Attorney-Verified Deed in Lieu of Foreclosure Document for California

Attorney-Verified Deed in Lieu of Foreclosure Document for California

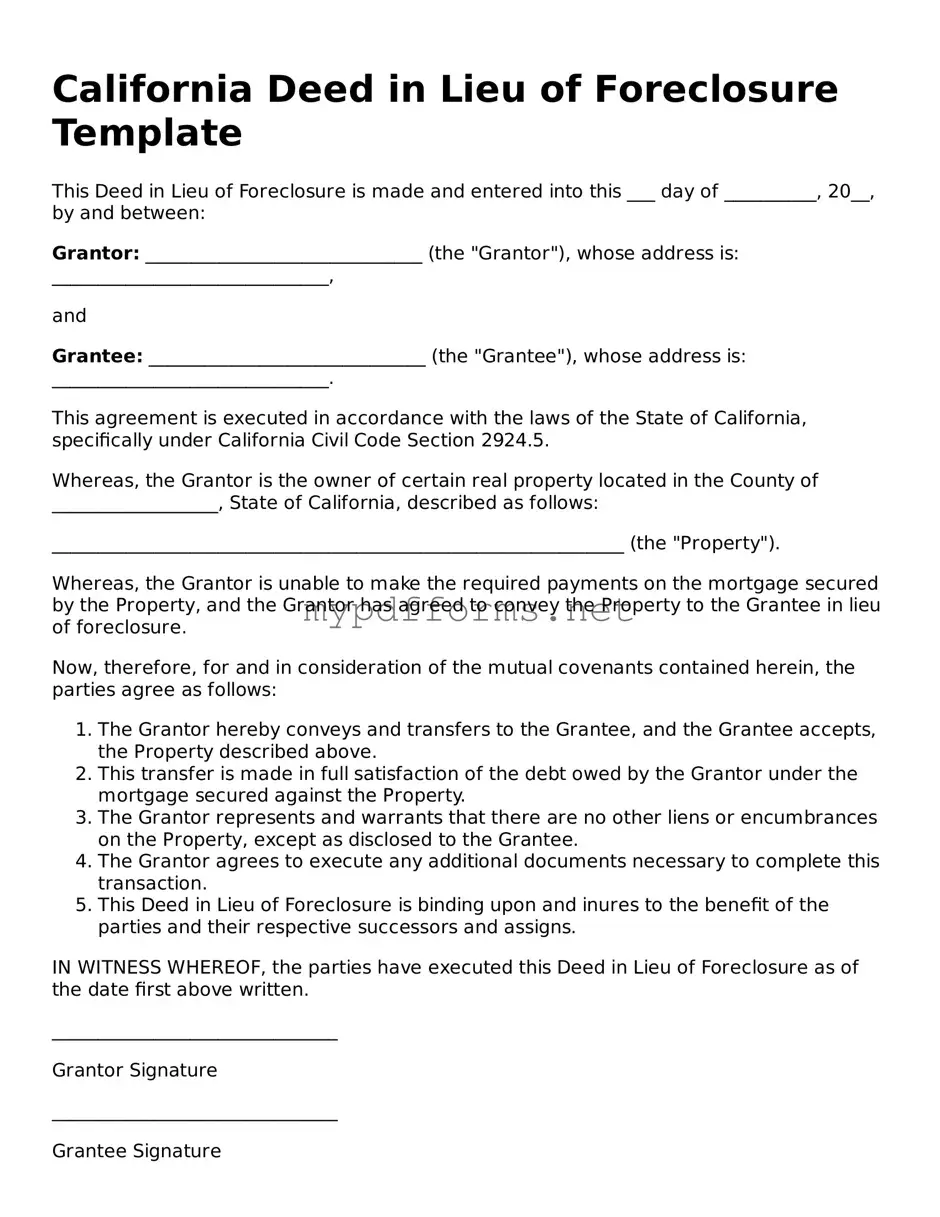

In the realm of real estate and mortgage transactions, the California Deed in Lieu of Foreclosure form serves as a critical tool for homeowners facing financial hardship. This form allows property owners to voluntarily transfer ownership of their home back to the lender, effectively avoiding the lengthy and often stressful foreclosure process. By completing this deed, homeowners can mitigate the negative impacts on their credit score that typically accompany foreclosure, while also providing lenders with a more efficient way to reclaim the property. The form includes essential details such as the names of the parties involved, a legal description of the property, and any outstanding debts associated with the mortgage. Additionally, it outlines the conditions under which the deed is executed, ensuring that both the homeowner and the lender understand their rights and obligations. This option not only facilitates a smoother transition for distressed homeowners but also enables lenders to manage their assets more effectively. Understanding the implications and requirements of the Deed in Lieu of Foreclosure is vital for anyone considering this path as a solution to their financial difficulties.

When filling out the California Deed in Lieu of Foreclosure form, it’s important to approach the process with care. Here are some essential dos and don’ts to keep in mind:

Deed in Lieu of Foreclosure Texas - This form helps facilitate an agreement between the homeowner and lender to avoid lengthy litigation.

A Texas Quitclaim Deed is a legal document used to transfer ownership of real property from one party to another without guaranteeing the title's validity. This form allows the grantor to relinquish any interest in the property, making it a straightforward option for property transfers among family members or acquaintances. To begin the process of completing this form, visit https://quitclaimdocs.com/fillable-texas-quitclaim-deed for more information.

Deed in Lieu of Foreclosure Ny - This process may help prevent the long-term damage to credit associated with foreclosure.

Filling out and using the California Deed in Lieu of Foreclosure form can be a crucial step for homeowners facing financial difficulties. Here are some key takeaways to consider:

After completing the California Deed in Lieu of Foreclosure form, you will need to submit it to the appropriate parties involved in the foreclosure process. This typically includes the lender and may require additional documentation. Ensure that you keep copies for your records and verify that all parties have received the necessary paperwork.

A Deed in Lieu of Foreclosure is a legal process where a homeowner voluntarily transfers the title of their property to the lender to avoid foreclosure. This option allows the borrower to walk away from their mortgage obligations without going through the lengthy foreclosure process.

This option can provide several advantages, including:

Generally, homeowners who are facing financial difficulties and are unable to keep up with their mortgage payments may qualify. Lenders typically require that the homeowner has exhausted other options, such as loan modification or short sale, before considering a Deed in Lieu.

The process usually involves the following steps:

In many cases, homeowners may be released from their mortgage obligations after the transfer. However, it’s important to negotiate this with your lender, as some lenders may pursue a deficiency judgment if the property sells for less than the outstanding mortgage balance.

While a Deed in Lieu is less damaging than a foreclosure, it will still impact your credit score. Typically, it may remain on your credit report for up to seven years. However, the exact impact varies depending on your overall credit history.

Homeowners may be allowed to stay in the property until the Deed is finalized, but this depends on the lender’s policies. It’s essential to clarify this with your lender early in the process.

If your request is denied, consider discussing alternative options with your lender, such as a loan modification or a short sale. Consulting with a housing counselor or legal professional can also provide guidance tailored to your situation.

A Short Sale is a process where a homeowner sells their property for less than the amount owed on their mortgage. Like a Deed in Lieu of Foreclosure, it allows the homeowner to avoid foreclosure. In both cases, the lender agrees to accept less than the full amount owed. However, in a short sale, the property is sold to a third party, while in a Deed in Lieu, the homeowner transfers ownership directly to the lender. Both options aim to relieve the financial burden on the homeowner and minimize losses for the lender.

A Loan Modification is another document that shares similarities with a Deed in Lieu of Foreclosure. In a loan modification, the lender agrees to change the terms of the mortgage to make it more affordable for the homeowner. This can include lowering the interest rate or extending the loan term. Both processes aim to help homeowners avoid foreclosure, but while a Deed in Lieu transfers ownership, a loan modification keeps the homeowner in their home by making payments manageable.

A Forebearance Agreement is also comparable. This document allows a homeowner to temporarily pause or reduce their mortgage payments. The lender agrees to this arrangement, often to help the homeowner get back on their feet financially. Like a Deed in Lieu of Foreclosure, it provides a way to avoid foreclosure. However, a forbearance is a temporary solution, while a Deed in Lieu is a permanent transfer of property ownership to the lender.

For those looking to ensure their healthcare wishes are respected, utilizing a Do Not Resuscitate Order form is crucial, especially for individuals facing serious health challenges.

Finally, a Bankruptcy Filing can be similar in its goal to prevent foreclosure. When a homeowner files for bankruptcy, it can halt foreclosure proceedings temporarily. This gives the homeowner time to reorganize their finances. Both a Deed in Lieu and bankruptcy can provide relief from the threat of losing a home. However, bankruptcy involves legal proceedings and can impact credit scores significantly, while a Deed in Lieu is a more straightforward transfer of ownership without court involvement.

A Deed in Lieu of Foreclosure can be a valuable tool for homeowners facing financial hardship. However, it is often accompanied by several other forms and documents that facilitate the process and ensure all legal requirements are met. Below is a list of documents commonly used alongside the California Deed in Lieu of Foreclosure.

Understanding these documents is crucial for homeowners considering a Deed in Lieu of Foreclosure. Each plays a significant role in ensuring a smooth transition and protecting the rights of all parties involved. Properly managing these forms can lead to a more favorable outcome for those navigating financial difficulties.

Many homeowners facing financial difficulties may consider a Deed in Lieu of Foreclosure as a potential solution. However, there are several misconceptions surrounding this process that can lead to confusion. Here are eight common misunderstandings:

Understanding these misconceptions is crucial for homeowners considering their options. It is important to approach the situation with a clear understanding of the potential consequences and benefits.