Get IRS 941 Form in PDF

Get IRS 941 Form in PDF

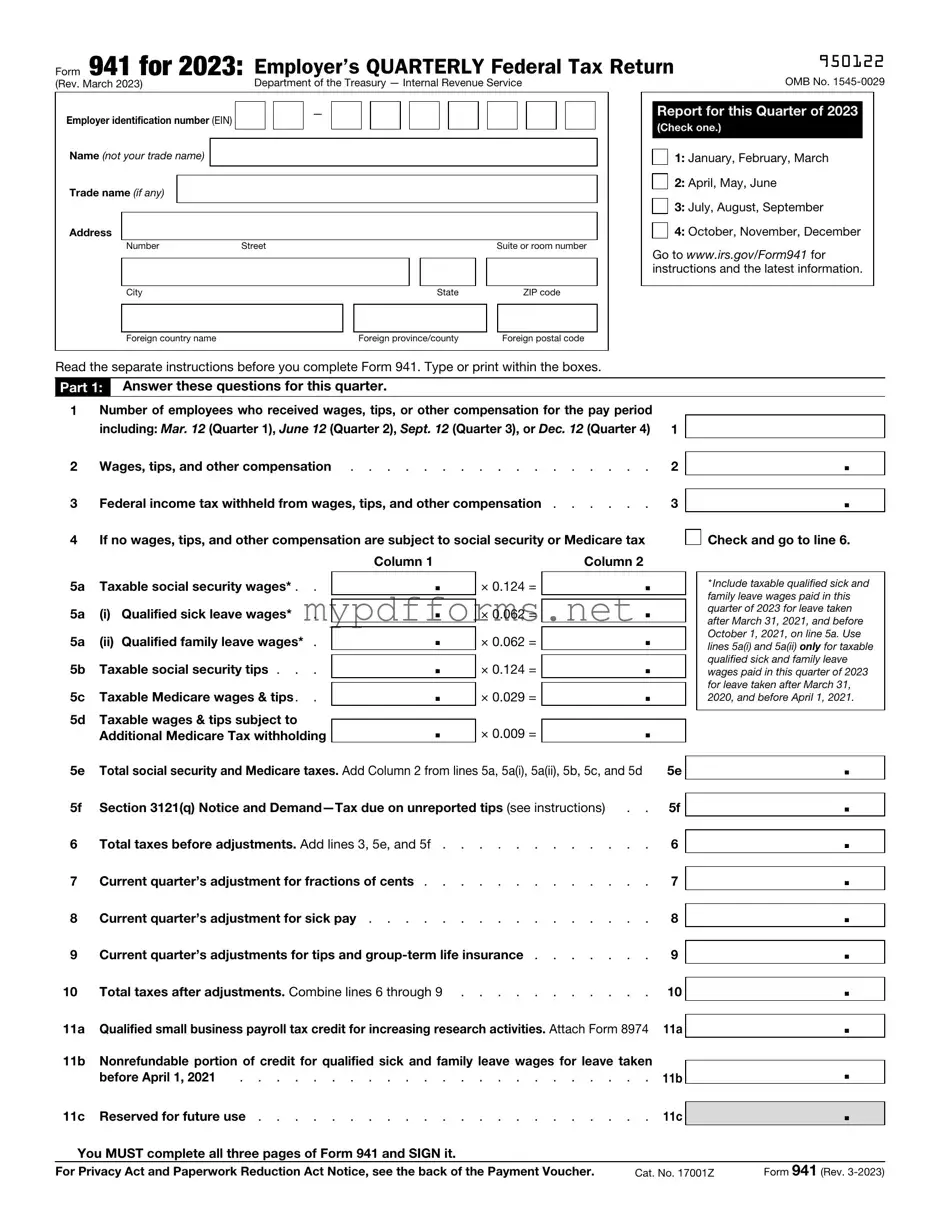

The IRS Form 941, officially known as the Employer's Quarterly Federal Tax Return, plays a crucial role in the landscape of payroll tax reporting for employers in the United States. This form is primarily used to report the wages paid to employees, the federal income tax withheld from those wages, and the employer and employee portions of Social Security and Medicare taxes. Employers must file this form quarterly, which means it is essential for maintaining compliance with federal tax obligations. Each quarter, businesses must accurately calculate and report their tax liabilities, ensuring that they contribute appropriately to the nation's social safety net. Additionally, Form 941 serves as a tool for the IRS to monitor compliance and assess potential penalties for underreporting or late payments. Understanding the nuances of this form is vital for any employer, as it not only affects their financial standing but also their relationship with the IRS and their employees. The form's instructions can be intricate, requiring careful attention to detail to avoid common pitfalls that could lead to audits or fines.

When filling out the IRS 941 form, it's important to follow certain guidelines to ensure accuracy and compliance. Here are six things to keep in mind:

Kde Decklist - Double-check your total number of trap cards.

Security Guard Observation Report - Documentation through this form helps ensure that security measures remain effective.

To ensure the confidentiality of sensitive information, utilizing a Maryland Non-disclosure Agreement template is highly advisable. This form establishes clear terms for confidentiality, allowing you to protect your business interests. For more information, you can visit the site that offers a comprehensive guide on the Non-disclosure Agreement process: comprehensive Maryland Non-disclosure Agreement form overview.

Emotional Support Animal Letter From Therapist - Official letter confirming the therapeutic necessity of an emotional support animal.

The IRS Form 941 is used by employers to report income taxes, Social Security tax, and Medicare tax withheld from employee paychecks.

This form must be filed quarterly, meaning it is due four times a year: at the end of January, April, July, and October.

Employers must report the total wages paid to employees during the quarter on this form.

Accurate calculations of tax liabilities are essential; errors can lead to penalties or interest charges.

Form 941 can be filed electronically or by mail, but electronic filing is often faster and more efficient.

Employers should keep records of all payroll and tax information, as the IRS may require these documents for verification.

Form 941 includes sections for adjustments, allowing employers to correct any previous errors in reported amounts.

It is important to ensure that the form is signed and dated before submission, as an unsigned form may be considered invalid.

Filling out the IRS 941 form is an important step for employers to report payroll taxes. After completing the form, you will need to submit it to the IRS by the appropriate deadline. Make sure to keep a copy for your records.

IRS Form 941 is a quarterly tax form that employers use to report income taxes, Social Security tax, and Medicare tax withheld from employee wages. It is also used to report the employer's share of Social Security and Medicare taxes.

Any employer who pays wages to employees must file Form 941. This includes businesses, non-profits, and government entities. If you have no employees during a quarter, you may not need to file, but you should check the IRS guidelines.

Form 941 is due on the last day of the month following the end of each quarter. For example:

You can file Form 941 electronically or by mail. To file electronically, use the IRS e-file system or a third-party software provider. If you choose to file by mail, send the completed form to the address specified for your location in the IRS instructions.

If you discover an error after filing, you should correct it by filing Form 941-X, Adjusted Employer’s QUARTERLY Federal Tax Return or Claim for Refund. This form allows you to make adjustments to previously filed Forms 941.

Yes, you can amend a previously filed Form 941 using Form 941-X. This is necessary if you need to correct errors in wages, taxes withheld, or other amounts reported.

Failing to file Form 941 can lead to penalties and interest on unpaid taxes. The IRS may assess fines for late filings. It’s essential to file on time to avoid these consequences.

The IRS Form 940 is similar to Form 941 in that both are used by employers to report taxes related to employee wages. While Form 941 is filed quarterly and focuses on income, Social Security, and Medicare taxes, Form 940 is an annual report that specifically addresses the Federal Unemployment Tax Act (FUTA). Employers use Form 940 to report and pay unemployment taxes, which help fund unemployment benefits for workers who lose their jobs. Both forms require accurate payroll information to ensure compliance with federal tax obligations.

Form W-2 is another document that shares similarities with Form 941. While Form 941 is filed quarterly, Form W-2 is an annual statement that employers provide to their employees. It reports the total wages paid to an employee and the taxes withheld throughout the year. Both forms are essential for tax reporting and ensure that employees have the necessary information to file their individual income tax returns. The data reported on Form W-2 is also derived from the payroll information that employers report on Form 941.

Form W-3 is closely related to Form W-2, serving as a summary of all W-2 forms issued by an employer. Like Form 941, which summarizes quarterly tax liabilities, Form W-3 consolidates the information from all W-2s into one document for submission to the Social Security Administration. Both forms are crucial for ensuring that the correct amounts of taxes are reported and that employees receive proper credit for their earnings and contributions toward Social Security and Medicare.

Form 943 is designed for agricultural employers, similar to Form 941. Both forms require employers to report taxes withheld from employee wages. However, Form 943 specifically pertains to farmworkers and includes unique provisions related to agricultural employment. The reporting periods align with those of Form 941, making it easier for agricultural employers to manage their tax obligations while ensuring compliance with federal tax laws.

Form 944 is another document that parallels Form 941, but it is intended for small employers with an annual payroll tax liability of $1,000 or less. Instead of filing quarterly, eligible employers can file Form 944 annually. This reduces the frequency of reporting for those with minimal payroll tax obligations while still ensuring that the IRS receives the necessary information about employee wages and tax withholdings.

Form 1099-MISC is a form used to report payments made to independent contractors and other non-employees. While Form 941 focuses on employee wages and taxes withheld, Form 1099-MISC serves a different purpose by documenting payments that are not subject to payroll taxes. Both forms are essential for accurate tax reporting, ensuring that the IRS has a complete picture of an employer's financial obligations and the payments made to various types of workers.

If you are looking to execute a property transfer, understanding the role of a Michigan Quitclaim Deed is crucial. This document facilitates the ownership shift without providing assurances regarding the title, making it ideal for personal transactions like those among family members or friends. For those interested in accessing a fillable form to ease the process, visit https://quitclaimdocs.com/fillable-michigan-quitclaim-deed.

Form 1040 is the individual income tax return that employees use to report their annual income, including wages reported on Form W-2. While Form 941 is a reporting tool for employers, Form 1040 is used by employees to calculate their tax liabilities. The information from Form 941 ultimately influences the amounts reported on Form 1040, as employees use the data to determine their eligibility for credits and deductions based on their reported income.

Finally, Form 1095-C is relevant for employers who provide health insurance to their employees. This form reports information about health coverage offered and is part of the Affordable Care Act requirements. While Form 941 deals with payroll taxes, both forms are essential for compliance with federal regulations. Employers must accurately report both payroll taxes and health coverage to avoid penalties and ensure that employees receive the necessary documentation for their tax filings.

The IRS Form 941 is a crucial document for employers, as it reports payroll taxes withheld from employees and the employer's share of Social Security and Medicare taxes. However, several other forms and documents are commonly used alongside Form 941 to ensure compliance with federal tax regulations. Below is a list of these forms, each serving a specific purpose in the payroll tax process.

Understanding these forms and their interconnections can significantly ease the burden of payroll tax compliance. Each document plays a vital role in the overall tax reporting process, ensuring that employers meet their obligations while providing accurate information to employees and the government alike.

The IRS Form 941 is an important document for employers, but many misconceptions surround it. Here are seven common misunderstandings:

Understanding these misconceptions can help employers navigate their tax responsibilities more effectively.