Attorney-Verified Loan Agreement Document for Florida

Attorney-Verified Loan Agreement Document for Florida

When individuals or businesses in Florida seek to borrow money, a Loan Agreement form becomes an essential document that outlines the terms and conditions of the loan. This form serves as a written record of the agreement between the lender and the borrower, detailing crucial aspects such as the loan amount, interest rate, repayment schedule, and any collateral involved. Additionally, it specifies the rights and responsibilities of both parties, ensuring that everyone understands their obligations. By clearly defining the duration of the loan and the consequences of default, this form helps protect both the lender's investment and the borrower's interests. It also may include provisions for late fees, prepayment options, and any applicable state laws that govern the lending process. Understanding these components is vital for anyone looking to navigate the borrowing landscape in Florida effectively.

When filling out the Florida Loan Agreement form, there are some important dos and don'ts to keep in mind. Following these guidelines can help ensure that your form is completed correctly and efficiently.

By following these simple guidelines, you can help make the process smoother and avoid potential issues later on.

Promissory Note Template New York - A competent Loan Agreement lays the foundation for a healthy lending experience.

When engaging in the sale of a motorcycle in Georgia, it is important to have a comprehensive understanding of the Georgia Motorcycle Bill of Sale form, which can be found at https://motorcyclebillofsale.com/free-georgia-motorcycle-bill-of-sale. This document is essential for ensuring that the transfer of ownership is well-documented and legally sound, providing protection for both the buyer and the seller throughout the transaction.

Texas Promissory Note Form - Understanding the consequences of missed payments highlighted in the agreement is crucial.

Free Promissory Note Template California - Borrowers should seek clarity on any ambiguous terms within the agreement.

When filling out and using the Florida Loan Agreement form, keep these key takeaways in mind:

By following these guidelines, you can create a clear and effective Loan Agreement that serves both parties well.

Completing the Florida Loan Agreement form is an important step in formalizing a loan between parties. After filling out the form, both parties will have a clear understanding of the terms and conditions of the loan, which can help prevent misunderstandings in the future. Follow the steps below to ensure that the form is filled out correctly.

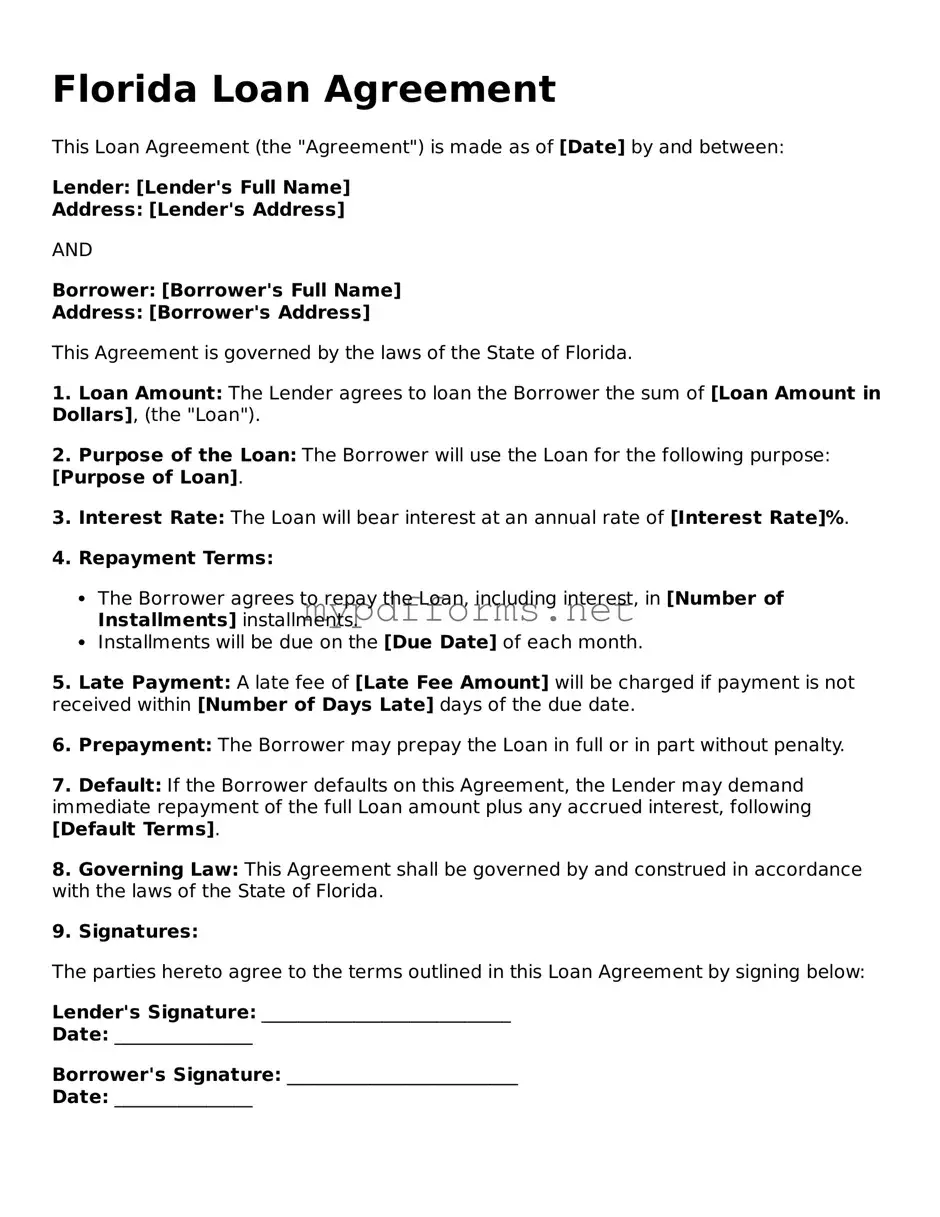

A Florida Loan Agreement is a legal document that outlines the terms and conditions of a loan between a lender and a borrower in the state of Florida. This agreement specifies the loan amount, interest rate, repayment schedule, and any collateral involved. It serves to protect the interests of both parties and provides a clear framework for the loan transaction.

Both individuals and businesses can use a Florida Loan Agreement. If you are lending money to a friend, family member, or business associate, it is wise to have a written agreement. This document helps avoid misunderstandings and provides legal recourse if the borrower fails to repay the loan.

A typical Florida Loan Agreement includes:

Yes, a properly executed Florida Loan Agreement is legally binding. Both parties must sign the document, and it should include all necessary terms. If either party fails to adhere to the agreement, the other party may seek legal remedies.

While it is not mandatory to hire a lawyer, it is advisable, especially for larger loans or more complex agreements. A legal professional can ensure that the document complies with Florida laws and adequately protects your interests.

Yes, modifications can be made to a Florida Loan Agreement after it has been signed, but both parties must agree to the changes. It is best to document any modifications in writing and have both parties sign the amended agreement.

If the borrower defaults, the lender may take legal action to recover the owed amount. The specifics of the default terms, including any penalties or fees, should be outlined in the Loan Agreement. Collateral may also be seized if it was included in the agreement.

Yes, Florida has specific laws governing loans, including interest rate limits and consumer protection regulations. It is essential to be aware of these laws to ensure compliance and avoid potential legal issues.

Templates for Florida Loan Agreements can be found online through various legal websites. However, ensure that the template you choose is up-to-date and complies with Florida laws. Consider consulting with a legal professional to customize the agreement to your specific needs.

The Florida Loan Agreement form shares similarities with a Personal Loan Agreement. Both documents outline the terms and conditions under which money is borrowed. They specify the loan amount, interest rates, repayment schedules, and the obligations of both the lender and the borrower. Personal Loan Agreements are typically used for unsecured loans, while the Florida Loan Agreement may also encompass secured loans, depending on the circumstances. Each agreement aims to protect the interests of both parties while ensuring clarity in the lending process.

Another document that resembles the Florida Loan Agreement is the Mortgage Agreement. This type of agreement is specifically related to real estate transactions. It details the terms under which a borrower receives funds to purchase property, using the property itself as collateral. Like the Florida Loan Agreement, it includes information on interest rates, repayment terms, and the consequences of default. Both documents serve to formalize the lending process and protect the lender’s investment.

A Business Loan Agreement is another similar document. This agreement is used when a business seeks financing from a lender. It outlines the terms of the loan, including the amount, interest rates, and repayment schedule. The Florida Loan Agreement and Business Loan Agreement both aim to ensure that the lender’s and borrower’s rights and responsibilities are clearly defined. Each document is tailored to the specific needs of the borrower, whether an individual or a business entity.

The Promissory Note is closely related to the Florida Loan Agreement as well. This document serves as a written promise from the borrower to repay a specified amount of money to the lender. While the Loan Agreement often contains more detailed terms and conditions, the Promissory Note focuses primarily on the promise to pay. Both documents are essential in establishing a legal obligation between the parties involved in the loan.

A Secured Loan Agreement is also similar to the Florida Loan Agreement. In this type of agreement, the borrower offers collateral to the lender, which can be seized if the borrower defaults on the loan. Both documents detail the loan amount, interest rates, and repayment terms, but the Secured Loan Agreement emphasizes the collateral aspect. This added layer of security for the lender is a key difference that can affect the terms of the loan.

In real estate transactions, understanding the various legal documents involved is crucial, and one important form to be aware of is the Quitclaim Deed, as it facilitates the transfer of property ownership without warranties. For those interested in a comprehensive overview, detailed information can be found at https://floridapdfform.com/, which provides access to printable forms and additional resources related to real estate conveyancing in Florida.

The Installment Loan Agreement bears resemblance to the Florida Loan Agreement as well. This document specifies a loan that is repaid through a series of scheduled payments over time. Both agreements outline the total loan amount, interest rates, and payment frequency. The Installment Loan Agreement, like the Florida Loan Agreement, aims to provide clear expectations for both the borrower and the lender regarding repayment.

A Credit Agreement is another document that shares similarities with the Florida Loan Agreement. This agreement outlines the terms under which credit is extended to a borrower. It includes details about the credit limit, interest rates, and repayment terms. Both the Credit Agreement and the Florida Loan Agreement serve to protect the lender’s interests while providing the borrower with a clear understanding of their obligations.

The Loan Modification Agreement is also comparable to the Florida Loan Agreement. This document is used when the terms of an existing loan need to be changed, often due to financial hardship. It outlines the new terms, including any adjustments to the interest rate or repayment schedule. Like the Florida Loan Agreement, it aims to ensure that both parties understand their rights and responsibilities under the modified terms.

The Lease Agreement is another document that, while serving a different purpose, shares structural similarities with the Florida Loan Agreement. A Lease Agreement outlines the terms under which a tenant rents property from a landlord. Both documents detail the obligations of each party, including payment terms and conditions for default. The clarity provided in both agreements helps to foster a positive relationship between the parties involved.

Lastly, the Loan Application is related to the Florida Loan Agreement in that it initiates the lending process. This document collects essential information from the borrower, including their financial history and creditworthiness. While the Loan Application does not finalize the terms of the loan, it is a critical step that leads to the creation of a Loan Agreement, such as the Florida Loan Agreement. Both documents work together to ensure that the lending process is transparent and fair.

When entering into a loan agreement in Florida, it's essential to understand that several other forms and documents may accompany the main agreement. These documents serve various purposes, from ensuring clarity in the terms to providing legal protections for both parties involved. Here’s a brief overview of some commonly used forms alongside the Florida Loan Agreement.

Understanding these accompanying documents can significantly enhance your experience when navigating a loan agreement. Being informed helps ensure that both parties are protected and that the terms of the loan are clear and fair. Always consider consulting with a legal professional to ensure that all necessary documents are in order and that your interests are adequately safeguarded.

When it comes to the Florida Loan Agreement form, several misconceptions often arise. Understanding these can help borrowers and lenders navigate the loan process more effectively. Here are four common misunderstandings:

By clarifying these misconceptions, individuals can approach the loan process with a better understanding and greater confidence.