Get Cg 20 10 07 04 Liability Endorsement Form in PDF

Get Cg 20 10 07 04 Liability Endorsement Form in PDF

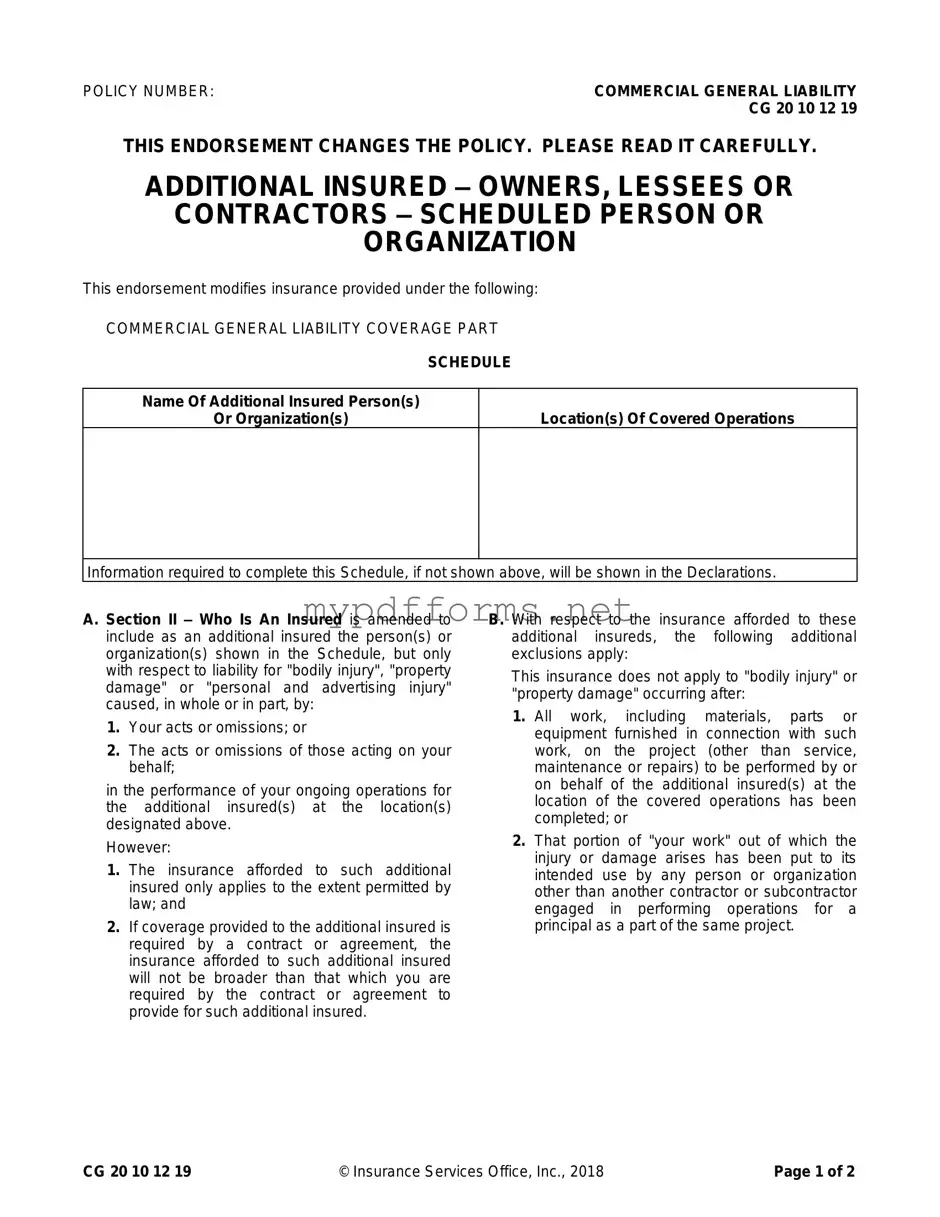

The CG 20 10 07 04 Liability Endorsement form is a crucial document for businesses seeking to add additional insured parties to their commercial general liability policy. It specifically allows owners, lessees, or contractors to be named as additional insureds, which can provide them with important coverage against claims for bodily injury, property damage, or personal and advertising injury. This endorsement is particularly relevant for ongoing operations at designated locations, as it clarifies the scope of coverage in relation to the actions of the insured and their representatives. However, it is essential to note that this coverage is limited by the terms of any existing contracts, ensuring that the insurance provided does not exceed what is required. Additionally, the endorsement outlines specific exclusions, such as coverage ceasing after project completion or when the work has been put to its intended use. Understanding these details is vital for all parties involved to ensure compliance and adequate protection under the policy.

When filling out the CG 20 10 07 04 Liability Endorsement form, it’s important to follow certain guidelines to ensure accuracy and compliance. Here’s a list of things you should and shouldn’t do:

Australian Passport Renewal Form - An expedited service is available for urgent requests at an additional cost.

The process of completing a transaction involving a boat often requires careful attention to detail, and a key part of that is utilizing the New York Boat Bill of Sale form. This document not only verifies the transfer of ownership but also safeguards both parties throughout the selling process. For those looking for a reliable source to obtain this form, you can visit https://newyorkpdfdocs.com to ensure all necessary legal requirements are met and to facilitate a smooth transfer.

Florida Realtors Residential Lease - Landlords are prohibited from taking retaliatory or discriminatory actions against tenants under specific conditions.

Here are key takeaways about filling out and using the CG 20 10 07 04 Liability Endorsement form:

To properly complete the CG 20 10 07 04 Liability Endorsement form, gather the necessary information and follow these steps. Ensure that all details are accurate to avoid any issues with your insurance coverage.

After completing the form, submit it to your insurance provider for processing. Keep a copy for your records to ensure you have all necessary documentation related to the endorsement.

The CG 20 10 07 04 Liability Endorsement form serves to add additional insured parties to a commercial general liability policy. This endorsement ensures that specified individuals or organizations are covered for liabilities related to bodily injury, property damage, or personal and advertising injury that may arise from the actions of the insured or their representatives during ongoing operations.

Individuals or organizations listed in the schedule of the endorsement qualify as additional insureds. They are covered only for liabilities resulting from the insured's actions or omissions during the performance of operations at designated locations. The coverage is limited to the extent required by law and any contractual obligations.

Several limitations apply to the coverage provided to additional insureds. Firstly, coverage does not extend to bodily injury or property damage occurring after all work related to the project has been completed. Additionally, if the injury or damage arises after the work has been put to its intended use by someone other than another contractor or subcontractor involved in the project, coverage is not applicable. These limitations ensure that the endorsement does not cover liabilities that arise after the completion of the insured's work.

The endorsement does not increase the overall limits of insurance. If the coverage for an additional insured is mandated by a contract, the maximum amount payable will be the lesser of the amount required by that contract or the limits available under the policy. This stipulation ensures that the coverage aligns with contractual obligations without exceeding the policy limits.

Yes, there are specific exclusions that apply to the coverage for additional insureds. The endorsement explicitly states that it does not cover any bodily injury or property damage occurring after the completion of all work related to the project. Furthermore, it excludes coverage for damages arising from work that has been put to its intended use, unless it involves another contractor or subcontractor engaged in the same project. These exclusions are important for defining the scope of coverage and ensuring clarity in liability responsibilities.

The CG 20 10 07 04 Liability Endorsement form is similar to the CG 20 10 12 19, which is another endorsement that adds additional insureds to a commercial general liability policy. Like the CG 20 10 07 04, it provides coverage for additional insureds with respect to liability for bodily injury, property damage, or personal and advertising injury. Both forms specify that the coverage applies only to the extent of the named insured's acts or omissions and are subject to the same limitations regarding contractual obligations. The key difference lies in the specific conditions and exclusions that may vary between the two endorsements, but the fundamental purpose remains consistent: to extend liability coverage to additional parties involved in a project.

The CG 20 37 10 01 is another endorsement that shares similarities with the CG 20 10 07 04. This endorsement is designed to provide coverage for additional insureds when the named insured is required to do so by a contract. It outlines the scope of coverage, emphasizing that it does not exceed what the contract stipulates. Like the CG 20 10 07 04, it includes exclusions that limit coverage based on the completion of work. Both documents aim to clarify the extent of liability coverage for additional insureds, ensuring that the named insured's obligations are met without exceeding the agreed-upon limits.

The CG 20 10 11 01 endorsement is also relevant as it modifies the insurance policy to include additional insureds. This form specifically addresses coverage for liability arising from the ongoing operations of the named insured. It shares the same core elements as the CG 20 10 07 04, focusing on bodily injury and property damage. Both endorsements limit coverage based on the completion of work and the contractual obligations of the named insured. The CG 20 10 11 01 provides additional clarity on the scope of coverage, making it an essential document for contractors and subcontractors working under specific agreements.

The CG 20 10 03 01 endorsement is another document that parallels the CG 20 10 07 04. This endorsement adds coverage for additional insureds but specifically focuses on completed operations. It is similar in that it provides coverage for bodily injury and property damage arising from the named insured’s work. However, it emphasizes that coverage applies only after the work has been completed, which differs from the ongoing operations focus of the CG 20 10 07 04. Both forms are critical for ensuring that additional insureds have the necessary protection, but they cater to different phases of a project.

The CG 20 10 02 01 endorsement also bears resemblance to the CG 20 10 07 04. This form is used to add additional insureds but focuses on specific locations or projects. Like the CG 20 10 07 04, it provides coverage for bodily injury and property damage but emphasizes the need for proper documentation of the insured locations. Both endorsements ensure that additional insureds are protected under the commercial general liability policy, but the CG 20 10 02 01 adds a layer of specificity regarding where coverage applies.

When dealing with the sale of a motor vehicle in Illinois, it’s crucial to have the appropriate documentation in place to ensure a smooth transaction. The Illinois Motor Vehicle Bill of Sale form serves as a key legal document that confirms the agreement between the seller and buyer. For more detailed information and resources, you can visit Illinois Forms, which provides access to the necessary forms and guidance needed for completing the sale properly.

Lastly, the CG 20 10 04 01 endorsement is similar in that it also addresses additional insureds in the context of liability coverage. This form is particularly focused on liability arising from the actions of subcontractors. Like the CG 20 10 07 04, it specifies the conditions under which the additional insureds are covered, including the requirement for the named insured's acts or omissions. Both endorsements aim to protect additional parties involved in a project, ensuring that liability coverage extends appropriately while adhering to contractual obligations.

The CG 20 10 07 04 Liability Endorsement form is often used in conjunction with various other documents and forms that help clarify coverage, responsibilities, and obligations in insurance policies. Below is a list of some of these related documents, each serving a specific purpose in the context of liability insurance.

Understanding these documents can help individuals and businesses navigate their insurance needs more effectively. Each plays a role in defining coverage and responsibilities, ensuring that all parties are aware of their rights and obligations in the event of a claim.

Misconceptions about the CG 20 10 07 04 Liability Endorsement form can lead to confusion regarding its coverage and implications. Below are seven common misconceptions, along with explanations to clarify them.

Understanding these misconceptions can help ensure that parties involved are aware of the specific terms and limitations of the CG 20 10 07 04 Liability Endorsement form.