Get Fl Dr 312 Form in PDF

Get Fl Dr 312 Form in PDF

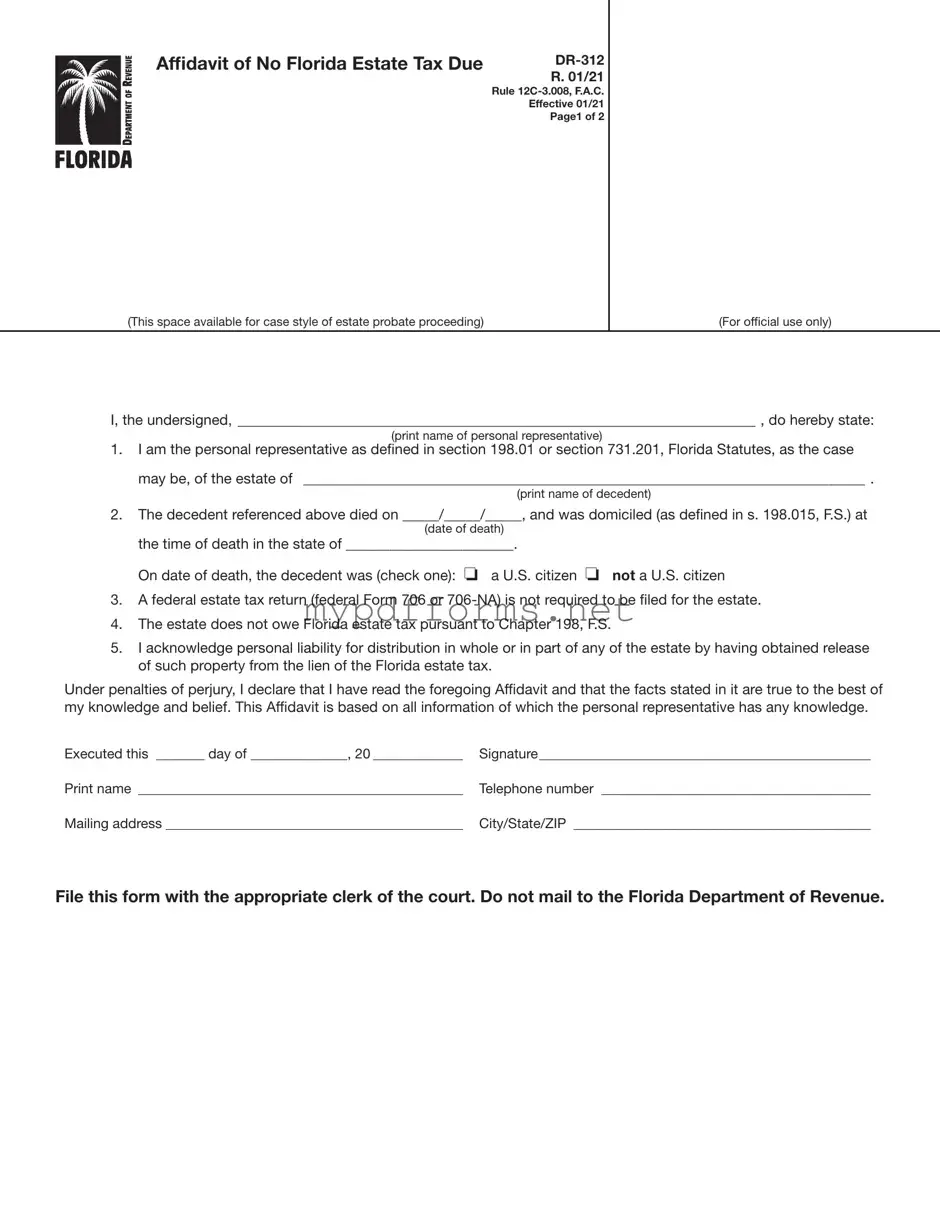

The Florida Form DR-312, officially known as the Affidavit of No Florida Estate Tax Due, serves a crucial role in the probate process for estates that are not subject to Florida estate tax. This form is essential for personal representatives, who are individuals designated to manage the estate of a deceased person. By completing this affidavit, the personal representative affirms that a federal estate tax return is not required and that the estate does not owe any Florida estate tax under Chapter 198 of the Florida Statutes. The form requires specific details, such as the decedent's name, date of death, and their residency status at the time of passing. Notably, it also includes a declaration of personal liability for any distribution of estate property, ensuring that the representative acknowledges their responsibilities. Once filed with the appropriate clerk of the court, this affidavit effectively removes the Florida estate tax lien and serves as evidence of nonliability for estate tax. It is important to note that the DR-312 cannot be used for estates that are required to file a federal Form 706 or 706-NA. Understanding when and how to use this form is vital for personal representatives navigating the complexities of estate management in Florida.

When completing the Florida DR-312 form, there are important guidelines to follow. Here is a list of things you should and shouldn't do:

Abn for Medicare - By issuing this notice, providers demonstrate their commitment to patient education.

In order to comply with state regulations and ensure lawful firearm possession, it is essential for applicants to be familiar with the required documentation, including the Illinois Application for Firearm Control Card. For more information on obtaining this application, you can visit Illinois Forms, which provide essential resources and guidance for prospective applicants in navigating the application process effectively.

What Is a Verification Form - Landlords retain the right to approve or deny applications based on this form.

Here are some important points to consider when filling out and using the Florida DR-312 form:

It is essential to follow these guidelines carefully to ensure compliance and avoid potential issues with estate tax obligations.

After gathering the necessary information, the next step involves accurately completing the Florida Form DR-312. This form must be filed with the appropriate clerk of the circuit court in the county where the decedent owned property. It is essential to ensure that all sections are filled out correctly to avoid delays in processing.

Once completed, file the form with the clerk of the circuit court. Do not mail it to the Florida Department of Revenue. Ensure that all information is accurate to facilitate a smooth filing process.

What is the purpose of the FL DR 312 form?

The FL DR 312 form, also known as the Affidavit of No Florida Estate Tax Due, is used to declare that an estate does not owe any Florida estate tax. It is necessary when a federal estate tax return is not required to be filed. This form serves as evidence of nonliability for Florida estate tax and helps to remove the Department's estate tax lien.

Who should file the FL DR 312 form?

The personal representative of the estate, as defined in Florida Statutes, should file the FL DR 312 form. This includes any person in actual or constructive possession of the decedent's property. Individuals who manage the estate or have control over the decedent's assets may also use this form.

When should the FL DR 312 form be used?

This form should be used when an estate is not subject to Florida estate tax under Chapter 198 of the Florida Statutes, and when a federal estate tax return (Form 706 or 706-NA) is not required. It is important to confirm that the estate meets these criteria before filing.

Where should the FL DR 312 form be filed?

The FL DR 312 form must be filed with the clerk of the circuit court in the county or counties where the decedent owned property. It should not be mailed to the Florida Department of Revenue.

What information is required on the FL DR 312 form?

The form requires the name of the personal representative, the name of the decedent, the date of death, the state of domicile at the time of death, and whether the decedent was a U.S. citizen. Additionally, the personal representative must acknowledge personal liability for the distribution of the estate.

What are the consequences of filing the FL DR 312 form?

Filing the FL DR 312 form removes the estate tax lien imposed by the Florida Department of Revenue. It also serves as proof that the estate is not liable for Florida estate tax, which can facilitate the distribution of assets to beneficiaries.

What happens if the estate is required to file a federal estate tax return?

The FL DR 312 form cannot be used if the estate is required to file a federal estate tax return (Form 706 or 706-NA). In such cases, the personal representative must comply with federal filing requirements instead.

How can I contact the Florida Department of Revenue for assistance?

For assistance, individuals can call Taxpayer Services at 850-488-6800, Monday through Friday, excluding holidays. Additional information and resources are available on the Department's website at floridarevenue.com.

Are there any specific filing deadlines for the FL DR 312 form?

There are no specific deadlines mentioned for filing the FL DR 312 form. However, it is advisable to file it promptly after determining that the estate does not owe any Florida estate tax and that no federal estate tax return is required.

The Affidavit of No Florida Estate Tax Due (Form DR-312) shares similarities with the IRS Form 706, the United States Estate (and Generation-Skipping Transfer) Tax Return. Both forms serve to clarify the tax obligations of an estate following a decedent's passing. While Form 706 is used when the estate exceeds certain value thresholds and requires federal estate tax filing, Form DR-312 is utilized when no federal estate tax return is necessary. The completion of either form involves the personal representative affirming the estate's tax status, underscoring the importance of accurate reporting in estate administration.

Another related document is the IRS Form 706-NA, which is specifically for non-resident aliens. This form is similar to Form DR-312 in that it addresses tax obligations following a decedent's death. However, while Form 706-NA is required for estates of non-resident aliens that meet specific criteria, Form DR-312 is designed for Florida estates that do not owe state tax. Both forms require the personal representative to assert the estate's tax status, but they cater to different circumstances based on the decedent's residency.

The Florida Department of Revenue's Nontaxable Certificate is also comparable to Form DR-312. This certificate historically served as proof that an estate was not subject to Florida estate tax. However, with the introduction of Form DR-312, the issuance of Nontaxable Certificates has been discontinued. Both documents aimed to provide assurance regarding tax liabilities, but the DR-312 has streamlined the process for estates that do not owe taxes, thus eliminating the need for a separate certificate.

The Affidavit of Heirship is another document that bears resemblance to Form DR-312. This affidavit is often used to establish the heirs of a decedent's estate when there is no will. Like Form DR-312, the Affidavit of Heirship requires a personal representative to affirm the validity of the claims made regarding the estate. Both documents serve important roles in the probate process, ensuring clarity and legal standing for the distribution of assets.

Additionally, the Florida Probate Court's Petition for Summary Administration is similar to Form DR-312 in that it addresses the administration of estates that may not require full probate proceedings. This petition is used for smaller estates, allowing for a quicker resolution. Both documents facilitate the process of settling an estate, but the Petition for Summary Administration is specifically for cases that meet certain criteria, whereas Form DR-312 is focused on tax liability.

The Certificate of Discharge from Personal Representative is another document that has parallels with Form DR-312. This certificate is issued when a personal representative has completed their duties and is released from further obligations. Both documents signify a conclusion in the estate administration process, with Form DR-312 confirming that no estate taxes are owed, while the Certificate of Discharge signifies that the personal representative has fulfilled their responsibilities.

The Affidavit of Small Estate is also comparable to Form DR-312. This affidavit allows for the simplified transfer of assets when an estate meets certain value limits. Similar to Form DR-312, it is used when the estate does not have complex tax obligations. Both documents aim to streamline the process of settling estates, providing a more efficient means of transferring property to heirs.

The Last Will and Testament itself can be viewed as related to Form DR-312, as it outlines the decedent's wishes regarding asset distribution. While the will does not directly address tax obligations, it sets the framework for how the estate will be managed and distributed. Both documents play critical roles in the probate process, with the will dictating the distribution and Form DR-312 confirming the tax status of the estate.

For individuals involved in motorcycle transactions, understanding the importance of the Georgia Motorcycle Bill of Sale is essential; it serves as a reliable proof of ownership transfer, covering essential details like the motorcycle's make and VIN. As part of this process, it is advisable to utilize resources such as the motorcyclebillofsale.com/free-georgia-motorcycle-bill-of-sale to ensure all documentation is complete and compliant with state regulations.

Lastly, the Petition for Letters of Administration is similar to Form DR-312 in that it initiates the probate process. This petition is filed to appoint a personal representative to manage the estate. Both documents are essential in ensuring that the estate is handled according to legal requirements, with the petition establishing the representative's authority and Form DR-312 addressing tax liabilities.

When dealing with estate matters in Florida, several forms and documents accompany the Affidavit of No Florida Estate Tax Due (Form DR-312). Each of these documents serves a specific purpose in the probate process, ensuring that all necessary legal steps are followed properly. Below is a brief overview of some commonly used forms alongside the DR-312.

Understanding these forms and their purposes can help facilitate the probate process. Each document plays a crucial role in ensuring that the estate is handled according to the law, protecting the interests of the decedent's heirs and beneficiaries. It is essential to approach these matters with care and attention to detail to ensure a smooth resolution.

Understanding the Fl Dr 312 form is crucial for personal representatives managing estates in Florida. However, several misconceptions can lead to confusion. Here are five common misunderstandings about this form:

This is incorrect. The Fl Dr 312 form should be filed directly with the clerk of the circuit court in the county where the decedent owned property. Do not mail it to the Florida Department of Revenue.

This is not true. The Fl Dr 312 form should only be used when a federal estate tax return (Form 706 or 706-NA) is not required to be filed. If such a return is needed, this form is not applicable.

While the Fl Dr 312 serves as evidence of nonliability for Florida estate tax, it does not automatically guarantee that there will be no estate tax due. It is essential to ensure that all conditions for its use are met.

Only the personal representative, as defined by Florida law, can file this form. This includes individuals in actual or constructive possession of the estate's property.

This is a misconception. The Fl Dr 312 must be duly recorded in the public records of the county or counties where the decedent owned property to be effective.

By clarifying these misconceptions, personal representatives can navigate the process more smoothly and ensure compliance with Florida estate tax regulations.