Deed of Trust Template

Deed of Trust Template

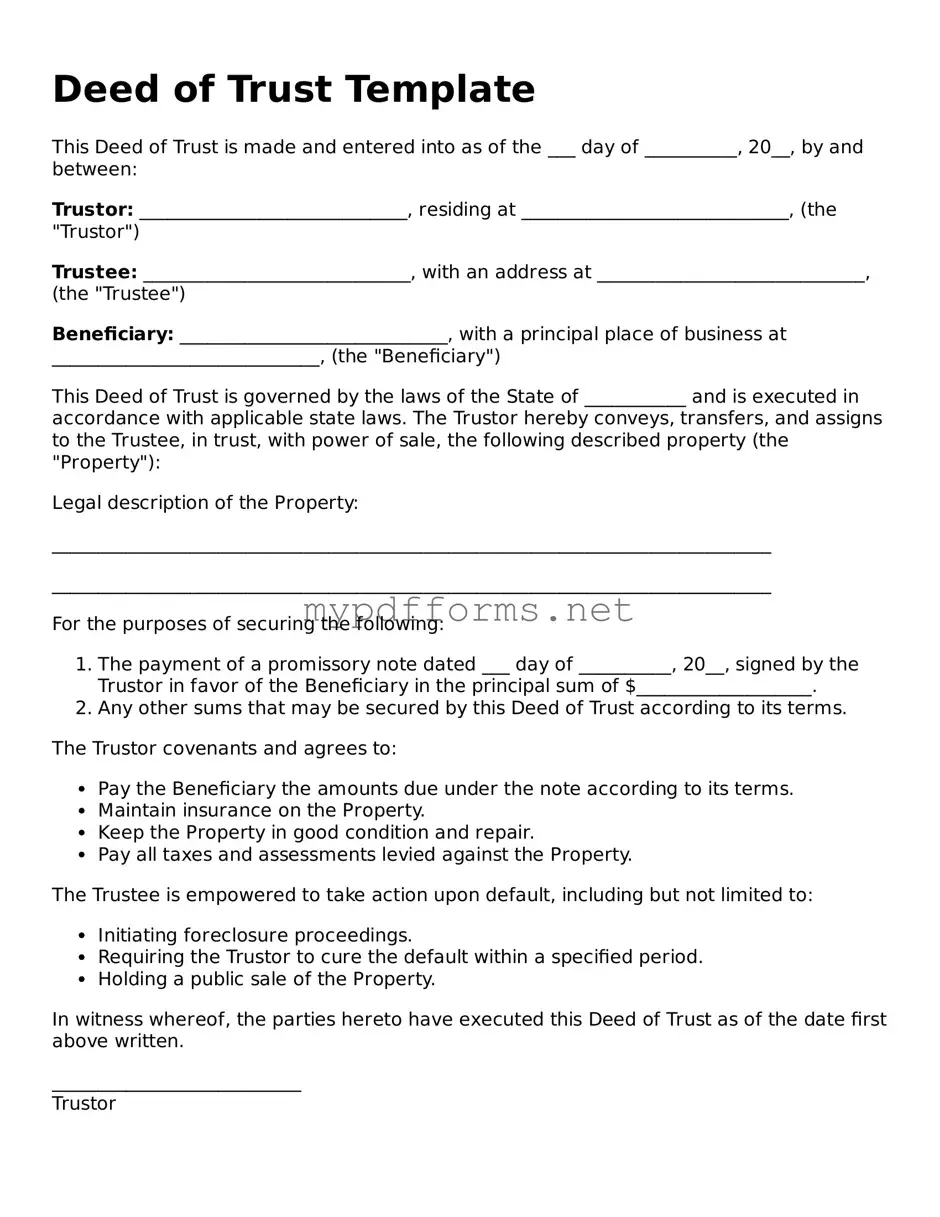

The Deed of Trust form plays a critical role in real estate transactions, serving as a key instrument in securing loans for property purchases. This legal document establishes a three-party agreement between the borrower, the lender, and a neutral third party known as the trustee. It outlines the borrower's obligation to repay the loan while granting the lender a security interest in the property until the debt is satisfied. Key components of the Deed of Trust include the loan amount, the interest rate, and the repayment terms, which specify how and when the borrower must make payments. Additionally, the form details the rights and responsibilities of each party, including what happens in the event of default. By providing a clear framework for the transaction, the Deed of Trust protects the interests of all parties involved and facilitates a smoother lending process. Understanding this document is essential for anyone engaged in real estate, as it influences the ownership and financial responsibilities tied to the property.

When filling out a Deed of Trust form, there are important guidelines to follow. Here are six things to consider:

Life Estate Deed Sample - A Lady Bird Deed can only be created for real estate, making it specific to properties like homes and land.

Before initiating the transfer of ownership, it is essential to understand the requirements and details needed for a Georgia Deed form; for convenience, the form is available here to facilitate the process and ensure all necessary information is captured correctly.

Understanding the Deed of Trust form is crucial for anyone involved in real estate transactions. Here are some key takeaways to keep in mind:

By keeping these points in mind, you can navigate the complexities of the Deed of Trust form more effectively and ensure that your interests are protected.

Filling out the Deed of Trust form is an important step in securing a loan and establishing the terms of the agreement. After completing the form, it will need to be signed and notarized before it can be filed with the appropriate county office. Ensure that all information is accurate and complete to avoid delays in processing.

A Deed of Trust is a legal document used in real estate transactions to secure a loan. It involves three parties: the borrower (trustor), the lender (beneficiary), and a third-party trustee. The borrower transfers the property title to the trustee, who holds it as collateral for the loan until it is paid off. This arrangement provides security for the lender while allowing the borrower to retain possession of the property.

While both a Deed of Trust and a mortgage serve to secure a loan against real estate, they differ in structure and execution. A mortgage involves two parties: the borrower and the lender. In contrast, a Deed of Trust includes a third-party trustee. This trustee has the authority to initiate foreclosure proceedings if the borrower defaults on the loan. This can make the foreclosure process faster and more straightforward with a Deed of Trust compared to a traditional mortgage.

If the borrower defaults on the loan, the trustee has the right to sell the property through a process called non-judicial foreclosure. This means the trustee can proceed with the sale without going through court, making the process quicker. The proceeds from the sale are used to pay off the remaining loan balance, and any excess funds are returned to the borrower. It's important for borrowers to understand their rights and obligations under the Deed of Trust to avoid potential loss of property.

Yes, a Deed of Trust can be modified or refinanced. If a borrower wishes to change the terms of their loan, they may negotiate with the lender to modify the existing Deed of Trust. This could involve adjusting the interest rate, extending the loan term, or changing other terms. Additionally, if a borrower wants to refinance, a new Deed of Trust will typically be created to reflect the new loan. It's essential for borrowers to consult with their lender and possibly a legal professional to ensure that any modifications or refinancing are properly documented.

A mortgage is a common document that serves a similar purpose to a Deed of Trust. Both documents secure a loan by placing a lien on the property. In a mortgage, the borrower retains ownership of the property while the lender has a claim against it until the loan is paid off. Like a Deed of Trust, a mortgage outlines the terms of the loan, including the repayment schedule and interest rate. However, the key difference is that a mortgage typically involves only two parties: the borrower and the lender.

Understanding the nuances of property transfer documents is essential, especially when considering a California Gift Deed form. This legal instrument not only facilitates the gift of property without monetary exchange but also plays a crucial role in protecting the rights of both the giver and the recipient. For those looking to ensure a smooth transaction, accessing the Gift Deed Form can be a helpful starting point.

A promissory note is another document closely related to a Deed of Trust. This note is a written promise from the borrower to repay the loan amount under specified terms. While the Deed of Trust secures the loan with the property, the promissory note details the borrower's obligation to repay. Both documents work together; the Deed of Trust provides security for the lender, while the promissory note outlines the borrower's commitment.

A land contract is similar to a Deed of Trust in that it involves the sale of property where the buyer makes payments over time. In a land contract, the seller retains legal title to the property until the buyer pays the full purchase price. This arrangement protects the seller, similar to how a Deed of Trust protects the lender. Both documents ensure that the buyer has an interest in the property, but the legal ownership remains with the seller until the contract is fulfilled.

A lease agreement can also be compared to a Deed of Trust in terms of securing an interest in property. While a lease does not involve a loan, it grants a tenant the right to occupy and use a property for a specified period in exchange for rent. Similar to a Deed of Trust, a lease agreement outlines the terms and conditions of use. However, in a lease, the landlord retains ownership, while a Deed of Trust involves a loan secured by the property.

An option agreement is another document that shares similarities with a Deed of Trust. This agreement gives a buyer the right, but not the obligation, to purchase property at a predetermined price within a certain timeframe. While the Deed of Trust secures a loan, an option agreement secures the buyer's potential interest in the property. Both documents create a legal interest in the property, although they serve different purposes in the real estate transaction.

A mortgage commitment letter is also related to the Deed of Trust. This letter is issued by a lender to confirm that they are willing to lend a specified amount under certain conditions. It serves as a preliminary agreement before the formal loan documents, including the Deed of Trust, are finalized. Both documents are essential in the loan process, as the commitment letter outlines the lender's terms, while the Deed of Trust secures the loan with the property.

A title insurance policy is another document that shares a connection with a Deed of Trust. While a Deed of Trust secures a loan with the property, title insurance protects the lender and borrower against potential issues with the property's title. Both documents are crucial in real estate transactions, as they help ensure that the lender's investment is protected. Title insurance provides peace of mind, while the Deed of Trust provides a legal claim on the property.

Finally, a quitclaim deed is similar in that it transfers interest in property, but it does not secure a loan like a Deed of Trust. A quitclaim deed allows one party to transfer their interest in a property to another without making any guarantees about the title's validity. While a Deed of Trust is used to secure a loan, a quitclaim deed can be used to transfer ownership or interest in property without a financial transaction. Both documents involve property rights but serve different legal purposes.

A Deed of Trust is a crucial document in real estate transactions, especially when securing a loan. However, it is often accompanied by several other forms and documents that help clarify the terms and protect the interests of all parties involved. Below is a list of commonly used documents that complement the Deed of Trust.

Understanding these documents is essential for anyone involved in a real estate transaction. Each plays a vital role in ensuring a smooth process and protecting the interests of borrowers and lenders alike.

The Deed of Trust form is often misunderstood, leading to confusion for those involved in real estate transactions. Here are four common misconceptions:

While both serve to secure a loan, they are not identical. A mortgage involves two parties: the borrower and the lender. In contrast, a Deed of Trust involves three parties: the borrower, the lender, and a trustee. The trustee holds the title until the loan is repaid, providing an additional layer of security for the lender.

This is a common belief, but in reality, Deeds of Trust are utilized in many states across the U.S. Their usage varies by jurisdiction, but they are not limited to a specific region. Understanding local regulations is key to knowing when a Deed of Trust is appropriate.

Many people think that signing this document grants them ownership. However, the Deed of Trust secures the loan and does not transfer ownership. The borrower retains equitable title, while the lender or trustee holds legal title until the loan is satisfied.

This misconception can create unnecessary anxiety. In fact, a Deed of Trust can be modified, but such changes typically require the agreement of all parties involved. It’s important to consult with a professional if alterations are needed.

Understanding these misconceptions can help individuals navigate the complexities of real estate transactions more effectively.