Loan Agreement Template

Loan Agreement Template

When entering into a financial arrangement, a Loan Agreement form serves as a crucial document that outlines the terms and conditions of the loan. This form typically includes essential details such as the names of the lender and borrower, the loan amount, and the interest rate. It also specifies the repayment schedule, which outlines when and how payments will be made. Additional clauses may address late fees, prepayment options, and default conditions, providing clarity and protection for both parties involved. Understanding each component of the Loan Agreement form can help prevent misunderstandings and ensure that both the lender and borrower are on the same page throughout the loan period. By clearly defining responsibilities and expectations, this document plays a vital role in fostering a successful financial relationship.

When filling out a Loan Agreement form, it's essential to approach the task with care. Here are some helpful tips on what to do and what to avoid.

Things You Should Do:

Things You Shouldn't Do:

Hunting Lease Contract - The lease can detail that only certain species may be hunted, as determined by local laws.

Five Wishes Document Pdf - This document can ease the burden on family members by providing clear guidance on your healthcare choices.

To ensure that your LLC operates smoothly and is compliant with state regulations, it is essential to utilize the appropriate resources when drafting your Operating Agreement. For more information and to access necessary documentation, you can visit Illinois Forms, where you will find valuable templates and guidance tailored for your needs.

Shared Well Agreement - Responsibilities for damages during maintenance operations are laid out in the agreement.

When filling out and using a Loan Agreement form, it’s essential to understand several key points. Here are some important takeaways to consider:

By paying attention to these details, individuals can create a clear and effective Loan Agreement that serves the interests of both the lender and the borrower.

Completing the Loan Agreement form is an important step in securing your loan. Follow these steps carefully to ensure that all necessary information is provided accurately. This will help facilitate a smooth process as you move forward.

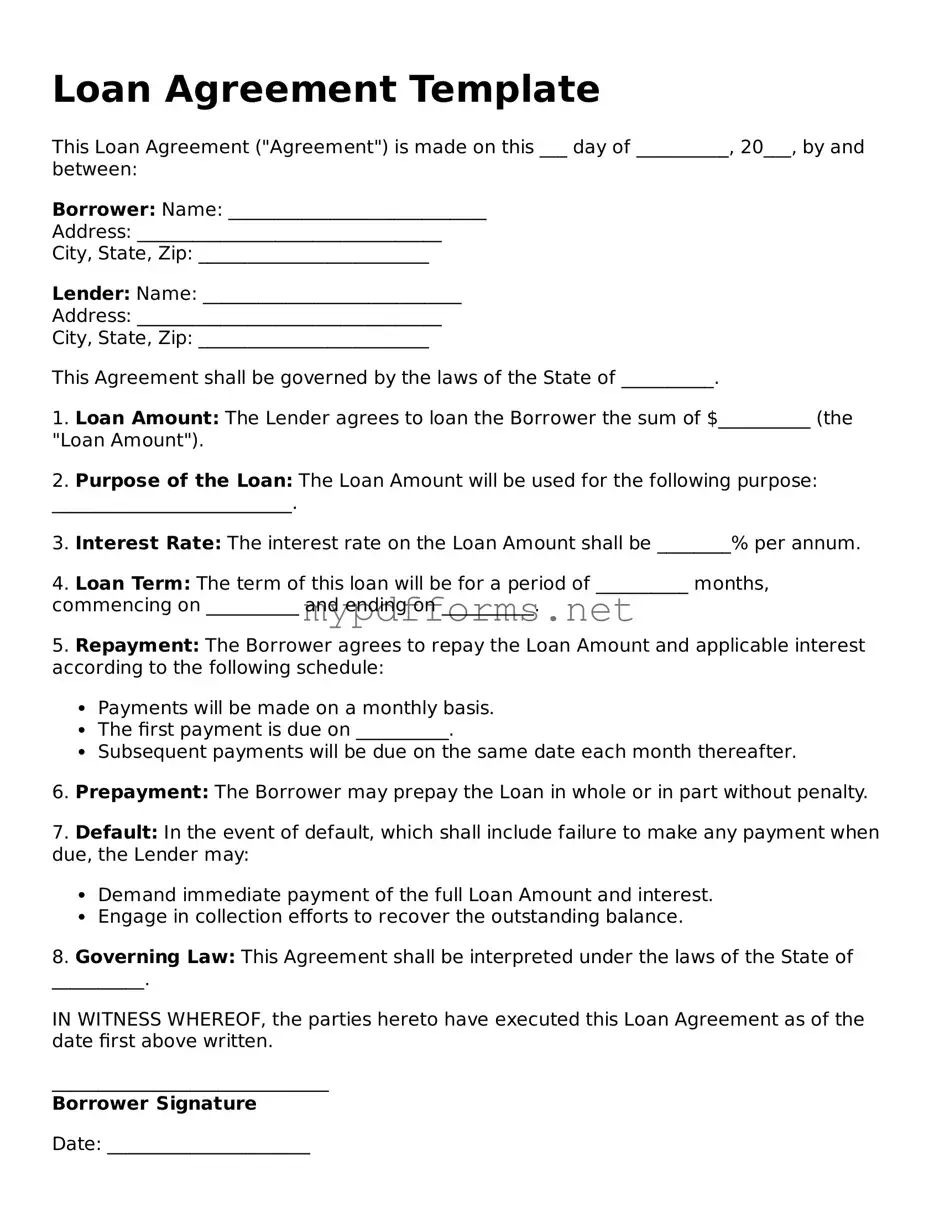

A Loan Agreement is a legally binding document between a lender and a borrower. It outlines the terms and conditions under which money is borrowed and specifies how and when the loan will be repaid. This document protects both parties by clearly defining the obligations of each side.

A comprehensive Loan Agreement typically includes the following elements:

Having a Loan Agreement is crucial for several reasons. First, it provides legal protection for both parties. If disputes arise, the agreement serves as a reference point for resolving conflicts. Second, it establishes clear expectations regarding repayment and other terms, which can help prevent misunderstandings. Finally, it can also help in maintaining a positive relationship between the lender and the borrower by ensuring transparency and accountability.

Yes, a Loan Agreement can be modified, but both parties must agree to the changes. Any modifications should be documented in writing and signed by both the lender and the borrower to ensure that they are enforceable. Verbal agreements or informal changes may not hold up in court, so it’s best to keep everything documented.

The Loan Agreement form shares similarities with a Promissory Note. Both documents outline the terms of a loan, including the amount borrowed, interest rates, and repayment schedules. A Promissory Note is typically a simpler document that focuses on the borrower's promise to repay the loan, while a Loan Agreement may provide more detailed terms and conditions. Each document serves as a binding contract, ensuring that both parties understand their obligations and rights regarding the loan transaction.

Another document akin to the Loan Agreement is the Mortgage Agreement. While a Loan Agreement can pertain to various types of loans, a Mortgage Agreement specifically deals with real estate loans. It outlines the borrower's commitment to repay the loan and includes details about the property being financed. Both documents protect the lender's interests, but the Mortgage Agreement adds a layer of security by using the property as collateral, which is not always the case in standard Loan Agreements.

A Credit Agreement is also similar to a Loan Agreement, as both outline the terms under which a borrower can access funds. However, a Credit Agreement typically involves a revolving line of credit, allowing the borrower to withdraw funds up to a specified limit as needed. In contrast, a Loan Agreement usually involves a lump sum that is repaid over time. Both documents require clear terms regarding interest rates, repayment schedules, and any fees associated with borrowing.

For those looking to manage their financial affairs effectively, the necessary details on the General Power of Attorney requirements can provide essential guidance on creating such a powerful legal document.

The Lease Agreement can be compared to a Loan Agreement in that both documents involve the exchange of value over time. A Lease Agreement outlines the terms under which a lessee can use property owned by a lessor in exchange for rental payments. Similar to a Loan Agreement, it specifies payment amounts, duration, and responsibilities of both parties. While one involves borrowing money and the other involves renting property, both serve to formalize an agreement and protect the rights of the involved parties.

Lastly, a Service Agreement has parallels with a Loan Agreement in that both documents define the terms of an arrangement between parties. A Service Agreement details the expectations, deliverables, and payment terms for services rendered. While a Loan Agreement focuses on the borrowing and repayment of funds, both documents require clear communication of obligations and can include terms for default or breach of contract. Each serves to ensure that both parties are aware of their responsibilities and the consequences of not fulfilling them.

When entering into a loan agreement, several other forms and documents often accompany the main contract to ensure clarity and protection for all parties involved. Below is a list of common documents that you may encounter in conjunction with a loan agreement.

Each of these documents plays a crucial role in the loan process, ensuring that both borrowers and lenders have a clear understanding of their rights and responsibilities. Being familiar with these forms can help facilitate a smoother transaction.

Understanding loan agreements can be tricky. Here are eight common misconceptions that people often have:

Each loan agreement is unique, tailored to the specific terms negotiated between the lender and borrower. Rates, fees, and repayment terms can vary widely.

Loan agreements can be used for both small and large amounts. Even a small personal loan can have a formal agreement.

While changes are difficult, they are not impossible. Both parties can agree to modify the terms, but this usually requires a written amendment.

Many lenders, including credit unions, online lenders, and private individuals, also use loan agreements. It’s not just a bank thing.

Reading the agreement is crucial. Understanding your rights and obligations can prevent future misunderstandings.

Lenders also have rights and responsibilities outlined in the agreement. It protects both parties involved.

After signing, borrowers should keep track of payments and terms. It’s important to stay informed throughout the loan period.

Written agreements provide clear evidence of terms and conditions. Verbal agreements can lead to disputes and are harder to enforce.