Attorney-Verified Promissory Note Document for California

Attorney-Verified Promissory Note Document for California

The California Promissory Note form serves as a crucial financial instrument that outlines the terms under which one party, the borrower, agrees to repay a specified sum of money to another party, the lender. This legally binding document is not merely a piece of paper; it encapsulates the essence of trust and obligation between individuals or entities engaged in a lending arrangement. Typically, the form includes essential details such as the principal amount, interest rate, repayment schedule, and any applicable fees or penalties for late payments. Additionally, it often specifies the rights and responsibilities of both parties, ensuring clarity and mutual understanding. Importantly, the Promissory Note may also include provisions for default, outlining the consequences should the borrower fail to meet their obligations. As a result, this document plays a vital role in fostering transparency and accountability in financial transactions, providing both parties with a clear framework for their agreement. Understanding the nuances of this form is essential for anyone involved in lending or borrowing, as it lays the groundwork for a successful financial relationship.

When filling out the California Promissory Note form, it's important to follow some guidelines. Here’s a list of things you should and shouldn’t do:

Following these steps can help avoid potential issues down the road. Make sure to double-check everything before submitting your form.

New York Promissory Note - Effective communication between the parties can facilitate smoother transactions.

When engaging in any sale, understanding the importance of a Bill of Sale form in New Jersey is crucial; this document not only facilitates a smooth transaction but also serves as a protective measure for both the seller and buyer. For those seeking a reliable template, resources like NJ PDF Forms provide accessible options to ensure that all necessary details are captured accurately.

Loan Agreement Template Texas - A notice period before default may also be a part of the terms outlined.

When filling out and using the California Promissory Note form, keep the following key takeaways in mind:

Once you have the California Promissory Note form in front of you, it's time to fill it out accurately. This document serves as a written promise to pay a specific amount of money under agreed-upon terms. Completing it correctly is essential to ensure that both parties understand their obligations. Follow these steps to fill out the form properly.

After completing the form, keep a copy for your records and provide a copy to the other party. This ensures that both sides have a clear understanding of the terms agreed upon. Proper documentation can help prevent misunderstandings in the future.

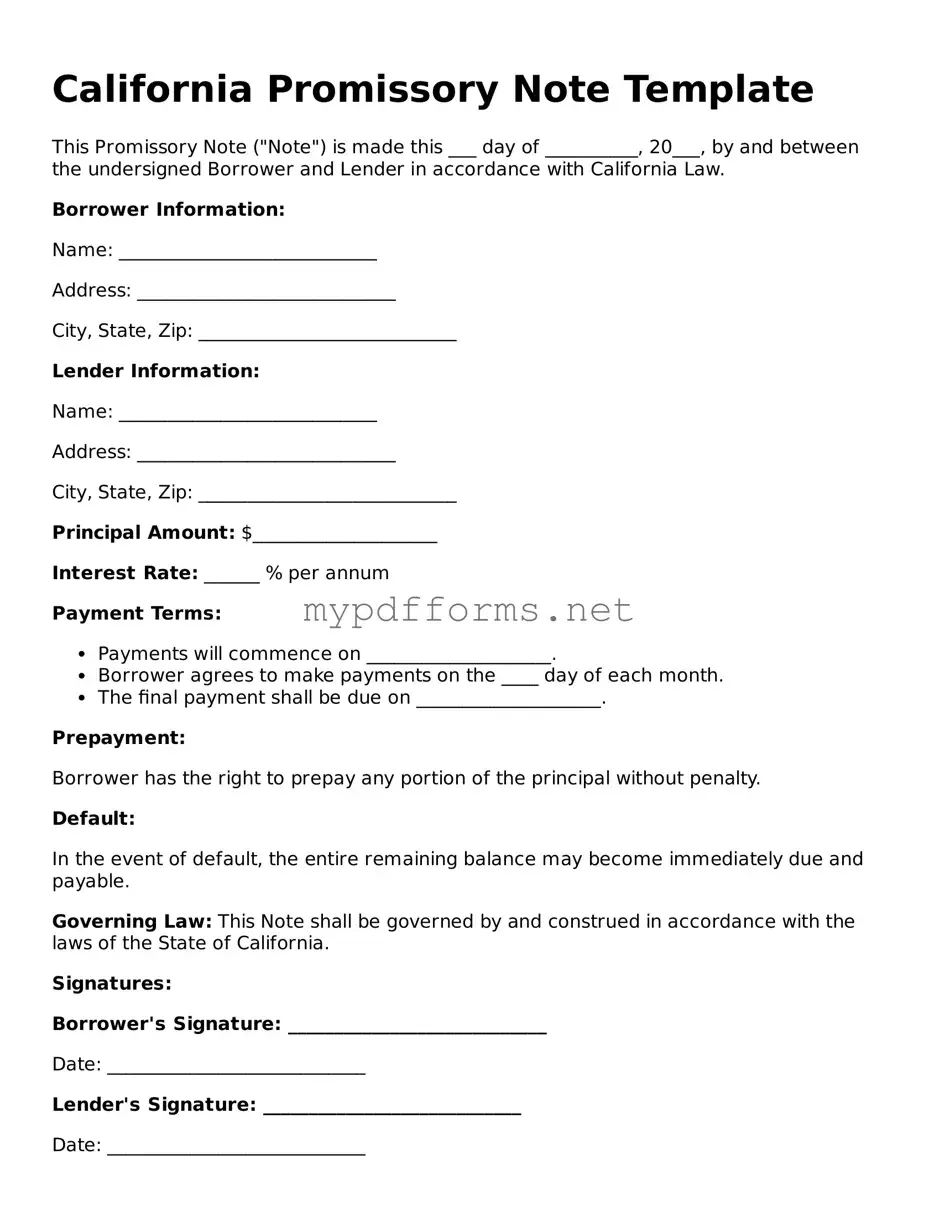

A California Promissory Note is a written agreement between a borrower and a lender. It outlines the terms under which the borrower agrees to repay a specific amount of money. This document includes details such as the loan amount, interest rate, repayment schedule, and any penalties for late payments.

Key components of a California Promissory Note include:

Yes, a California Promissory Note is legally binding as long as it meets certain requirements. Both parties must agree to the terms, and the note must be signed by the borrower. It is advisable to have the document witnessed or notarized to strengthen its enforceability.

Absolutely. While there are standard templates available, you can customize a California Promissory Note to fit your specific needs. You may want to include additional clauses, such as provisions for default, prepayment, or collateral. However, it’s important to ensure that any modifications comply with California law.

A loan agreement is similar to a promissory note in that it outlines the terms of a loan between a borrower and a lender. Both documents specify the amount borrowed, the interest rate, and the repayment schedule. However, a loan agreement is generally more comprehensive, often detailing additional terms such as collateral, default conditions, and the rights and responsibilities of both parties. While a promissory note is a straightforward promise to pay, a loan agreement provides a broader framework for the entire borrowing relationship.

A mortgage is another document that shares similarities with a promissory note. In a mortgage, the borrower agrees to repay a loan used to purchase real estate, and the property itself serves as collateral. Like a promissory note, a mortgage includes details about the loan amount and repayment terms. However, a mortgage also includes specific provisions regarding the property, including what happens if the borrower defaults. The promissory note is often part of the mortgage transaction, representing the borrower's promise to repay the loan.

An installment agreement is akin to a promissory note in that it involves a borrower agreeing to repay a debt in regular payments over time. Both documents specify the amount owed and the payment schedule. However, an installment agreement may cover a broader range of transactions, such as the purchase of goods or services, while a promissory note is typically focused on a loan. The installment agreement may also include terms regarding late fees or penalties for missed payments, providing additional protections for the lender.

For those looking to document the purchase of a trailer, the official trailer bill of sale form in Maryland is a valuable resource. This document not only verifies the sale but also guarantees that both parties are protected by including pertinent details such as buyer and seller information, along with the sale price and trailer description.

A personal guarantee is similar to a promissory note in that it involves a commitment to repay a debt. In this case, a third party agrees to take responsibility for the debt if the primary borrower defaults. While a promissory note is a direct promise from the borrower, a personal guarantee adds an extra layer of security for the lender. This document can be especially important in business transactions where the lender wants assurance that someone will be accountable for the debt.

A security agreement shares similarities with a promissory note as both documents deal with debts and obligations. In a security agreement, the borrower pledges collateral to secure a loan. This agreement outlines the terms under which the lender can claim the collateral if the borrower defaults. While a promissory note is simply a promise to pay, a security agreement provides the lender with rights to specific assets, making it a more protective measure in lending situations.

A deed of trust is another document that resembles a promissory note, particularly in real estate transactions. A deed of trust involves three parties: the borrower, the lender, and a trustee. The borrower signs a promissory note, which is secured by the deed of trust on the property. This document outlines the terms of the loan and what happens if the borrower defaults. While the promissory note is the promise to repay, the deed of trust provides a legal claim to the property itself.

A loan modification agreement is similar to a promissory note in that it involves changes to the original loan terms. This document is used when a borrower and lender agree to alter the repayment terms, interest rate, or other conditions of the original promissory note. While a promissory note represents the initial agreement, a loan modification acknowledges that circumstances have changed, and both parties need to adjust their expectations accordingly.

Finally, a lease agreement can be compared to a promissory note in that it involves a commitment to pay for the use of property, typically real estate. Both documents outline payment amounts and schedules. However, a lease agreement typically includes additional terms related to the use of the property, such as maintenance responsibilities and duration of the lease. While a promissory note is focused solely on repayment, a lease agreement encompasses a broader relationship between the tenant and landlord.

When engaging in a loan agreement in California, a Promissory Note is often accompanied by various other documents to ensure clarity and legal protection for both parties involved. Here is a list of common forms and documents that may be used alongside a California Promissory Note:

These documents play a crucial role in establishing the terms of the loan and protecting the interests of both the lender and the borrower. Understanding each of these forms can help ensure a smoother transaction and minimize potential disputes down the line.

When it comes to the California Promissory Note form, there are several misconceptions that can lead to confusion. Understanding these misconceptions is essential for anyone involved in lending or borrowing money. Here are four common misunderstandings:

Understanding these misconceptions can help individuals navigate the lending landscape more effectively. A clear grasp of what a California Promissory Note entails can lead to smoother transactions and better financial relationships.