Get Gift Letter Form in PDF

Get Gift Letter Form in PDF

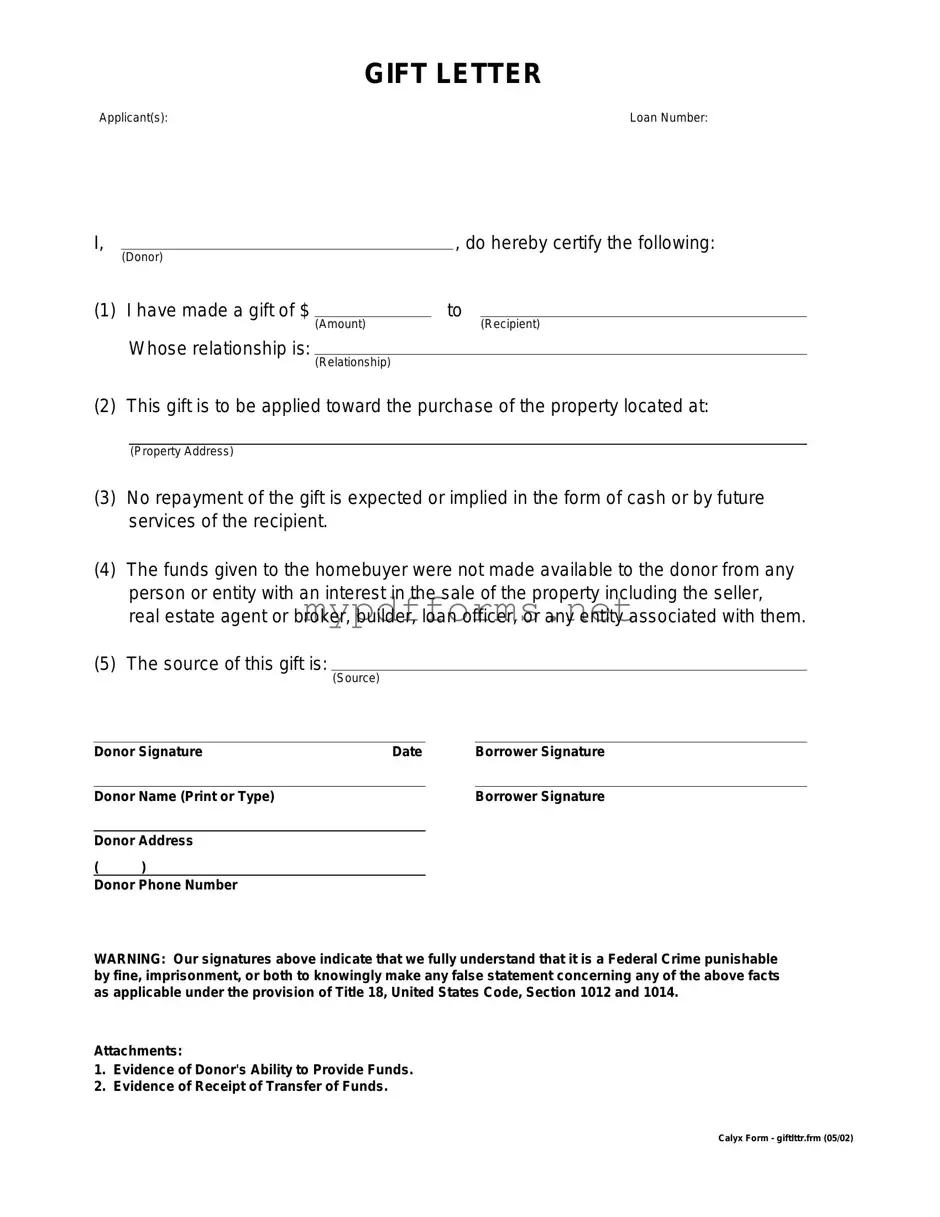

The Gift Letter form plays a crucial role in the realm of financial transactions, particularly when it comes to real estate purchases and securing loans. This document serves as a formal declaration that a monetary gift is being provided to the recipient, typically from a family member or close friend, to assist with a down payment or other costs associated with buying a home. By clearly outlining the nature of the gift, the form helps to establish that the funds do not require repayment, distinguishing them from loans. This clarity is essential for lenders, as they need assurance that the borrower has sufficient financial stability without the burden of additional debt. Furthermore, the Gift Letter form usually includes details such as the donor's relationship to the recipient, the amount of the gift, and a statement confirming that no repayment is expected. By providing this information, the form not only supports the loan application process but also helps to protect both parties by documenting the transaction. Overall, understanding and properly utilizing the Gift Letter form can significantly ease the path to homeownership for many individuals and families.

When filling out a Gift Letter form, it's important to follow certain guidelines to ensure clarity and compliance. Here’s a list of dos and don’ts:

Chicago Title Lien Waiver - Details any remaining balance owed for completed work after current payments.

The Illinois Motorcycle Bill of Sale form is a legal document that records the details of a transaction when buying or selling a motorcycle in Illinois. It ensures that the transfer of ownership is recognized by law and provides a record of the sale for both parties. For those looking to make their motorcycle sale official, fill out the form by clicking the button below or visit Illinois Forms for more information.

Da Form 2823 - Disclosure of information on the DA 2823 may contribute to the Army’s processes for recruitment and retention.

How Do You Know You Had a Miscarriage - The form reflects a commitment to transparency concerning the management of fetal remains.

Gift letters are essential for documenting the transfer of funds from a donor to a recipient, particularly in real estate transactions.

Ensure that all necessary information is included, such as the donor's name, the recipient's name, the amount of the gift, and the relationship between the two parties.

It is important for the donor to explicitly state that the funds are a gift and do not require repayment, as this can affect loan eligibility for the recipient.

Both the donor and recipient should sign the gift letter to validate the transaction and provide a clear record for financial institutions.

When preparing to fill out the Gift Letter form, it is essential to ensure that all information is accurate and complete. This form is often required during financial transactions, such as purchasing a home, to confirm that the funds being gifted do not need to be repaid. Following the steps below will help streamline the process and ensure everything is in order.

Once the form is filled out and signed, it can be submitted as part of the required documentation for the relevant financial transaction. Ensuring that all details are accurate will help facilitate a smooth process.

A Gift Letter form is a document that verifies a monetary gift given to a borrower for a home purchase. This letter serves to confirm that the funds are a gift and not a loan, ensuring that the recipient does not have to repay the money. It is often required by lenders during the mortgage application process.

Usually, a family member or close friend provides a Gift Letter. The person giving the gift must be someone who has a personal relationship with the borrower. This could include parents, siblings, or even grandparents.

A Gift Letter should include the following details:

While there is no strict format, the letter should be clear and concise. It should be written in a professional tone. Many lenders provide a template or specific guidelines to follow, which can be helpful.

Yes, lenders often require proof of the gift. This may include bank statements showing the transfer of funds or a copy of the check. The Gift Letter itself serves as a formal declaration, but additional documentation may be necessary.

Gift Letters are most commonly used for mortgage loans, particularly when purchasing a home. However, some lenders may allow gift funds for other types of loans. It is essential to check with the specific lender to understand their policies.

If a Gift Letter is not provided, the lender may consider the funds as a loan, which could affect the borrower’s debt-to-income ratio. This may lead to complications in the loan approval process. Therefore, it is crucial to provide the letter as part of the mortgage application.

Yes, there can be tax implications for the donor. The IRS allows individuals to gift a certain amount each year without incurring gift tax. As of 2023, this limit is $17,000 per recipient. It is advisable for the donor to consult a tax professional for guidance on their specific situation.

The Gift Letter form is closely related to the Affidavit of Support. This document is often used when an individual sponsors a foreign national seeking a visa. It serves to demonstrate that the sponsor has sufficient financial resources to support the visa applicant. Both documents require a declaration of funds, ensuring that the recipient will not become a public charge. This similarity emphasizes the importance of financial stability in both personal and immigration contexts.

Another document similar to the Gift Letter is the Bank Statement. This financial document provides a detailed overview of an individual’s account activity over a specific period. Like the Gift Letter, a Bank Statement can be used to show proof of funds. It offers transparency regarding financial resources, which is crucial in both lending and gifting scenarios.

The Loan Agreement also shares similarities with the Gift Letter. This document outlines the terms and conditions under which a loan is provided. While a Loan Agreement involves repayment, both documents require a clear statement of the funds involved. They highlight the importance of financial accountability, whether in a gift or a loan situation.

The Promissory Note is another document that resembles the Gift Letter. A Promissory Note is a written promise to pay a specified amount of money to a designated party. Both documents require the acknowledgment of the transfer of funds. However, the key difference lies in the expectation of repayment in a Promissory Note, while a Gift Letter indicates a gift with no strings attached.

The Statement of Assets is similar to the Gift Letter in that it provides a comprehensive overview of an individual's financial situation. This document lists all assets and liabilities, giving a clear picture of one’s net worth. Both documents can be used to establish financial stability, whether for personal transactions or loan applications.

The Financial Gift Declaration is another document akin to the Gift Letter. This declaration explicitly states that a financial gift has been made, often for tax purposes. Like the Gift Letter, it requires the donor to confirm that the funds are a gift and not a loan. This ensures clarity in the nature of the transaction, which is important for both parties.

The Tax Return can also be compared to the Gift Letter. While a Tax Return details an individual's income and tax obligations, it can also reflect financial gifts received. Both documents serve as evidence of financial transactions and can be important in assessing an individual’s financial health, particularly when applying for loans or mortgages.

The Gift Tax Return is closely related to the Gift Letter. This document is filed with the IRS to report gifts exceeding a certain value. Similar to the Gift Letter, it requires the donor to disclose the amount gifted. Both documents are essential for tax compliance and help clarify the nature of financial transfers between individuals.

When dealing with the sale of a motorcycle, it's essential to have the proper documentation in place, such as the North Carolina Motorcycle Bill of Sale. This legal form ensures the transaction is recorded accurately, offering peace of mind to both buyer and seller. To assist in this process, you can find a comprehensive resource at motorcyclebillofsale.com/free-north-carolina-motorcycle-bill-of-sale, which provides guidelines and a downloadable template to help streamline the transfer of ownership.

Lastly, the Mortgage Application often requires a Gift Letter as part of the documentation. When a borrower receives a gift to help with a down payment, the lender may request a Gift Letter to confirm the funds are not a loan. Both documents aim to ensure that financial support is clearly understood, protecting both the lender and the borrower in the transaction.

The Gift Letter form is an essential document used primarily in real estate transactions, especially when a buyer receives financial assistance from a family member or friend to help with a down payment. However, several other forms and documents often accompany the Gift Letter to provide additional information and ensure transparency in the transaction. Below is a list of these commonly used documents.

Understanding these accompanying documents is crucial for both donors and recipients to ensure a smooth transaction. Each document plays a role in clarifying the financial relationship and ensuring compliance with applicable regulations. Properly managing these forms can help facilitate the home-buying process and protect the interests of all parties involved.

When it comes to the Gift Letter form, many people hold misconceptions that can lead to confusion. Here are seven common misunderstandings:

Many believe that Gift Letters are only necessary for significant financial gifts. In reality, any monetary gift intended to help with a home purchase may require a Gift Letter, regardless of the amount.

This is not true. Both first-time buyers and repeat buyers may use Gift Letters if they receive financial assistance from family or friends.

Some think that a simple conversation suffices. However, lenders typically require a written Gift Letter to document the transaction properly.

While family members are common gift givers, friends and other individuals can also provide financial assistance, as long as it is documented correctly.

This is a misconception. Notarization is not typically required, but the letter must be signed by the donor.

While it’s best to provide the Gift Letter early in the process, it can sometimes be submitted at closing. Check with your lender for their specific requirements.

A Gift Letter indicates that the money is a gift, not a loan. It’s essential to clarify that the donor does not expect repayment.

Understanding these misconceptions can help ensure a smoother home-buying process. Always consult with your lender for specific requirements related to Gift Letters.