Get IRS Schedule B 941 Form in PDF

Get IRS Schedule B 941 Form in PDF

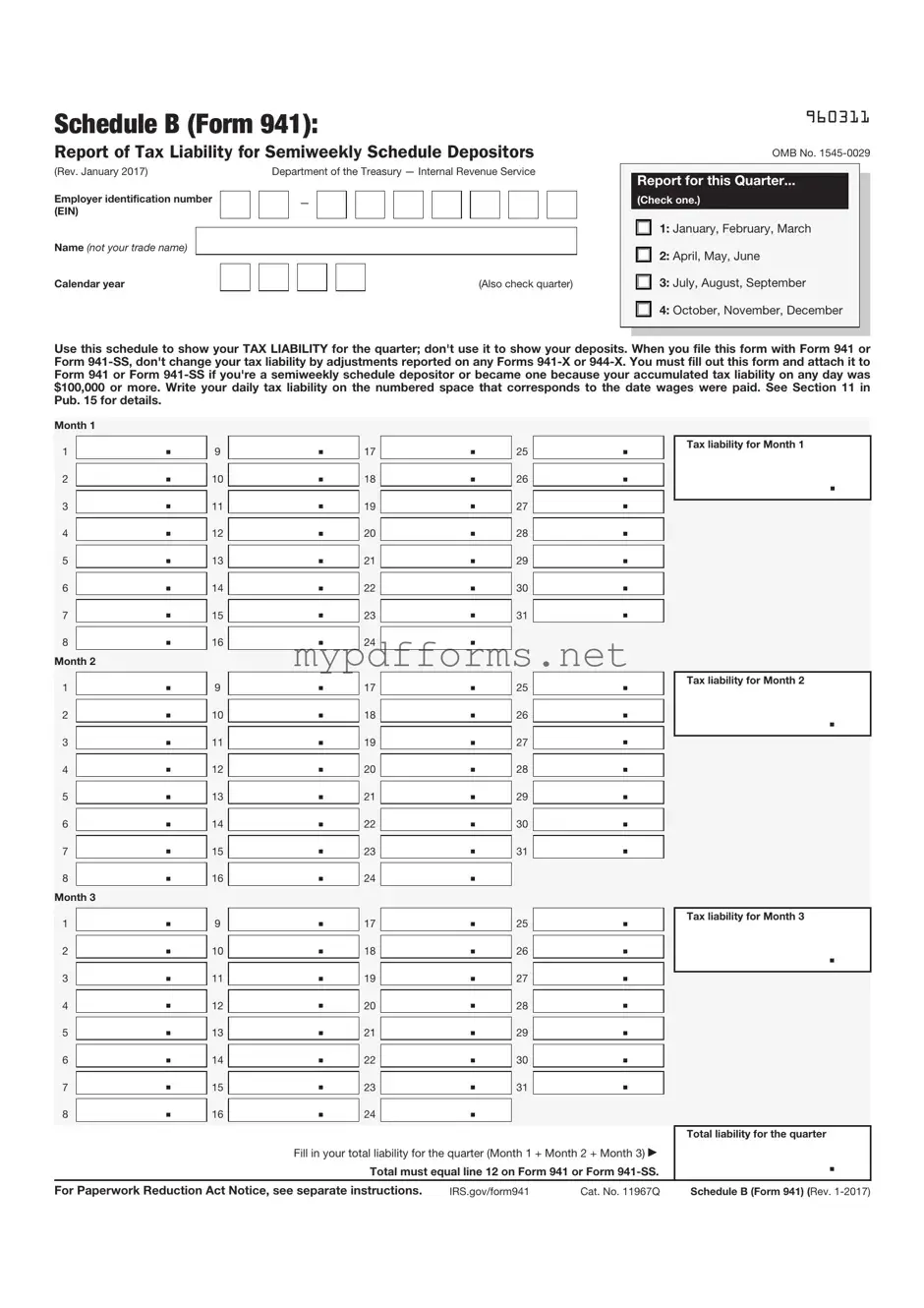

The IRS Schedule B (Form 941) serves as a critical component for employers who are required to report their payroll tax obligations. This form is specifically designed to provide the Internal Revenue Service with detailed information regarding the employment taxes withheld from employees' wages, as well as the employer's share of Social Security and Medicare taxes. Employers must complete this form on a quarterly basis, thereby ensuring compliance with federal tax regulations. Schedule B includes sections that require the reporting of various tax liabilities, including the total amount of wages paid and the total tax liability for the quarter. Additionally, it necessitates the disclosure of any adjustments to previously reported amounts, which helps maintain accurate records. By completing Schedule B, employers not only fulfill their legal obligations but also contribute to the overall integrity of the tax system, ensuring that the correct amounts are reported and paid in a timely manner.

When filling out the IRS Schedule B 941 form, it's important to follow certain guidelines to ensure accuracy and compliance. Here are some key do's and don'ts:

1750 Pdf - Properly filled forms contribute to transparency in military supply chain management.

When engaging in a motorcycle transaction, it is vital to utilize the appropriate paperwork, such as the Minnesota Motorcycle Bill of Sale, to facilitate the ownership transfer; for more details, you can visit motorcyclebillofsale.com/free-minnesota-motorcycle-bill-of-sale to access the necessary forms and ensure all legal requirements are met.

5707e Form - The outcome of the visa application can significantly depend on the details captured in this form.

Correction Deed California - The Scrivener's Affidavit may be required in various contexts, including property deeds and court filings.

Here are some important points to consider when filling out and using the IRS Schedule B (Form 941):

After gathering all necessary information, you're ready to fill out the IRS Schedule B (Form 941). This form is essential for reporting certain tax details, and accuracy is crucial. Follow these steps to complete it correctly.

Once you have completed these steps, make sure to keep a copy for your records. Filing on time is crucial to avoid penalties, so be aware of the due dates for your specific quarter.

What is IRS Schedule B (Form 941)?

IRS Schedule B (Form 941) is used by employers to report their tax liability for federal income tax withheld and Social Security and Medicare taxes. This schedule is an important part of Form 941, which is filed quarterly. It helps the IRS track the timing of tax deposits made by employers. If you have a tax liability of $100,000 or more during a deposit period, you must complete Schedule B.

Who needs to file Schedule B?

Any employer who has a tax liability of $100,000 or more during a deposit period must file Schedule B along with their Form 941. This includes businesses that have a high payroll or have made significant tax deposits. It’s essential to check your tax liability to determine if you need to include this schedule with your quarterly filings.

How do I complete Schedule B?

To complete Schedule B, you will need to provide information about your tax liability for each month of the quarter. This includes the amount of federal income tax withheld, as well as the Social Security and Medicare taxes. You will also indicate the dates when you made your tax deposits. It’s important to ensure that all figures are accurate and match your records to avoid any issues with the IRS.

What happens if I don’t file Schedule B when required?

If you fail to file Schedule B when required, you may face penalties from the IRS. These penalties can be significant, depending on the amount of tax owed and how late the filing is. Additionally, not filing can lead to delays in processing your Form 941, which can affect your overall compliance with tax obligations. To avoid these issues, always check if you need to include Schedule B with your quarterly filings.

The IRS Schedule B (Form 941) is similar to the IRS Form 944. Both forms are used by employers to report payroll taxes. While Form 941 is typically filed quarterly, Form 944 is an annual return for smaller employers who owe less in payroll taxes. This means that the frequency of reporting differs, but both forms ultimately serve the same purpose of ensuring that employers report and pay their federal employment taxes accurately.

Another document that shares similarities with Schedule B is the IRS Form 940. This form is used to report federal unemployment tax (FUTA). Employers must file Form 940 annually, just as they might file Schedule B with Form 941 quarterly. Both forms require detailed information about employee wages and taxes withheld, ensuring compliance with federal tax obligations.

The IRS Schedule B (Form 941) is closely related to the IRS Form 943, which is used by agricultural employers. Like Schedule B, Form 943 accounts for social security and Medicare taxes, reporting wages paid to farmworkers. The structure and purpose of both forms are heavily focused on compliance with federal employment tax regulations. Employers in agriculture find Form 943 necessary to reflect their unique payroll situations, including seasonal workers and special rules applicable to farm labor. For those needing further resources on documentation, the newyorkpdfdocs.com provides helpful templates and forms to assist in various transactions.

Additionally, the IRS Form W-2 is comparable to Schedule B in that both documents relate to employee earnings and tax withholding. Employers must issue Form W-2 to employees at the end of the year, summarizing their total wages and the taxes withheld. While Schedule B focuses on reporting to the IRS throughout the year, Form W-2 serves as a year-end summary for employees and the IRS.

Lastly, IRS Form 1099 shares a connection with Schedule B, as it is used to report payments made to non-employees, such as independent contractors. Like Schedule B, Form 1099 ensures that the IRS receives accurate information about income and taxes withheld. Both forms are essential for maintaining transparency in financial reporting and fulfilling tax obligations.

The IRS Schedule B (Form 941) is an essential document for employers to report their tax liabilities. Along with this form, several other documents may be necessary to ensure compliance with federal tax regulations. Below is a list of commonly used forms and documents that often accompany Schedule B.

These documents play a crucial role in maintaining accurate records and ensuring compliance with tax obligations. It is important to stay organized and timely in filing these forms to avoid potential penalties and ensure smooth operations for your business.

Understanding the IRS Schedule B (Form 941) can be challenging. Below are six common misconceptions about this form, along with clarifications to help clear up any confusion.

Being aware of these misconceptions can help ensure compliance and accurate reporting when it comes to employment taxes.