Attorney-Verified Loan Agreement Document for California

Attorney-Verified Loan Agreement Document for California

The California Loan Agreement form serves as a crucial document for individuals and entities engaging in lending transactions within the state. This form outlines the specific terms and conditions agreed upon by both the lender and the borrower, ensuring clarity and mutual understanding. Key components typically include the loan amount, interest rate, repayment schedule, and any collateral involved. Additionally, the agreement may specify the consequences of default, providing a clear framework for resolving disputes. By detailing the obligations and rights of each party, the California Loan Agreement aims to protect both the lender's investment and the borrower's ability to repay the loan. Understanding this form is essential for anyone considering a loan in California, as it establishes the legal foundation for the transaction and helps prevent potential misunderstandings in the future.

When filling out the California Loan Agreement form, attention to detail is crucial. Here are some important dos and don'ts to keep in mind:

Texas Promissory Note Form - Clearly articulated payment methods can facilitate smooth transactions between lender and borrower.

In addition to its importance in establishing a clear framework for operations, the Florida Operating Agreement form can be easily accessed and downloaded from floridapdfform.com/, making it a convenient resource for business owners looking to ensure their LLC functions smoothly and efficiently.

Promissory Note Florida Pdf - Identifies the parties involved in the loan transaction.

When dealing with a California Loan Agreement form, understanding its essential components is crucial for both lenders and borrowers. Here are some key takeaways to consider:

By paying attention to these key aspects, both parties can foster a clearer understanding of their responsibilities and expectations throughout the loan process.

Filling out the California Loan Agreement form requires careful attention to detail. This document is essential for establishing the terms of a loan between parties. Once completed, the form will serve as a binding agreement that outlines the responsibilities and expectations of both the lender and the borrower.

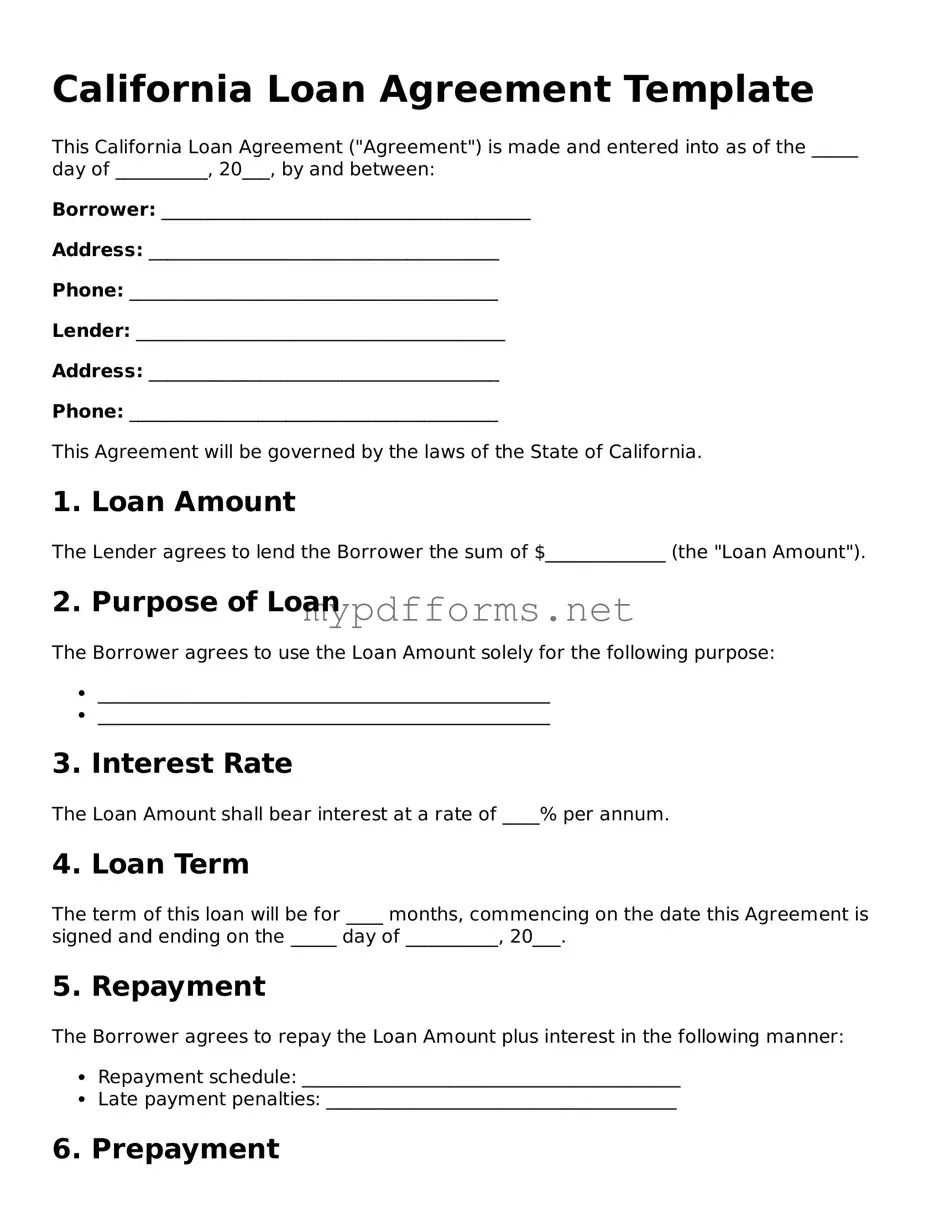

A California Loan Agreement form is a legal document that outlines the terms and conditions of a loan between a lender and a borrower. This form typically includes details such as the loan amount, interest rate, repayment schedule, and any collateral involved. It serves to protect the rights of both parties by clearly defining their obligations and expectations.

This form is suitable for individuals or businesses in California who are lending or borrowing money. It can be used in various situations, including personal loans between friends or family members, business loans, or even real estate transactions. Anyone seeking to formalize a loan arrangement should consider using this document to ensure clarity and legal protection.

A typical California Loan Agreement form includes several important components:

Including these elements helps ensure that both parties have a clear understanding of the loan's terms.

Yes, when properly executed, a California Loan Agreement form is a legally binding contract. Both parties must agree to the terms and sign the document for it to be enforceable. If disputes arise, the agreement can be presented in court as evidence of the agreed-upon terms. It is advisable to keep a copy of the signed agreement for reference.

The California Loan Agreement form shares similarities with a Promissory Note. Both documents outline the terms of a loan, including the amount borrowed, interest rates, and repayment schedules. While a Loan Agreement is more comprehensive, detailing the rights and obligations of both parties, a Promissory Note is typically a simpler document that primarily focuses on the borrower's promise to repay the loan. Both documents serve as legal evidence of the loan arrangement and can be enforced in court if necessary.

Another document similar to the California Loan Agreement is the Mortgage Agreement. While a Loan Agreement can be unsecured, a Mortgage Agreement specifically secures the loan with real property. This means that if the borrower defaults, the lender has the right to foreclose on the property. Both documents include terms regarding repayment and may outline penalties for late payments, but the Mortgage Agreement also includes specific provisions related to the property being used as collateral.

The California Loan Agreement is also akin to a Security Agreement. In both documents, the borrower agrees to provide collateral to secure the loan. A Security Agreement, however, is often used for personal property rather than real estate. It details the specific collateral and the rights of the lender in the event of default. While both documents aim to protect the lender's interests, the Security Agreement is more focused on the specific assets pledged as security.

A similar document is the Loan Application. This document is typically completed by the borrower to provide the lender with necessary information about their financial situation. While the Loan Agreement finalizes the terms of the loan, the Loan Application initiates the lending process. Both documents are essential in establishing the lender-borrower relationship, but they serve different purposes within that relationship.

The California Loan Agreement can also be compared to a Lease Agreement, particularly when the loan is related to rental property. Both documents outline terms and conditions regarding the use of property, including payment amounts and timelines. However, a Lease Agreement specifically pertains to the rental of property, while a Loan Agreement is focused on the borrowing of funds. Both documents require clear communication of obligations to prevent disputes.

Another related document is the Loan Modification Agreement. This document is used when the terms of an existing loan need to be changed, such as adjusting interest rates or extending repayment periods. While the California Loan Agreement sets the original terms, a Loan Modification Agreement serves to update those terms to better suit the needs of both the borrower and lender. Both documents require mutual consent and are legally binding.

Understanding various loan agreements is essential for both lenders and borrowers to navigate the complexities of financial transactions. For example, the motorcyclebillofsale.com/free-georgia-motorcycle-bill-of-sale is a critical legal document that ensures the proper transfer of motorcycle ownership, similar to how loan agreements clarify the expectations between lending parties. Each type of agreement serves a unique purpose, emphasizing the importance of formalizing financial exchanges to safeguard rights and responsibilities.

The California Loan Agreement is also similar to a Forbearance Agreement. This document is utilized when a borrower is struggling to make payments and requests temporary relief from their obligations. Both agreements require the lender's approval and outline new terms for repayment. However, a Forbearance Agreement is specifically focused on providing short-term relief, whereas the Loan Agreement establishes the long-term terms of the loan.

A similar document is the Loan Repayment Plan. This plan details how a borrower will repay their loan over time, including specific payment amounts and due dates. While the Loan Agreement provides the overall framework for the loan, the Loan Repayment Plan breaks down the repayment process into manageable steps. Both documents aim to ensure that the borrower understands their obligations and can fulfill them.

Lastly, the California Loan Agreement resembles a Debt Settlement Agreement. This document is used when a borrower negotiates with a lender to settle a debt for less than the total amount owed. Both agreements involve discussions between the borrower and lender, but a Debt Settlement Agreement typically occurs after a borrower has defaulted or is at risk of defaulting. While the Loan Agreement is proactive in establishing terms, the Debt Settlement Agreement is reactive, often arising from financial distress.

When entering into a loan agreement in California, several other forms and documents often accompany the primary agreement. These documents help clarify the terms of the loan, protect the interests of both parties, and ensure compliance with state laws. Below is a list of some commonly used documents alongside the California Loan Agreement form.

Understanding these accompanying documents is crucial for both borrowers and lenders. They not only enhance the clarity of the loan agreement but also help safeguard the rights and responsibilities of each party involved.

Many people have misunderstandings about the California Loan Agreement form. Let’s clear up some common misconceptions.

Understanding these points can help you navigate the loan process more effectively. Always consider consulting a professional if you have questions about your specific situation.