Get IRS 1120 Form in PDF

Get IRS 1120 Form in PDF

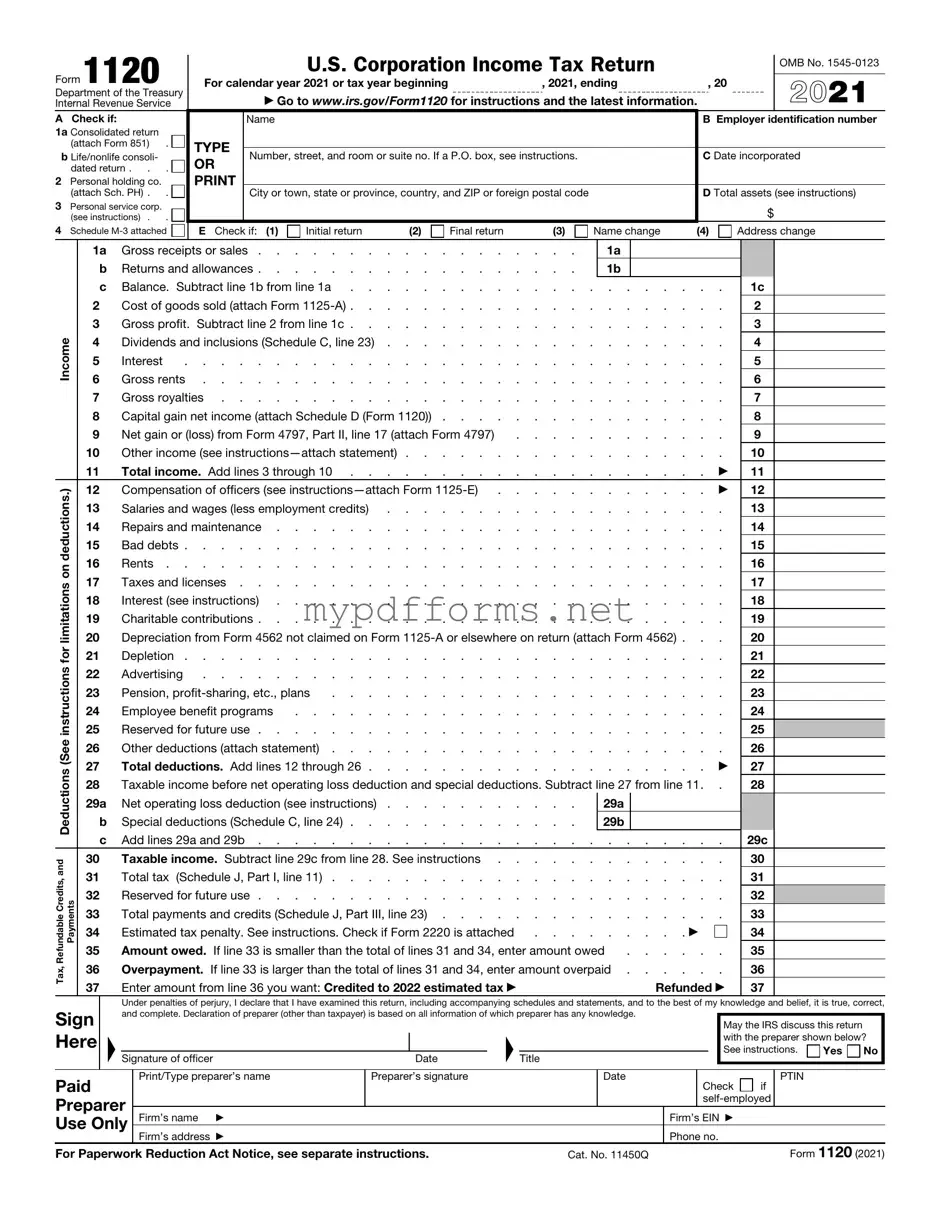

The IRS Form 1120 serves as a critical tool for corporations in the United States to report their income, deductions, and tax liability. This form is essential for C corporations, which are separate legal entities from their owners, allowing them to pay taxes at the corporate level. Corporations must detail their revenue, including sales and other income, while also itemizing various expenses such as salaries, rent, and cost of goods sold. Additionally, the form requires corporations to disclose any tax credits they may be eligible for, which can significantly reduce their overall tax burden. Filing Form 1120 accurately is crucial, as it not only impacts the corporation's tax obligations but also informs the IRS of the company’s financial health. Timely submission is vital to avoid penalties, and understanding the nuances of this form can help corporations navigate the complexities of federal tax regulations.

When filling out the IRS Form 1120, which is used by corporations to report their income, it’s important to follow certain guidelines to ensure accuracy and compliance. Here’s a list of things you should and shouldn’t do:

Sample Proxy Form for Homeowners' Association - Be aware of the meeting date to ensure your proxy is submitted on time.

When dealing with property transfers, it's essential to understand the implications of using a Michigan Quitclaim Deed, which allows for the transfer of ownership without title guarantees. This form can often be a straightforward solution in family situations or sales between friends. To get started and fill out the necessary form, visit https://quitclaimdocs.com/fillable-michigan-quitclaim-deed/.

Health Insurance Marketplace Statement - Taxpayers should familiarize themselves with the 1095-A details to maximize their tax benefits.

The IRS Form 1120 is essential for corporations to report their income, gains, losses, deductions, and credits. Here are some key takeaways to keep in mind when filling out and using this form:

By following these guidelines, you can ensure that your Form 1120 is completed accurately and submitted on time, helping to maintain compliance with IRS regulations.

Filling out the IRS Form 1120 is a crucial step for corporations to report their income, gains, losses, deductions, and credits. Ensuring accuracy is vital, as this form plays a significant role in determining tax obligations. Follow these steps carefully to complete the form correctly.

After submitting the form, keep a copy for your records. Monitor any correspondence from the IRS regarding your submission, as it may require further action or clarification.

What is the IRS Form 1120?

The IRS Form 1120 is the U.S. Corporation Income Tax Return. Corporations use this form to report their income, gains, losses, deductions, and credits. It is essential for calculating the corporation's tax liability for the year.

Who is required to file Form 1120?

Any corporation that is created or organized in the United States or under U.S. law must file Form 1120. This includes C corporations, which are taxed separately from their owners. Certain exceptions may apply, such as S corporations, which file a different form.

When is Form 1120 due?

Form 1120 is generally due on the 15th day of the fourth month after the end of the corporation's tax year. For corporations that operate on a calendar year, this means the due date is April 15. If the due date falls on a weekend or holiday, the deadline is extended to the next business day.

What information is required on Form 1120?

The form requires detailed information about the corporation's income, deductions, and credits. Key sections include:

Accurate reporting is crucial, as it affects the corporation's tax liability.

Can a corporation file Form 1120 electronically?

Yes, corporations can file Form 1120 electronically. The IRS encourages electronic filing as it can expedite processing times and reduce errors. Corporations must use an approved e-file provider to submit their returns electronically.

What happens if a corporation fails to file Form 1120?

If a corporation fails to file Form 1120 by the due date, it may face penalties. The IRS imposes a penalty for late filing, which can accumulate over time. Additionally, failure to file can result in the corporation losing its good standing with the state and incurring interest on unpaid taxes.

Are there any special considerations for foreign corporations?

Foreign corporations that engage in business within the United States must also file Form 1120 if they meet specific criteria. They must report their effectively connected income and may be subject to different tax rates. It's important for foreign corporations to understand their filing obligations to comply with U.S. tax laws.

Where can I find additional resources for completing Form 1120?

The IRS website provides comprehensive resources, including instructions for Form 1120, worksheets, and examples. Additionally, consulting with a tax professional can offer tailored guidance, especially for complex situations.

The IRS Form 1120 is primarily used by corporations to report their income, gains, losses, deductions, and credits. It serves as the standard corporate tax return. A similar document is the IRS Form 1120-S, which is specifically designed for S corporations. Unlike the standard Form 1120, which is for regular corporations, Form 1120-S allows S corporations to pass income directly to shareholders, avoiding double taxation. This form also requires reporting of various income sources, deductions, and credits, but it emphasizes the flow-through nature of income in S corporations.

For those involved in transactions requiring liability protection, understanding the importance of a strict Hold Harmless Agreement clause can prove invaluable. This legal document not only safeguards interests but also delineates responsibilities in scenarios like property rentals or special events. By utilizing this form, parties can ensure that they are taking appropriate legal steps to mitigate risks associated with their engagements.

Another related document is the IRS Form 1065, which is used by partnerships to report income, deductions, gains, and losses. Like Form 1120, Form 1065 serves to inform the IRS about the financial activities of the business. However, it differs in that partnerships do not pay taxes at the entity level; instead, income is passed through to partners, who report it on their personal tax returns. This form also includes a Schedule K-1 for each partner, detailing their share of the partnership's income and deductions.

The IRS Form 990 is a key document for tax-exempt organizations, such as charities. While Form 1120 focuses on corporations, Form 990 provides transparency for nonprofits by requiring them to disclose their financial activities, governance, and compliance with tax regulations. Both forms aim to ensure proper reporting and compliance, but Form 990 emphasizes public accountability and the use of funds for charitable purposes.

Form 941, the Employer's Quarterly Federal Tax Return, is another important document for businesses, though it focuses on employment taxes. Businesses use this form to report income taxes, Social Security, and Medicare taxes withheld from employee paychecks. While Form 1120 reports overall corporate income and expenses, Form 941 is specifically for payroll taxes, highlighting the different aspects of business taxation.

The IRS Form 1065-B is similar to Form 1065 but is used by electing large partnerships. This form allows large partnerships with specific characteristics to report their income and deductions in a manner that is slightly different from regular partnerships. While both forms share the goal of reporting partnership income, Form 1065-B includes provisions tailored to larger entities, reflecting their unique structure and tax requirements.

Form 1120-POL is used by political organizations to report their income, gains, losses, deductions, and credits. While it serves a similar purpose to Form 1120, it is specifically tailored for organizations that primarily engage in political activities. This form ensures that political organizations comply with tax regulations while also providing a clear picture of their financial activities to the IRS.

The IRS Form 5500 is relevant for employee benefit plans, such as pension and health plans. While not a corporate tax return, it shares similarities in that it requires detailed reporting of financial activities related to employee benefits. Like Form 1120, it aims to ensure compliance with federal regulations, but it focuses on the management and funding of employee benefit plans instead of corporate income.

Form 1120-F is for foreign corporations that have income effectively connected with a trade or business in the United States. This form is similar to Form 1120 in that it reports income and deductions, but it addresses the unique tax situation of foreign entities. It ensures that foreign corporations comply with U.S. tax laws while providing a framework for reporting their U.S.-sourced income.

Finally, IRS Form 990-T is used by tax-exempt organizations to report unrelated business income. This form is similar to Form 1120 in that it requires reporting of income and expenses, but it specifically addresses income that is not related to the organization’s primary exempt purpose. Both forms ensure proper reporting and compliance, but Form 990-T focuses on the income generated from activities that may be subject to taxation despite the organization’s tax-exempt status.

The IRS Form 1120 is essential for corporations to report their income, gains, losses, deductions, and credits. However, several other forms and documents are often used in conjunction with Form 1120 to provide a comprehensive overview of a corporation's financial activities. Below is a list of some of these commonly associated forms and documents, along with a brief description of each.

Understanding these forms and documents is crucial for ensuring compliance with IRS regulations. Each plays a unique role in the overall tax reporting process, helping corporations accurately reflect their financial activities and obligations. By keeping these forms organized and readily available, corporations can streamline their tax preparation efforts and minimize potential issues with the IRS.

The IRS Form 1120 is a crucial document for corporations in the United States, but several misconceptions often arise regarding its purpose and requirements. Understanding these misconceptions can help ensure compliance and accurate reporting. Below is a list of common misunderstandings about Form 1120.

Understanding these misconceptions can help corporations navigate the complexities of tax filing and ensure they meet their obligations accurately and on time.