Get Mortgage Statement Form in PDF

Get Mortgage Statement Form in PDF

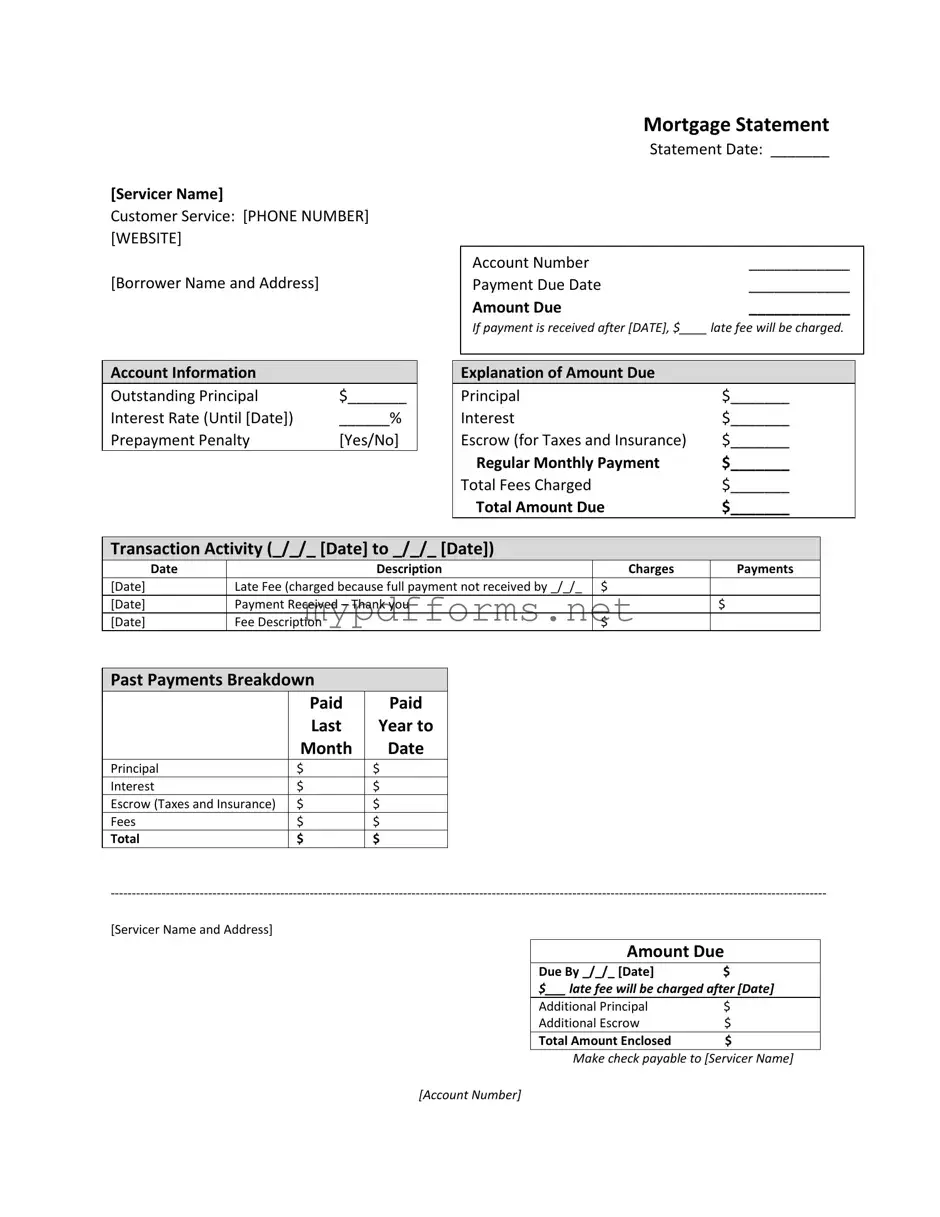

The Mortgage Statement form is an essential document that provides borrowers with a comprehensive overview of their mortgage account. This form includes crucial details such as the servicer's name, customer service contact information, and the borrower's name and address. At the top, the statement lists the date it was issued, the account number, and the payment due date, along with the total amount due. If a payment is not made by the specified date, the borrower should be aware of the late fee that will be incurred. The account information section breaks down the outstanding principal, interest rate, and whether a prepayment penalty applies. Further, it clarifies the components of the amount due, including principal, interest, and escrow for taxes and insurance. Transaction activity is documented over a specified date range, detailing charges and payments made, including any late fees. The form also provides a breakdown of past payments, offering insight into the borrower's payment history. Important messages highlight the implications of partial payments and delinquency notices, ensuring borrowers understand the consequences of late payments. Additionally, resources for mortgage counseling or assistance are available for those experiencing financial difficulties, emphasizing the servicer's commitment to supporting borrowers in challenging times.

When filling out the Mortgage Statement form, it is important to follow specific guidelines to ensure accuracy and compliance. Below are six recommendations on what to do and what to avoid.

Paystubs for Independent Contractor - Promotes financial literacy among independent contractors.

An Illinois Non-disclosure Agreement form is a legal document used to protect confidential information. It is designed to be signed by individuals or businesses that wish to share sensitive data while legally preventing the other party from disclosing it. For those looking to secure their information, just click the button below to start filling out your form, or visit Illinois Forms for more resources.

Lost Title Alabama - Make sure to include the current Alabama title secured with the application.

When filling out and using the Mortgage Statement form, it is essential to pay attention to several key aspects to ensure clarity and compliance. Below are important takeaways to consider:

By keeping these takeaways in mind, you can navigate your mortgage statement more effectively and take proactive steps in managing your mortgage obligations.

Completing the Mortgage Statement form is an important step in managing your mortgage payments effectively. This form provides essential details about your account, payment history, and any fees that may apply. To ensure accuracy and avoid delays, follow the steps outlined below carefully.

Once you have filled out the form completely, double-check for accuracy. This will help you avoid potential issues with your mortgage account. After confirming that all information is correct, you can submit the form as instructed by your servicer.

What is a Mortgage Statement?

A Mortgage Statement is a document provided by your mortgage servicer that outlines the details of your mortgage account. It includes information such as the amount due, payment due date, outstanding principal balance, interest rate, and any fees charged. This statement helps you keep track of your mortgage payments and understand your current financial obligations.

How can I contact my mortgage servicer for questions about my statement?

You can reach your mortgage servicer’s customer service by calling the phone number listed on your Mortgage Statement. Additionally, you may visit their website for further assistance. It is important to have your account number handy when you contact them to expedite the process.

What happens if I miss my payment due date?

If your payment is not received by the due date, a late fee will be charged as indicated on your Mortgage Statement. The specific amount of the late fee will be detailed in the statement. It is crucial to make your payments on time to avoid additional fees and potential negative impacts on your credit score.

What does the amount due on my Mortgage Statement include?

The amount due typically includes several components: principal, interest, and escrow for taxes and insurance. Each of these elements is broken down in your statement, allowing you to see exactly what you are paying for each month. Regular monthly payments and any fees charged will also be included in the total amount due.

What is a prepayment penalty?

A prepayment penalty is a fee that may be charged if you pay off your mortgage loan early. Not all loans have this penalty, and it will be indicated on your Mortgage Statement. If you are considering making additional payments towards your principal, it is wise to check whether a prepayment penalty applies to your loan.

What should I do if I am experiencing financial difficulty?

If you are facing financial challenges, it is important to take action. Your Mortgage Statement may provide information about mortgage counseling or assistance programs on the back. Reaching out to your servicer as soon as possible can help you explore options to avoid delinquency and potential foreclosure.

What are partial payments and how are they handled?

Partial payments are amounts that do not cover the full payment due on your mortgage. According to your Mortgage Statement, any partial payments made will not be applied to your mortgage balance. Instead, they are held in a separate suspense account until the full payment is made. Once the balance of the partial payment is received, it will then be applied to your mortgage.

How can I ensure my mortgage payments are applied correctly?

To ensure that your payments are applied correctly, always make your payments in full and on time. Review your Mortgage Statement for accuracy and keep records of your payments. If you notice any discrepancies, contact your servicer immediately to resolve any issues.

The first document similar to a Mortgage Statement is a Billing Statement. This document provides a summary of what is owed for a specific period. It includes details like the amount due, due date, and any late fees. Just like a mortgage statement, a billing statement helps the borrower keep track of their payments and understand their financial obligations.

Another related document is the Loan Statement. This statement outlines the terms of a loan, including the principal balance, interest rate, and payment history. Similar to a mortgage statement, it provides a clear picture of the borrower's current financial status regarding the loan. Both documents serve to inform the borrower about their financial responsibilities and any outstanding balances.

When dealing with motorcycle ownership in North Carolina, it's vital to have the appropriate documentation to facilitate the sale effectively. The North Carolina Motorcycle Bill of Sale form can be accessed easily at motorcyclebillofsale.com/free-north-carolina-motorcycle-bill-of-sale/, ensuring that both buyers and sellers adhere to the necessary legal requirements while making the transaction as seamless as possible.

A Payment History Report is also comparable to a Mortgage Statement. This report details all the payments made over a certain period, showing dates, amounts, and any fees incurred. Like a mortgage statement, it helps borrowers track their payment patterns and identify any issues that may arise, such as missed payments or late fees.

The Escrow Statement is another similar document. It breaks down the escrow account, showing how much money is set aside for property taxes and insurance. This document is important for homeowners, as it reflects the same escrow information found in a mortgage statement. Both statements help borrowers understand how their payments are allocated.

A Property Tax Statement shares similarities with a Mortgage Statement as well. It provides details on property taxes owed, including due dates and amounts. Just like a mortgage statement, it helps homeowners stay informed about their financial obligations related to their property, ensuring they do not miss important payments.

The Annual Mortgage Statement is also worth mentioning. This document summarizes the mortgage payments made over the past year, including principal and interest paid. It serves a similar purpose as a mortgage statement by providing an overview of the borrower’s financial activity related to their mortgage, making it easier to prepare for tax season.

Finally, a Credit Report can be seen as a related document. While it does not provide specific payment details, it reflects the borrower's credit history, including mortgage payments. Like a mortgage statement, it plays a crucial role in understanding the borrower’s financial health and can impact future borrowing opportunities.

When managing a mortgage, several important documents accompany the Mortgage Statement form. These documents serve various purposes, providing essential information about the loan, payment history, and any potential issues. Below is a list of five common forms and documents that are often used alongside the Mortgage Statement.

Understanding these documents is crucial for borrowers to manage their mortgage effectively. Each form plays a role in maintaining clear communication between the borrower and lender, ensuring that both parties are aware of their rights and responsibilities throughout the life of the loan.

Understanding your mortgage statement is crucial for managing your home loan effectively. However, there are several misconceptions that can lead to confusion. Here are seven common misconceptions:

By clarifying these misconceptions, homeowners can better navigate their mortgage responsibilities and avoid unnecessary stress.