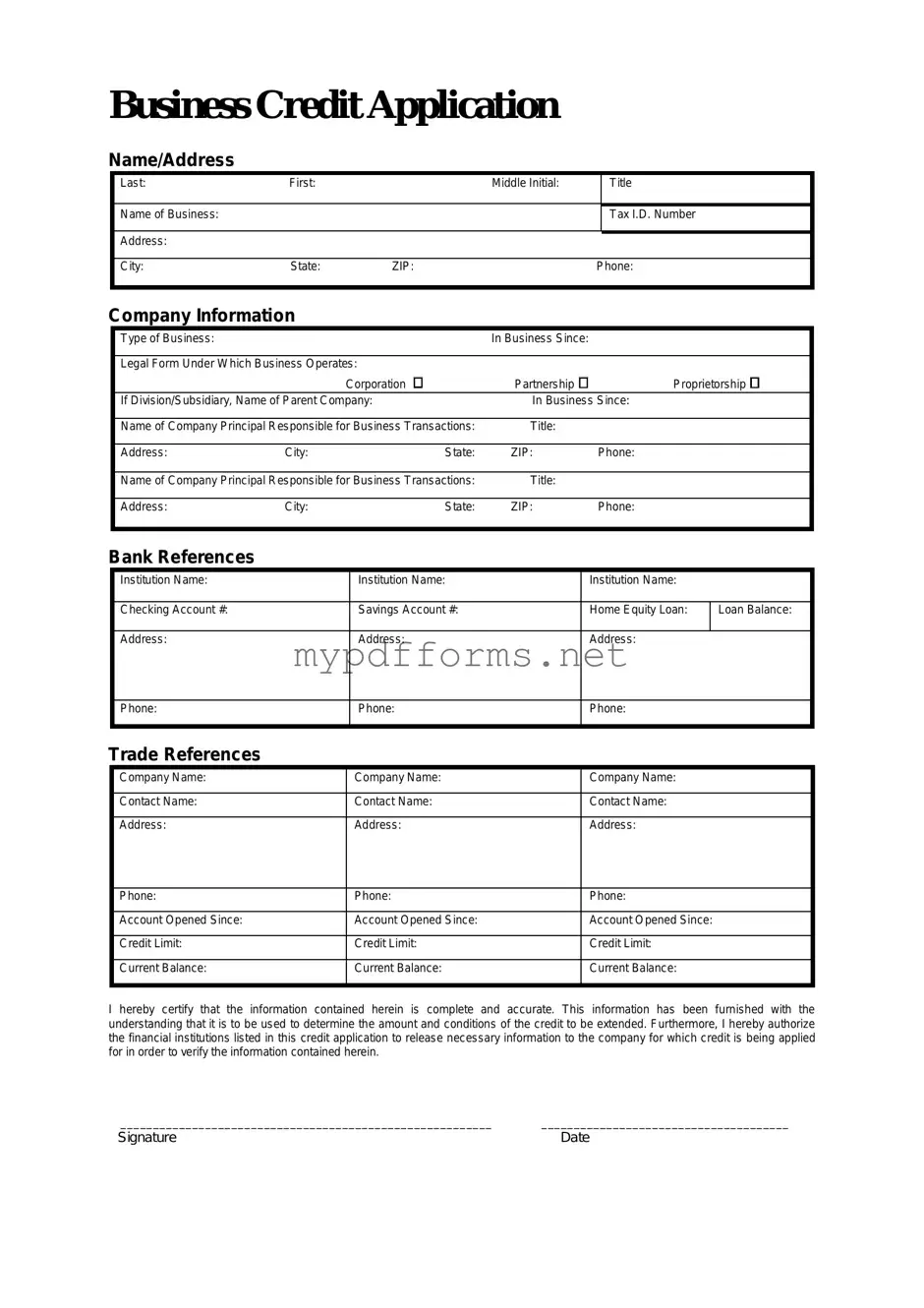

The Business Credit Application form serves as a crucial tool for companies seeking to establish credit with suppliers and lenders. This form typically collects essential information about the business, including its legal name, address, and contact details. It also requires financial data such as annual revenue, number of employees, and ownership structure, which helps creditors assess the company's creditworthiness. Additionally, the form often includes sections for personal guarantees from business owners, allowing lenders to evaluate the risk associated with extending credit. By providing a comprehensive overview of the business's financial health and operational history, the Business Credit Application form facilitates informed decision-making for both the applicant and the creditor. Understanding the intricacies of this form can streamline the credit application process and enhance the chances of approval, ultimately supporting the growth and sustainability of the business.

When filling out a Business Credit Application form, there are important dos and don’ts to keep in mind. Following these guidelines can help ensure your application is processed smoothly and efficiently.

State of Michigan Divorce Forms - Each section of the form is crucial for establishing the details of the divorce case.

In the process of forming an LLC in Illinois, it’s essential to ensure that all foundational documents are in place, including the vital Operating Agreement. This document not only delineates the roles and responsibilities of members but also aids in establishing a clear protocol for decision-making and conflict resolution. For more guidance and templates, consider exploring Illinois Forms, which can help streamline the formation process and ensure compliance with state regulations.

D1 Application Form Download - You can exchange your foreign or Northern Ireland licence for a British one.

Filling out a Business Credit Application form can be a crucial step for any business seeking to establish credit with suppliers or financial institutions. Understanding the key components of this process can help ensure a smooth application experience.

By keeping these key takeaways in mind, businesses can navigate the credit application process more effectively, ultimately leading to better financial opportunities.

Once you have the Business Credit Application form ready, it's time to fill it out accurately. Providing complete and correct information is essential for processing your application efficiently.

After completing the form, double-check all entries for accuracy. Submit the application according to the instructions provided, and await further communication regarding your credit request.

The Business Credit Application form is a document that businesses complete to request credit from a lender or supplier. This form typically includes information about the business, such as its legal name, address, type of business, and financial details. By submitting this application, a business seeks to establish a credit line or obtain financing for operational needs.

This form is crucial for several reasons. First, it helps lenders assess the creditworthiness of a business. The information provided allows them to evaluate the risk involved in extending credit. Second, it establishes a formal record of the business's request for credit, which can be important for both parties in future transactions. Lastly, completing this form accurately can lead to better credit terms and conditions.

A Business Credit Application form generally requires a variety of information. This includes:

Providing complete and accurate information is essential for a smooth application process.

The processing time for a Business Credit Application can vary significantly depending on the lender or supplier. Typically, it can take anywhere from a few hours to several days. Factors influencing the timeline include the complexity of the application, the lender's internal processes, and the volume of applications being processed. Businesses are encouraged to follow up with the lender if they do not receive a response within a reasonable timeframe.

The Business Loan Application is a document that serves a similar purpose to the Business Credit Application form. Both forms are designed to gather essential information about a business seeking financial assistance. The loan application typically includes details about the company’s financial history, creditworthiness, and the purpose of the loan. Just like the credit application, it requires information about the business owner, including personal guarantees and assets, which helps lenders assess risk and make informed decisions.

The Vendor Credit Application is another document closely related to the Business Credit Application. This form is used by businesses when applying for credit from suppliers or vendors. It collects similar information regarding the business’s credit history, financial stability, and payment terms. Both applications aim to establish trust and ensure that the business can fulfill its financial obligations, making them vital for maintaining healthy vendor relationships.

A Personal Credit Application is often used by individuals seeking credit for personal use, such as loans or credit cards. While it focuses on personal financial information, it shares a common goal with the Business Credit Application: evaluating creditworthiness. Both forms require detailed information about income, debts, and credit history, allowing lenders to gauge the applicant’s ability to repay the borrowed amount.

As various business forms play essential roles in financial transactions, one key aspect often overlooked is the proper handling of unclaimed funds. The Ohio Unclaimed form is specifically designed to assist companies in reporting unclaimed assets, ensuring that they comply with state regulations while also aiding individuals in recovering their lost funds.

The Commercial Lease Application is another document that shares similarities with the Business Credit Application. When a business seeks to rent commercial space, landlords often require this application to assess the tenant’s financial stability. Like the credit application, it includes financial disclosures, business history, and references, helping landlords determine if the business can meet lease obligations.

The Business Partnership Agreement is a document that outlines the terms of a partnership between two or more business entities. While it serves a different purpose, it often requires financial disclosures similar to those found in a Business Credit Application. Both documents aim to clarify financial responsibilities and expectations, ensuring that all parties involved understand their roles and obligations.

The Equipment Financing Application is used by businesses looking to acquire equipment through financing. This application gathers information about the business’s financial health and its ability to repay the financing. Like the Business Credit Application, it assesses the risk involved in lending money, focusing on the business’s cash flow and credit history to make informed lending decisions.

The Merchant Cash Advance Application is another document that resembles the Business Credit Application. It allows businesses to apply for an advance based on future credit card sales. Both applications require financial information, including revenue and creditworthiness, to evaluate the business's capacity to repay the advance. This similarity lies in the focus on the business's financial performance and the assessment of risk involved.

The Business Insurance Application is a document that businesses complete to obtain insurance coverage. While it primarily focuses on risk assessment for insurance purposes, it shares some similarities with the Business Credit Application. Both documents require detailed financial information, business history, and operational data to help underwriters evaluate the risk associated with insuring the business.

The Business Registration Application is essential for legally establishing a business entity. While its primary purpose is to register the business with the state, it often requires financial disclosures similar to those in a Business Credit Application. Both forms aim to provide a clear picture of the business's operations, ownership, and financial status, ensuring compliance with legal requirements and helping to establish credibility.

Finally, the SBA Loan Application is used when businesses seek loans backed by the Small Business Administration. This application is similar to the Business Credit Application in that it gathers comprehensive financial information and business history. Both documents are designed to help lenders assess the viability of the business and its ability to repay the loan, making them critical tools in the financing process.

When applying for business credit, several forms and documents may accompany the Business Credit Application form. These documents help lenders assess the creditworthiness of the business and ensure a thorough evaluation of the application. Below is a list of commonly used documents.

Including these documents with the Business Credit Application form can significantly enhance the chances of approval. Each document plays a vital role in presenting a complete picture of the business’s financial situation and commitment to meeting its obligations.

Many people hold misconceptions about the Business Credit Application form. Understanding these can help clarify the process and ease any concerns. Here are ten common misconceptions:

By addressing these misconceptions, businesses can approach the credit application process with more confidence and clarity.