Get IRS 8300 Form in PDF

Get IRS 8300 Form in PDF

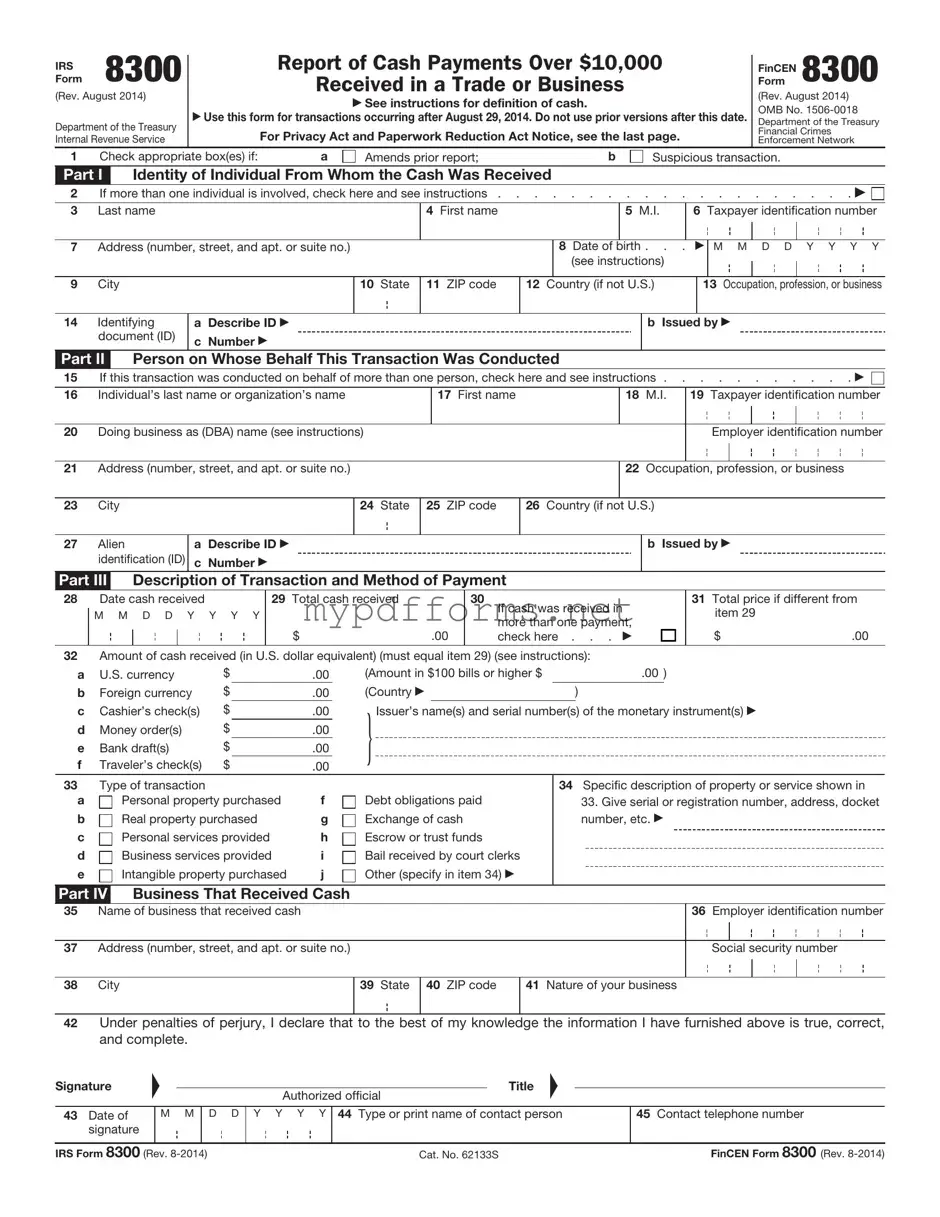

The IRS 8300 form plays a crucial role in maintaining transparency in financial transactions, particularly those involving cash payments exceeding $10,000. Businesses and individuals must file this form when they receive such payments, ensuring compliance with federal regulations aimed at combating money laundering and tax evasion. The form requires detailed information about the payer, including their name, address, and taxpayer identification number, as well as specifics about the transaction itself. Timely submission is essential; the form must be filed within 15 days of receiving the cash payment. Failure to comply can result in significant penalties. Understanding the requirements and implications of the IRS 8300 form is vital for anyone engaged in large cash transactions, as it not only safeguards against legal repercussions but also contributes to the integrity of the financial system.

When filling out the IRS 8300 form, it is important to follow specific guidelines to ensure accuracy and compliance. Below is a list of things to do and avoid.

Broward Animal Control - Pets are required to be vaccinated against rabies by law in many areas.

When engaging in a motorcycle sale in Arizona, it is crucial to utilize the Arizona Motorcycle Bill of Sale form to document the transaction. By providing a clear record of the sale, this form helps ensure a smooth transfer of ownership between the buyer and seller. For those looking to obtain a reliable version of this essential document, visit motorcyclebillofsale.com/free-arizona-motorcycle-bill-of-sale to access the necessary resources.

Pest Control Contract - Include special instructions that may be necessary for effective pest control implementation.

Filling out the IRS 8300 form is an important process for businesses that receive cash payments over a certain threshold. Here are some key takeaways to keep in mind:

Completing the IRS 8300 form requires attention to detail and accuracy. After gathering the necessary information, follow the steps outlined below to ensure the form is filled out correctly.

After completing these steps, ensure the form is submitted promptly to meet the IRS deadline. This helps maintain compliance and avoid potential penalties.

The IRS Form 8300 is a document that businesses must file when they receive cash payments exceeding $10,000 in a single transaction or in related transactions. This form is important for tracking large cash transactions to prevent money laundering and other illegal activities. By reporting these transactions, businesses help the government monitor financial activities and ensure compliance with tax laws.

Any business that accepts cash payments over $10,000 must file Form 8300. This requirement applies to various types of businesses, including retail stores, car dealerships, and service providers. It's essential for businesses to understand that the $10,000 threshold applies to the total cash received, not just individual transactions. If a customer pays in cash multiple times in a short period, and the total exceeds $10,000, the business must file the form.

Form 8300 requires several pieces of information. Businesses need to provide details about the transaction, including the amount of cash received, the date of the transaction, and the nature of the business. Additionally, information about the person or entity making the cash payment is necessary. This includes their name, address, and taxpayer identification number. Accurate and complete information is crucial, as errors can lead to penalties.

Failing to file Form 8300 when required can lead to significant consequences. The IRS imposes penalties for non-compliance, which can vary based on the severity of the violation. If a business neglects to report a transaction, it may face fines and increased scrutiny from tax authorities. In severe cases, repeated violations could lead to criminal charges. Therefore, it is essential for businesses to stay informed and comply with the reporting requirements to avoid these potential issues.

The IRS Form 1099 is a crucial document used to report various types of income other than wages, salaries, and tips. Like the IRS Form 8300, which reports cash transactions exceeding $10,000, the 1099 form serves to inform the IRS about income received by individuals or entities. Both forms aim to ensure transparency and compliance with tax regulations, helping the IRS track income that may otherwise go unreported. They both require accurate information about the payer and recipient, emphasizing the importance of record-keeping for tax purposes.

Form W-2 is another essential document that shares similarities with the IRS Form 8300. While the W-2 reports wages and salaries paid to employees, it also serves to document income for tax reporting. Both forms require detailed information about the payer and recipient, including identification numbers. They function as tools for the IRS to monitor income and ensure that taxes are paid appropriately, reinforcing the integrity of the tax system.

The IRS Form 8949 is used to report capital gains and losses from the sale of assets. Similar to the IRS Form 8300, it plays a role in maintaining transparency in financial transactions. While Form 8300 focuses on large cash transactions, Form 8949 addresses the sale of investments, requiring detailed reporting of each transaction. Both forms highlight the importance of accurate reporting and compliance with tax laws, ensuring that all financial activities are properly documented.

The Bank Secrecy Act (BSA) Currency Transaction Report (CTR) is a document that banks and financial institutions must file when a customer conducts a cash transaction exceeding $10,000. This report is similar to the IRS Form 8300 in that both documents aim to monitor large cash transactions to prevent money laundering and other financial crimes. Both forms require detailed information about the transaction and the parties involved, reinforcing the need for vigilance in financial reporting.

The Foreign Bank and Financial Accounts Report (FBAR) is another document that focuses on financial transparency. Individuals with foreign bank accounts exceeding $10,000 must file the FBAR, similar to the IRS Form 8300's requirement for reporting cash transactions. Both documents serve to inform the government about substantial financial activity, helping to combat tax evasion and ensure compliance with financial regulations.

Form 5471 is used by U.S. citizens and residents who are officers, directors, or shareholders in certain foreign corporations. This form requires extensive reporting of financial activities, paralleling the IRS Form 8300's focus on significant transactions. Both forms emphasize the need for transparency in financial dealings, ensuring that the IRS has a comprehensive understanding of taxpayers' financial situations.

Form 1065 is utilized by partnerships to report income, deductions, and other financial information. Similar to the IRS Form 8300, it requires detailed reporting to ensure accurate tax assessment. Both forms are essential for compliance with tax laws, as they help the IRS track financial activities and ensure that all income is reported appropriately.

The IRS Form 990 is filed by tax-exempt organizations to provide the IRS with information about their financial activities. Like the IRS Form 8300, it serves as a tool for transparency and accountability. Both forms require detailed reporting and aim to ensure compliance with tax regulations, helping to maintain the integrity of the tax system.

Form 1066 is used by real estate investment trusts (REITs) to report income, deductions, and other financial information. This form shares similarities with the IRS Form 8300 in that both require comprehensive reporting of financial activities. They both play a vital role in ensuring compliance with tax laws and providing the IRS with necessary information to assess tax obligations accurately.

Understanding the various forms used for reporting income and financial transactions is crucial for compliance. For instance, if you're dealing with a real estate recovery situation in Illinois, you may need to familiarize yourself with the Illinois 20A form. This document is essential for notifying a defendant about a pending forcible entry action and it plays a significant role in the eviction process. To ensure you have all the necessary details, you can access the Illinois Forms that can guide you through the proper procedures.

Finally, Form 941 is the Employer's Quarterly Federal Tax Return, which reports income taxes, Social Security tax, and Medicare tax withheld from employee wages. Like the IRS Form 8300, it emphasizes the importance of accurate reporting and compliance with tax regulations. Both forms require detailed information about financial transactions, ensuring that the IRS can effectively monitor tax liabilities and enforce tax laws.

The IRS 8300 form is essential for reporting cash payments over $10,000 received in a trade or business. However, there are several other forms and documents that often accompany it to ensure compliance with tax regulations and to provide additional information. Below is a list of these related documents.

By understanding these additional forms and documents, you can ensure that all necessary information is accurately reported and compliant with IRS regulations. This not only helps in maintaining proper records but also minimizes the risk of issues with tax authorities.

The IRS Form 8300 is an important document for businesses that receive cash payments over $10,000. However, several misconceptions surround this form. Here are seven common misunderstandings:

This is not true. While the form is specifically for cash payments, it also applies to transactions involving cash equivalents, such as money orders and cashier's checks.

In reality, any business that receives cash payments exceeding $10,000 must file this form, regardless of its size. This includes sole proprietors and small businesses.

This is a misconception. Filing Form 8300 is mandatory when cash payments exceed the threshold. Failing to do so can lead to significant penalties.

While the IRS does collect this information, it can also be shared with other government agencies, including law enforcement, to help combat money laundering and other illegal activities.

The form must be filed within 15 days of the transaction. This timeframe allows businesses to organize their records and ensure accurate reporting.

This is incorrect. If multiple related transactions occur within a 12-month period that together exceed $10,000, they must also be reported on the form.

In truth, failing to file can result in hefty fines and penalties. The IRS takes compliance seriously, and businesses must adhere to the regulations.

Understanding these misconceptions can help businesses stay compliant and avoid potential issues with the IRS. It's essential to be informed and proactive in managing cash transactions.