Attorney-Verified Deed in Lieu of Foreclosure Document for New York

Attorney-Verified Deed in Lieu of Foreclosure Document for New York

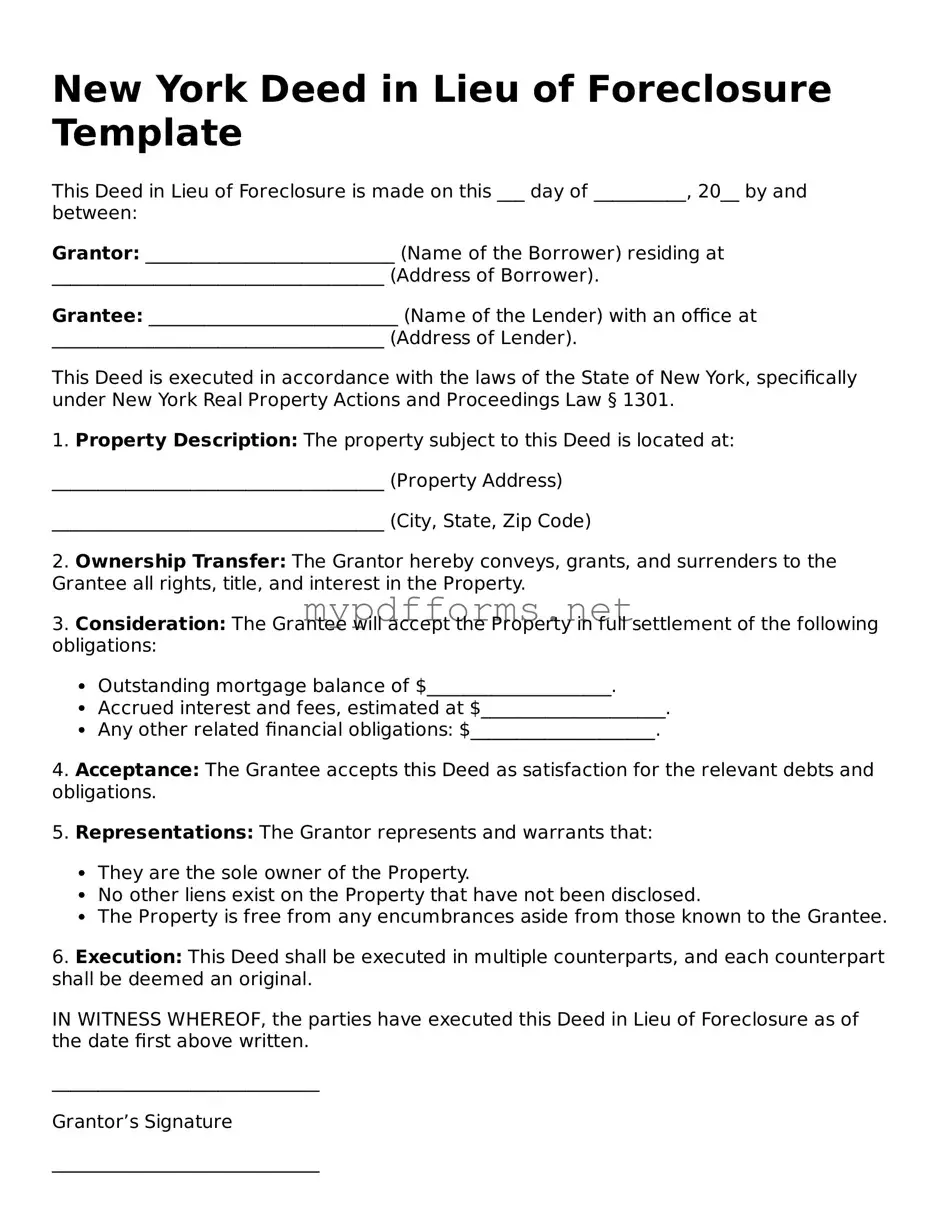

The New York Deed in Lieu of Foreclosure form serves as a critical tool for homeowners facing the possibility of foreclosure. This legal document allows property owners to voluntarily transfer ownership of their property to the lender in exchange for the cancellation of their mortgage debt. By utilizing this form, homeowners can avoid the lengthy and often stressful foreclosure process, thereby protecting their credit score and minimizing the emotional toll associated with losing a home. The form outlines essential details, including the property description, the parties involved, and the specific terms of the transfer. It also addresses potential liabilities, ensuring that both the homeowner and the lender understand their rights and responsibilities. This option can be particularly appealing for those seeking a more dignified exit from homeownership, as it provides a clear path to resolving mortgage issues while potentially preserving the homeowner's financial future.

When filling out the New York Deed in Lieu of Foreclosure form, it is essential to follow specific guidelines to ensure accuracy and compliance. Below are four important do's and don'ts to consider:

Deed in Lieu of Foreclosure Texas - In some cases, this deed might lead to favorable terms or incentives from the lender for rapid resolution.

Having a reliable General Power of Attorney is crucial for managing your affairs effectively, especially in unforeseen circumstances, and for those looking to formalize this arrangement, the Illinois Forms provide an excellent resource to aid in the process.

When dealing with a Deed in Lieu of Foreclosure in New York, it's essential to understand the process and implications. Here are some key takeaways to keep in mind:

Taking these steps can help ensure a smoother experience as you navigate this challenging situation.

Filling out the New York Deed in Lieu of Foreclosure form is an important step in the process of transferring property ownership. Once you have completed the form, you will need to ensure it is properly signed and submitted to the relevant authorities. Here’s how to fill out the form correctly.

After submitting the form, keep a copy for your records. This will help you track the progress and provide proof of the transfer if needed in the future.

A Deed in Lieu of Foreclosure is a legal process that allows a homeowner to transfer ownership of their property back to the lender to avoid foreclosure. This option is typically pursued when the homeowner is unable to keep up with mortgage payments and wants to mitigate the negative impact of foreclosure on their credit. By voluntarily giving the property back to the lender, the homeowner may be able to avoid the lengthy and costly foreclosure process.

There are several advantages to consider:

Yes, there are some risks to consider:

The process typically begins by contacting your lender. You should explain your financial situation and express your interest in a Deed in Lieu. The lender will likely require you to provide documentation of your financial hardship. After reviewing your situation, they may offer you a Deed in Lieu agreement. It is advisable to consult with a legal professional to ensure that you fully understand the implications and to help navigate the process effectively.

The New York Deed in Lieu of Foreclosure form shares similarities with a mortgage modification agreement. Both documents aim to provide a solution to distressed homeowners facing financial difficulties. A mortgage modification agreement involves changing the terms of an existing mortgage to make payments more manageable. This may include lowering the interest rate, extending the loan term, or even reducing the principal amount owed. By contrast, a deed in lieu of foreclosure transfers ownership of the property to the lender, allowing the homeowner to avoid the lengthy foreclosure process. Both options seek to alleviate the burden on the homeowner while providing a resolution for the lender.

Another document that resembles the Deed in Lieu of Foreclosure is a short sale agreement. In a short sale, the homeowner sells the property for less than the outstanding mortgage balance, with the lender’s approval. This process allows the homeowner to avoid foreclosure while still settling their debt. Similar to a deed in lieu, a short sale can help preserve the homeowner's credit score and provide a fresh start. However, while a deed in lieu transfers ownership directly to the lender, a short sale involves selling the property to a third party, which may take longer and require more effort from the homeowner.

A third similar document is a forbearance agreement. This type of agreement allows homeowners to temporarily pause or reduce their mortgage payments due to financial hardship. During the forbearance period, lenders typically agree not to initiate foreclosure proceedings. Like a deed in lieu, the goal is to keep the homeowner in their property and avoid foreclosure. However, while a deed in lieu results in the homeowner relinquishing ownership, a forbearance agreement allows them to retain ownership while they work through their financial challenges.

A Quitclaim Deed is a legal instrument that facilitates the transfer of property rights between parties without any assurance of the title's clarity. This can become particularly useful in circumstances involving financial distress, as it helps resolve ownership complexities swiftly. If you're looking for a fillable form to create a Washington Quitclaim Deed, you can find it at https://quitclaimdocs.com/fillable-washington-quitclaim-deed.

Another document that aligns with the Deed in Lieu of Foreclosure is a loan assumption agreement. In this scenario, a third party takes over the mortgage obligations from the original borrower. This can occur when a homeowner sells their property to someone who assumes the existing mortgage. Both a loan assumption and a deed in lieu provide a way to resolve mortgage issues without going through foreclosure. However, in a loan assumption, the original homeowner may still have some liability for the mortgage, while a deed in lieu fully absolves the homeowner from their mortgage responsibilities.

Lastly, a bankruptcy filing can also be compared to a Deed in Lieu of Foreclosure. Filing for bankruptcy offers individuals a legal way to reorganize or eliminate their debts, including mortgage obligations. While both options can prevent foreclosure, bankruptcy can provide a broader financial reset, impacting all debts, not just the mortgage. A deed in lieu, on the other hand, specifically addresses the mortgage and transfers property ownership to the lender. Each option has its own implications for credit scores and future borrowing, making it essential for homeowners to consider their unique circumstances when deciding which path to take.

When dealing with a Deed in Lieu of Foreclosure in New York, several other forms and documents may be necessary to ensure a smooth process. Each of these documents serves a specific purpose and helps clarify the terms of the transaction. Below is a list of commonly used forms that accompany the Deed in Lieu of Foreclosure.

Having these documents prepared and organized can help streamline the process of completing a Deed in Lieu of Foreclosure. It’s important to understand each document's role to avoid potential issues down the line.

Understanding the Deed in Lieu of Foreclosure in New York can be challenging due to various misconceptions. Here are nine common misunderstandings about this legal process:

Being informed about these misconceptions can help homeowners make better decisions regarding their options in the face of foreclosure. Understanding the realities of a deed in lieu of foreclosure is crucial for navigating this complex process.