Attorney-Verified Promissory Note Document for Florida

Attorney-Verified Promissory Note Document for Florida

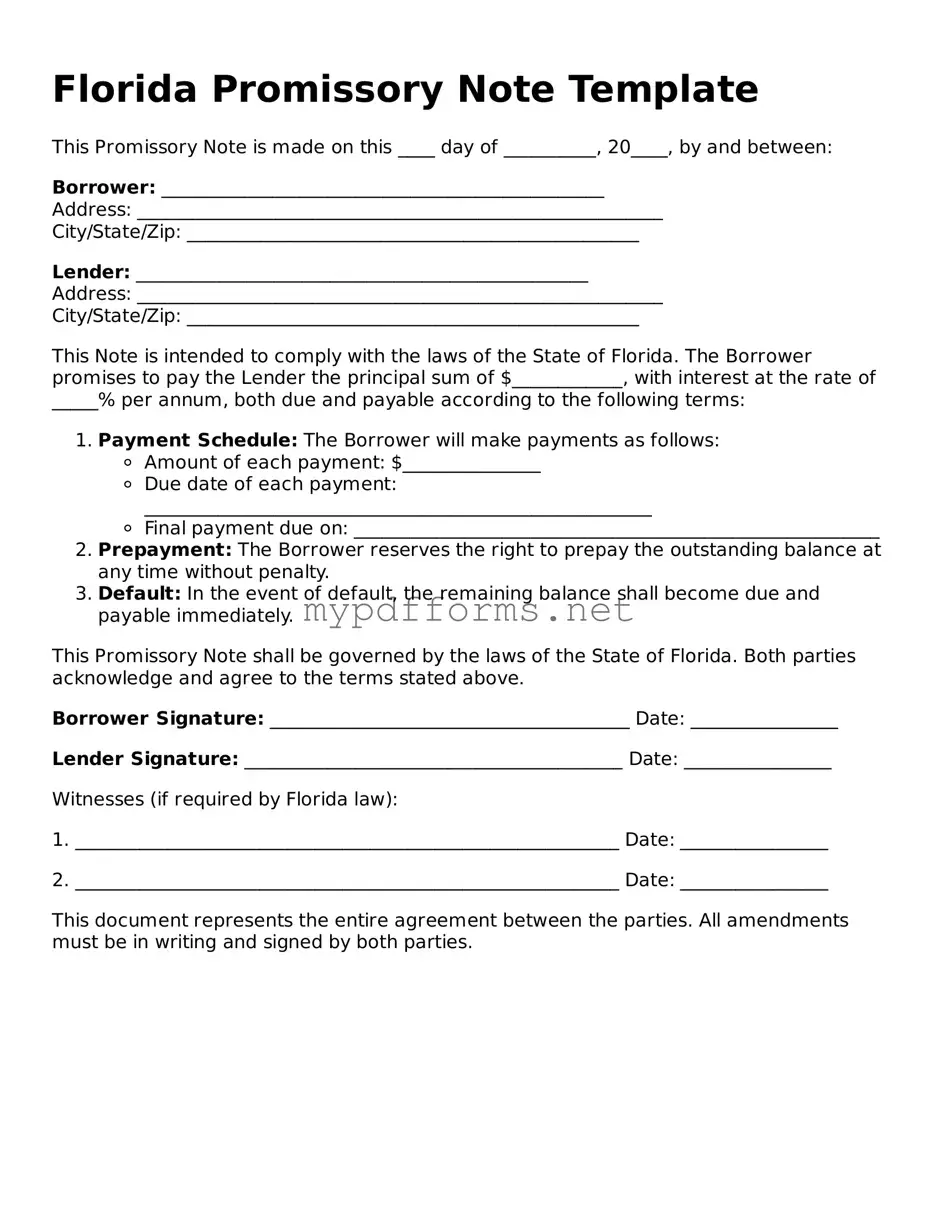

In Florida, a Promissory Note serves as a crucial document in lending agreements, outlining the terms of a loan between a borrower and a lender. This written promise details the amount borrowed, the interest rate, and the repayment schedule, providing clarity and security for both parties involved. The form typically includes essential elements such as the names and addresses of the borrower and lender, the loan amount, and any applicable fees or penalties for late payments. Additionally, it may specify the consequences of defaulting on the loan, which can include legal action or the seizure of collateral if applicable. Understanding the Florida Promissory Note form is vital for anyone entering into a loan agreement, as it not only protects the lender’s interests but also informs the borrower of their obligations. Whether you are a first-time borrower or a seasoned lender, being familiar with this form can help ensure a smooth transaction and prevent potential disputes down the line.

When filling out the Florida Promissory Note form, it's important to approach the task with care. Here are some essential dos and don'ts to keep in mind:

New York Promissory Note - Some notes may include clauses for early repayment without penalty.

Completing a Last Will and Testament is crucial for ensuring that your wishes regarding asset distribution and care for dependents are clearly stated. For residents in Illinois, utilizing resources such as Illinois Forms can simplify the process of creating this important legal document, ensuring that it meets all necessary legal requirements.

Free Promissory Note Template California - A borrower has the right to ask questions before signing the document.

When dealing with a Florida Promissory Note, understanding the essential elements can significantly impact the effectiveness of the document. Here are some key takeaways to consider:

Once you have the Florida Promissory Note form in front of you, it’s time to fill it out accurately. This form is essential for outlining the terms of a loan between the lender and the borrower. Follow the steps below to complete the form correctly.

After filling out the form, review it for accuracy. Each detail matters, as they form the basis of the agreement between the parties involved. Ensure that both the lender and borrower retain copies for their records.

A Florida Promissory Note is a legal document in which one party (the borrower) agrees to pay a specific amount of money to another party (the lender) under agreed-upon terms. This document outlines the amount borrowed, the interest rate, the repayment schedule, and any other conditions related to the loan.

Individuals and businesses commonly use Promissory Notes. They are often utilized in personal loans, business loans, or real estate transactions. Both lenders and borrowers benefit from having a written agreement, as it provides clarity and legal protection for both parties.

A well-drafted Florida Promissory Note typically includes the following elements:

Yes, a Promissory Note is a legally binding contract. Once signed by both parties, it obligates the borrower to repay the loan under the terms specified. If the borrower fails to repay, the lender has the right to take legal action to recover the owed amount.

While it is not mandatory to have a lawyer draft a Promissory Note, it is advisable to seek legal guidance, especially for larger loans or complex agreements. A legal professional can ensure that the document complies with Florida laws and meets the specific needs of both parties.

Yes, a Promissory Note can be modified if both the borrower and lender agree to the changes. It is essential to document any modifications in writing and have both parties sign the amended agreement to ensure clarity and legal enforceability.

If the borrower defaults, the lender can take several actions, including demanding full repayment, charging late fees, or pursuing legal action to recover the owed amount. The specific consequences should be outlined in the Promissory Note itself, so both parties understand their rights and obligations.

A loan agreement is quite similar to a promissory note. Both documents outline the terms of a loan, including the amount borrowed and the repayment schedule. However, a loan agreement typically includes more detailed terms, such as collateral and the rights of both parties. While a promissory note is a simpler document that focuses on the promise to repay, a loan agreement provides a broader framework for the loan transaction.

A mortgage is another document that shares similarities with a promissory note. When someone borrows money to buy a home, they often sign both a mortgage and a promissory note. The promissory note serves as the borrower’s promise to repay the loan, while the mortgage secures the loan with the property itself. This means that if the borrower fails to repay, the lender can take possession of the home.

A deed of trust functions in a similar way to a mortgage but involves a third party, known as a trustee. In this case, the promissory note represents the borrower’s commitment to repay the loan. The deed of trust secures that loan by giving the trustee the right to sell the property if the borrower defaults. This arrangement can simplify the foreclosure process for lenders.

The Minnesota Motorcycle Bill of Sale form is an essential document for anyone looking to buy or sell a motorcycle in Minnesota, providing critical details regarding the motorcycle and the involved parties. Familiarity with this form ensures that all necessary information is captured during the transaction. For those needing assistance or a template, the free resource found at https://motorcyclebillofsale.com/free-minnesota-motorcycle-bill-of-sale/ can be very helpful.

An IOU is a more informal version of a promissory note. It simply acknowledges that one person owes money to another. While an IOU may not contain all the legal details found in a promissory note, it still establishes a debt. Both documents serve the purpose of recording a debt, but an IOU lacks the same level of legal enforceability.

A personal guarantee is another document that can complement a promissory note. When a borrower is unable to secure a loan based on their creditworthiness alone, a lender might require a personal guarantee. This document means that a third party agrees to repay the loan if the borrower defaults. The promissory note remains the primary document outlining the loan terms, while the personal guarantee adds an extra layer of security for the lender.

A business loan agreement is similar to a promissory note but is tailored for business purposes. This document outlines the terms of a loan made to a business rather than an individual. Like a promissory note, it includes the loan amount and repayment terms, but it may also detail how the funds can be used and any specific conditions tied to the loan.

A credit agreement is another related document. This agreement outlines the terms under which a borrower can access credit from a lender. While a promissory note is focused on a specific loan, a credit agreement may allow for multiple borrowings over time. Both documents establish the borrower’s obligation to repay, but the credit agreement provides a broader framework for ongoing financial transactions.

A lease agreement can also bear similarities to a promissory note in certain contexts. When leasing property, a lease agreement outlines the terms of payment and responsibilities of both parties. If a lease includes a promise to pay rent, it operates in a similar manner to a promissory note. Both documents create obligations that can be enforced by the parties involved.

Lastly, a settlement agreement can be compared to a promissory note when it involves a payment plan. In cases where parties settle a dispute, a settlement agreement may outline a payment schedule similar to that found in a promissory note. Both documents formalize the terms of repayment, ensuring that all parties understand their obligations moving forward.

When dealing with a Florida Promissory Note, several other forms and documents may be necessary to ensure clarity and protection for all parties involved. Understanding these documents can help facilitate a smoother transaction. Below is a list of commonly used forms that often accompany a Promissory Note.

These documents work together to create a comprehensive framework for the lending arrangement. Having them in place can help prevent misunderstandings and protect the interests of both the lender and borrower.

Understanding the Florida Promissory Note form can be challenging, especially with the various misconceptions that exist. Here are ten common misunderstandings about this important document:

Many believe that all promissory notes are identical. In reality, each note can be tailored to fit specific agreements between the parties involved.

While both documents relate to borrowing money, a promissory note focuses on the borrower's promise to repay, whereas a loan agreement outlines the terms of the loan in greater detail.

This is not true. Promissory notes can be used in business transactions, real estate deals, and more, not just personal loans.

Simply signing the note does not guarantee enforceability. Proper documentation and compliance with state laws are crucial.

While it is common to include an interest rate, it is not mandatory. A note can be interest-free if the parties agree.

Notarization can add an extra layer of legitimacy, but it is not a requirement for a promissory note to be valid in Florida.

Promissory notes can be used for any amount, big or small. They are a flexible option for various financial agreements.

Not all notes are enforceable. Factors such as lack of consideration or illegal terms can void a promissory note.

While the original terms are binding, parties can mutually agree to modify the note later, as long as changes are documented.

Borrowers can draft promissory notes as well. It is important for both parties to understand the terms before signing.

By dispelling these misconceptions, individuals can better navigate the complexities of promissory notes in Florida and ensure their agreements are clear and enforceable.