Get IRS 433-F Form in PDF

Get IRS 433-F Form in PDF

The IRS 433-F form plays a crucial role in the financial dealings between taxpayers and the Internal Revenue Service (IRS). This form is primarily used to provide a comprehensive overview of a taxpayer's financial situation, which can include income, expenses, assets, and liabilities. When individuals or businesses find themselves unable to pay their tax debts in full, submitting the 433-F can help facilitate a discussion about payment options, such as installment agreements or offers in compromise. By detailing your financial circumstances, the form helps the IRS assess your ability to pay and determine a reasonable resolution. Completing the IRS 433-F accurately is essential, as it directly impacts your negotiations with the IRS. Understanding its components and the information required can empower taxpayers to navigate their financial obligations more effectively.

When filling out the IRS 433-F form, it’s crucial to ensure accuracy and completeness. Here are six essential dos and don'ts to guide you through the process.

Following these guidelines will help ensure your form is processed smoothly and efficiently. Take the time to double-check your information. It can make a significant difference in your dealings with the IRS.

Roofing Quote Template - For any roofing query, start with a detailed estimate request.

Completing the Florida Marriage Application form is crucial for engaged couples, as it not only provides the necessary information for obtaining a marriage license but is also the first step in the legal marriage process in Florida. To learn more about this important document, you can visit https://floridapdfform.com, where you will find detailed guidance and resources for ensuring your application is filled out correctly.

Texas Temporary Tag - Temporary tags can assist in meeting legal driving requirements.

The IRS 433-F form is a crucial document for individuals dealing with tax issues. Understanding how to fill it out correctly can make a significant difference in managing your tax situation. Here are some key takeaways to keep in mind:

By keeping these points in mind, you can navigate the IRS 433-F form with greater confidence and clarity. Properly completing this form is a vital step toward resolving your tax obligations.

Completing the IRS 433-F form is an important step in managing your tax situation. This form helps the IRS understand your financial situation. Follow these steps to fill it out accurately.

After completing the form, review it for accuracy. Submit it to the appropriate IRS address based on your location. Keep a copy for your records.

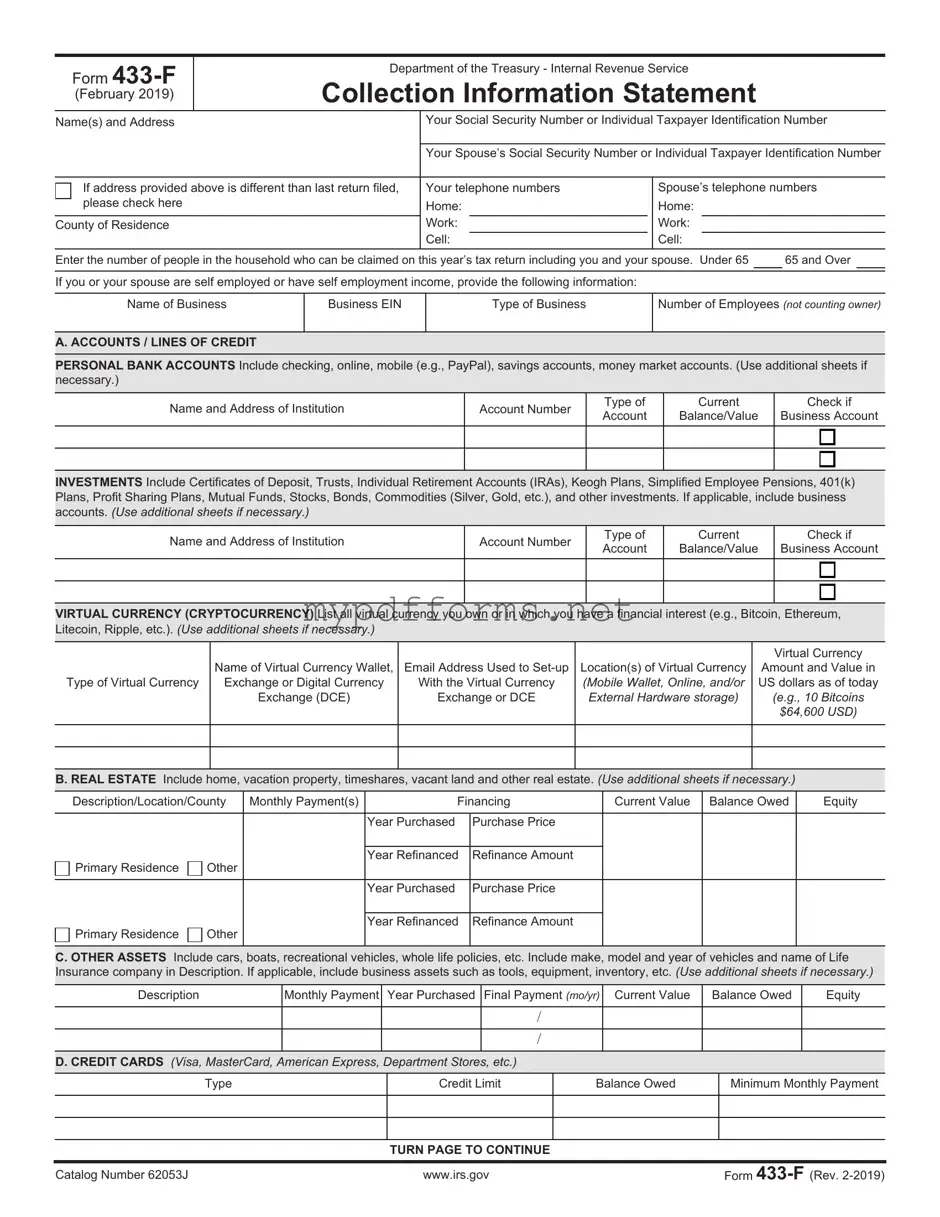

The IRS 433-F form, also known as the Collection Information Statement, is a document used by the Internal Revenue Service to collect financial information from taxpayers. This form helps the IRS assess a taxpayer's ability to pay outstanding tax debts. It provides a snapshot of your financial situation, including income, expenses, assets, and liabilities.

You may need to complete the IRS 433-F form if you are applying for an installment agreement, an offer in compromise, or if the IRS has requested it as part of their collection process. If you owe back taxes and are unable to pay in full, this form can help the IRS understand your financial situation and potentially work with you on a payment plan.

Filling out the IRS 433-F form involves several steps. First, gather all relevant financial documents, such as pay stubs, bank statements, and bills. Next, provide accurate information about your income, expenses, assets, and liabilities in the designated sections of the form. It's essential to be honest and thorough, as any discrepancies can lead to complications in your case.

Once you submit the IRS 433-F form, the IRS will review your information. They may contact you for additional details or clarification. Depending on your financial situation, they will determine whether to approve your request for an installment agreement or an offer in compromise. Keep in mind that this process can take time, so patience is key.

The IRS Form 433-A is similar to Form 433-F in that both are used to collect financial information from individuals. Form 433-A is specifically designed for individuals who owe more than $50,000 in taxes and is more detailed. It requires information about assets, income, expenses, and debts. This comprehensive nature allows the IRS to evaluate an individual's ability to pay tax liabilities, just as Form 433-F does, but with a deeper dive into financial status.

For those navigating the complexities of tax documentation, understanding various forms is crucial, including the Employment Verification Letter which serves to confirm an individual's work status and financial reliability, often impacting their ability to manage tax obligations effectively.

Form 433-B is another related document, but it is tailored for businesses. Like Form 433-F, it gathers financial information to assess the business's ability to pay tax debts. It requires details about the business's income, expenses, and assets. Both forms aim to provide the IRS with a clear picture of financial situations, but 433-B focuses on business entities rather than individuals.

Form 656 is closely associated with the 433 series as it is used to submit an Offer in Compromise (OIC). While Form 433-F collects financial data, Form 656 uses that data to propose a settlement amount that is less than the total tax owed. The information provided on Form 433-F helps the IRS determine whether to accept the offer based on the taxpayer's financial situation.

Form 9465, the Installment Agreement Request, also shares similarities with Form 433-F. This form allows taxpayers to request a payment plan for their tax debt. To evaluate the request, the IRS may require financial information similar to that collected in Form 433-F. Both forms aim to facilitate payment of tax liabilities, albeit through different methods.

Form 1040 is the individual income tax return form that, while not directly similar, is crucial for understanding an individual’s financial situation. The IRS uses the information from Form 1040 to assess tax liability. When filing Form 433-F, taxpayers often reference their 1040 to provide accurate income and expense data, ensuring consistency in their financial disclosures.

Form 8821, the Tax Information Authorization, allows taxpayers to authorize someone to receive their tax information. While not a financial disclosure form like 433-F, it plays a role in the overall process of managing tax liabilities. Taxpayers often need assistance in understanding their financial obligations, and this form facilitates communication between the IRS and authorized representatives.

Form 2848, the Power of Attorney and Declaration of Representative, is another document that supports the management of tax matters. Similar to Form 8821, it allows a representative to act on behalf of the taxpayer. Understanding the taxpayer's financial situation, as outlined in Form 433-F, can help representatives negotiate with the IRS more effectively.

Lastly, Form 1099 is not a direct counterpart but is relevant in the context of income reporting. This form reports various types of income other than wages, salaries, and tips. When completing Form 433-F, taxpayers must account for all sources of income, including those reported on Form 1099. Accurate reporting of income is essential for the IRS to assess a taxpayer's financial ability to settle tax debts.

The IRS 433-F form is an essential document used by individuals seeking to negotiate their tax debt with the IRS. However, there are several other forms and documents that often accompany it to provide a complete picture of an individual’s financial situation. Below is a list of these important documents.

When submitting the IRS 433-F form, including these additional documents can significantly strengthen your case. They provide the IRS with a clearer understanding of your financial situation, which is key to reaching a favorable resolution.

The IRS 433-F form is a crucial document for individuals dealing with tax debt, yet several misconceptions surround it. Understanding these misconceptions can help taxpayers navigate their financial obligations more effectively.

This is not true. While the form is often associated with significant tax issues, it can also be used by individuals who are simply seeking to negotiate payment plans or settle their tax liabilities, regardless of the amount owed.

Filing the form does not ensure acceptance of any offer. The IRS reviews each submission on a case-by-case basis, considering various factors before making a decision.

While professional help can be beneficial, it is not mandatory. Many individuals successfully complete the form on their own by carefully following the instructions provided by the IRS.

This is incorrect. The IRS takes a comprehensive look at your financial circumstances, including income, expenses, and assets, to determine your ability to pay.

In reality, you can amend your submission if your financial situation changes or if you realize you made an error. Keeping the IRS informed is essential for accurate processing.