Get IRS 940 Form in PDF

Get IRS 940 Form in PDF

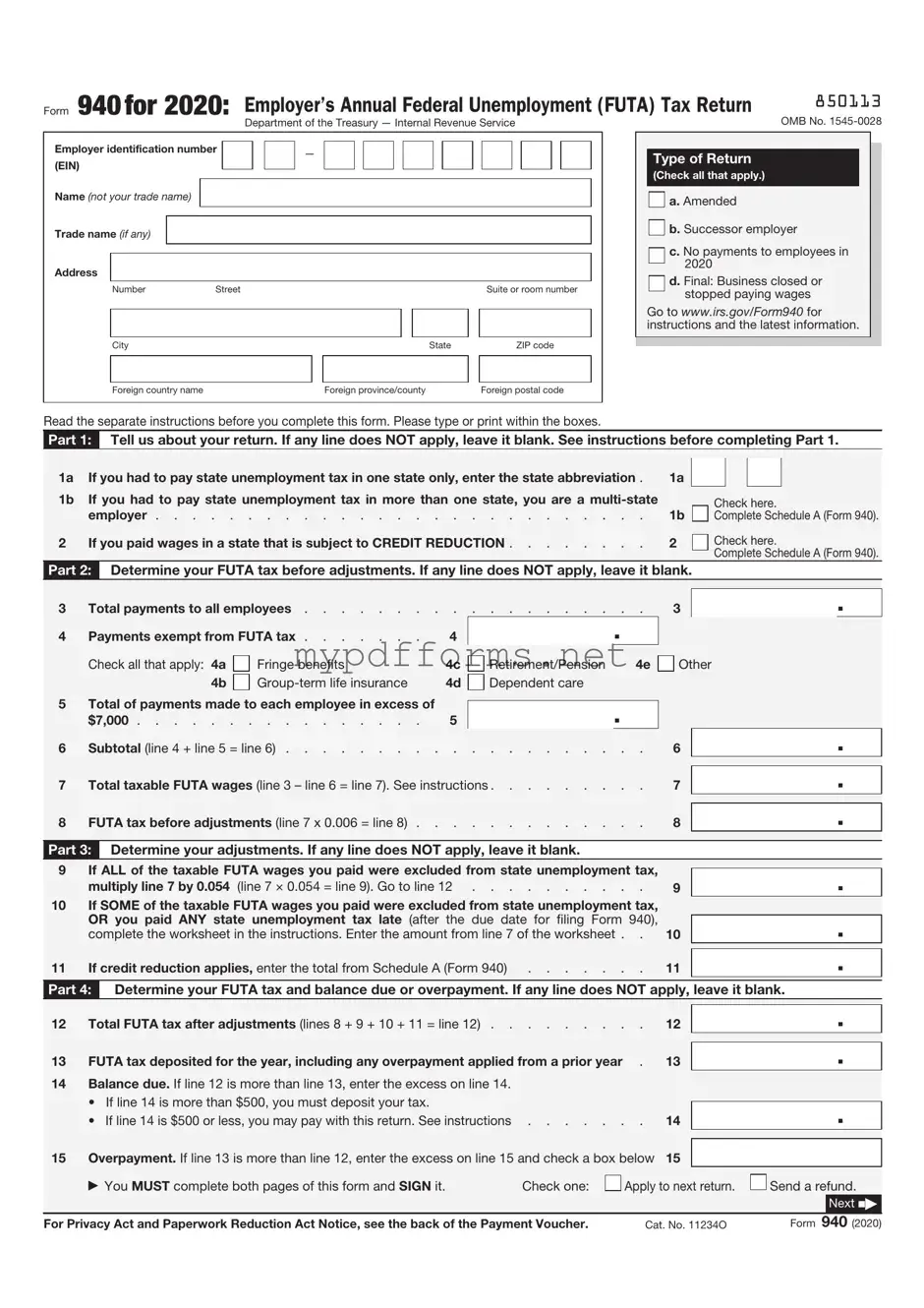

The IRS 940 form plays a crucial role in the landscape of employment taxes, serving as a vital tool for employers across the United States. This annual form is primarily used to report and pay federal unemployment tax (FUTA), a tax that funds unemployment benefits for workers who have lost their jobs. Employers must file this form if they paid $1,500 or more in wages in any calendar quarter or if they had at least one employee for any part of a day in 20 or more weeks during the year. Understanding the nuances of the IRS 940 form is essential for employers, as it not only ensures compliance with federal regulations but also helps in accurately calculating the amount owed. The form requires detailed information, including total taxable wages and any credits that may apply, such as those for state unemployment taxes paid. By grasping the key components and filing requirements of the IRS 940, employers can navigate the complexities of unemployment tax obligations with greater confidence and ease.

When filling out the IRS 940 form, it's important to follow certain guidelines to ensure accuracy and compliance. Here are four things to do and not do:

How to Design a Crest - A compass rose might be included to represent exploration and a journey through life.

In today’s competitive landscape, the importance of safeguarding your proprietary information cannot be overstated, and an Illinois Non-disclosure Agreement form serves as a key tool in achieving this goal. By ensuring that sensitive data is shared only under strict confidentiality, you can protect your business interests effectively. For those looking to secure their information, just click the button below to start filling out your form, or you can explore additional resources, including Illinois Forms, to assist you in the process.

5707e Form - In the event there are no children, a specific declaration must be signed in Section B.

The IRS 940 form is essential for employers who pay unemployment taxes. Here are some key takeaways to keep in mind when filling it out and using it:

Completing the IRS Form 940 is an important task for employers who need to report their annual Federal Unemployment Tax Act (FUTA) liability. Following these steps will help ensure the form is filled out correctly and submitted on time.

The IRS 940 form is an annual report that employers use to report their Federal Unemployment Tax Act (FUTA) tax. This tax funds unemployment benefits for workers who have lost their jobs. Employers must file this form if they paid wages of $1,500 or more in any calendar quarter or if they had at least one employee for any part of a day in 20 or more weeks during the year.

Any employer who meets the criteria mentioned above must file Form 940. This includes businesses of all sizes, as well as non-profit organizations. If you are unsure whether you need to file, it is best to consult with a tax professional.

The deadline for filing Form 940 is January 31 of the year following the tax year being reported. If you deposited all your FUTA tax on time, you may have until February 10 to file.

Form 940 requires various pieces of information, including:

The FUTA tax rate is currently 6.0% on the first $7,000 of each employee's wages. However, if you qualify for a credit, you may be able to reduce your effective tax rate to 0.6%. To calculate, multiply your total taxable wages by the applicable rate.

Failing to file Form 940 can lead to penalties and interest on any unpaid taxes. The IRS may impose fines for late filings, and the longer you wait, the more you may owe. It is essential to file on time to avoid these issues.

Yes, you can file Form 940 electronically using the IRS e-file system or through approved tax software. E-filing is often faster and can help ensure that your form is submitted correctly.

You can download Form 940 directly from the IRS website. It is also available through many tax software programs. Ensure you are using the correct version for the tax year you are reporting.

The IRS Form 941 is similar to Form 940 in that both are used by employers to report payroll taxes. While Form 940 is an annual report for federal unemployment taxes, Form 941 is filed quarterly and covers income taxes withheld from employee wages, Social Security, and Medicare taxes. Employers must file Form 941 to ensure compliance with tax withholding requirements throughout the year, whereas Form 940 focuses specifically on unemployment tax obligations.

When considering important legal documents, the New Jersey Do Not Resuscitate Order form is one that should not be overlooked, as it allows individuals to clearly state their wishes regarding life-saving measures during emergencies. Understanding this form is crucial for ensuring that medical preferences are honored, particularly in situations where prompt decisions are required. To facilitate access to various forms, individuals can consult resources such as NJ PDF Forms, which provide essential information and tools for completing necessary documentation.

Another related document is Form 944. This form is designed for small employers who have a lower payroll tax liability. Like Form 941, Form 944 reports federal income tax withheld and Social Security and Medicare taxes, but it is filed annually instead of quarterly. This allows eligible employers to simplify their reporting process, reducing the frequency of submissions while still meeting federal tax obligations.

Form 945 is also comparable to Form 940, as it is used to report federal income tax withheld from non-payroll payments, such as pensions and annuities. Employers and payers must file Form 945 annually, similar to how they file Form 940 for unemployment taxes. Both forms share the goal of ensuring accurate reporting of tax liabilities to the IRS, albeit for different types of payments.

Form 990 is another document that bears similarities to Form 940 in terms of reporting requirements, but it is specifically for tax-exempt organizations. While Form 940 deals with unemployment taxes for employers, Form 990 provides the IRS with information about the organization’s financial activities, governance, and compliance with tax regulations. Both forms serve to keep the IRS informed about the financial responsibilities of different entities.

Form W-2 is closely related as well, as it is used to report wages and taxes withheld for employees. Employers must issue Form W-2 to each employee at the end of the year, detailing their earnings and the taxes withheld. While Form 940 focuses on unemployment taxes, W-2 forms provide a comprehensive view of all payroll-related taxes and earnings, ensuring employees have the necessary information for their personal tax filings.

Form W-3 serves as a summary of all W-2 forms issued by an employer. It is submitted to the Social Security Administration and provides a total of all wages and taxes reported on the W-2 forms. Similar to Form 940, which summarizes unemployment tax obligations, Form W-3 consolidates payroll data, ensuring accurate reporting to the appropriate federal agency.

Finally, Schedule H is relevant for household employers who must report household employment taxes. This form is filed with the individual’s income tax return, detailing wages paid to household employees and the corresponding taxes owed. While Form 940 is specific to unemployment taxes for general employers, Schedule H addresses the unique tax responsibilities of those who hire domestic workers, ensuring compliance with federal tax laws.

The IRS 940 form is essential for employers as it reports annual Federal Unemployment Tax Act (FUTA) taxes. However, it is often accompanied by other forms and documents that help ensure compliance with federal and state tax regulations. Below is a list of forms that frequently accompany the IRS 940 form, each serving a unique purpose in the tax reporting process.

Understanding these forms and their purposes can help employers maintain compliance with tax laws and avoid potential penalties. Each document plays a vital role in the overall tax reporting process, ensuring that both federal and state obligations are met accurately and on time.

Understanding the IRS 940 form is crucial for employers. However, several misconceptions often lead to confusion. Here are eight common misunderstandings:

Clarifying these misconceptions can help ensure compliance and avoid potential penalties. Always consider consulting a tax professional for personalized advice.