Attorney-Verified Promissory Note Document for New York

Attorney-Verified Promissory Note Document for New York

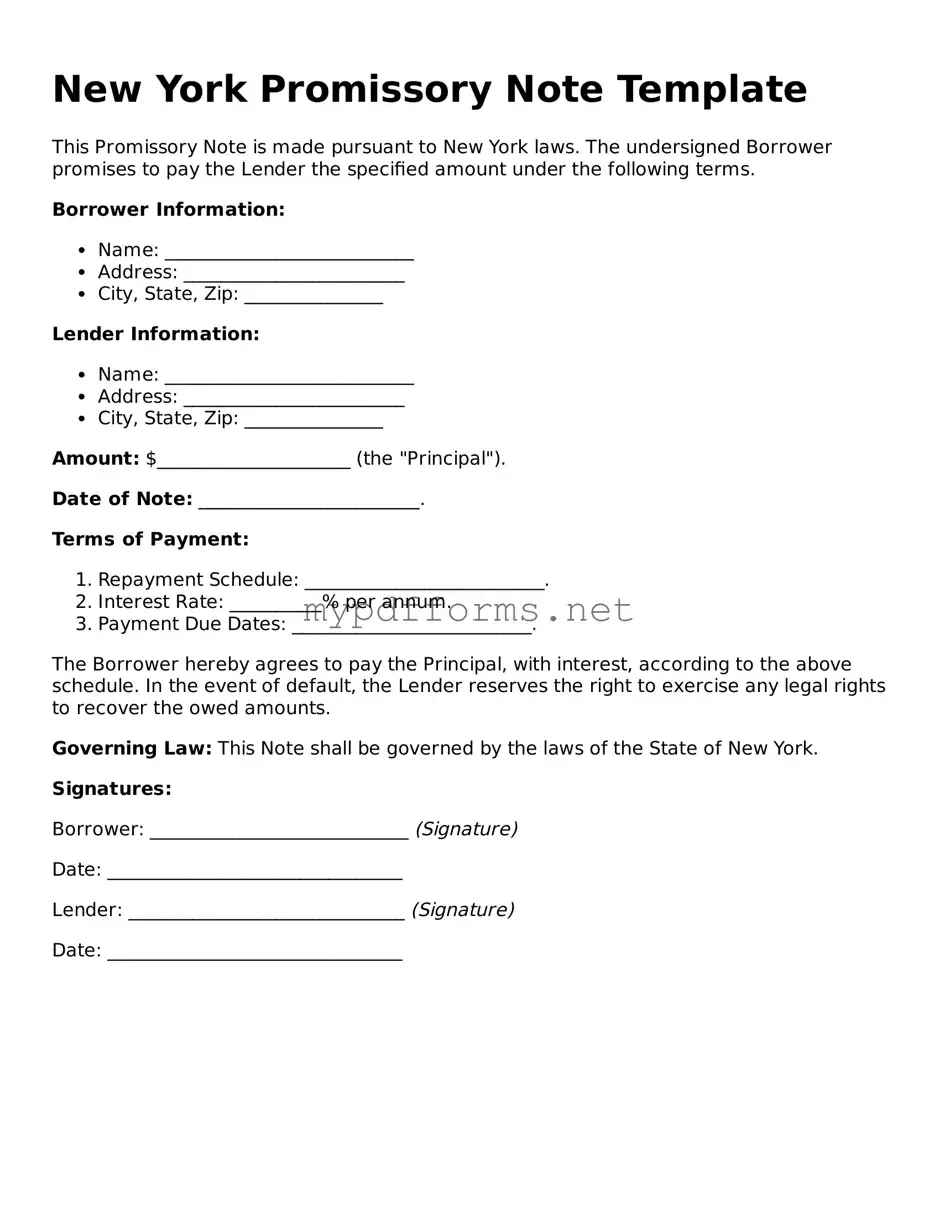

When engaging in financial transactions, clarity and security are paramount, and the New York Promissory Note form serves as a vital tool in achieving these objectives. This legally binding document outlines the terms under which one party agrees to pay a specified sum of money to another party at a defined future date or upon demand. Key components of the form include the principal amount, interest rate, repayment schedule, and the identities of both the borrower and lender. Additionally, it often includes provisions for default, detailing the consequences if the borrower fails to meet their obligations. Understanding this form is essential for anyone involved in lending or borrowing money in New York, as it not only protects the lender's interests but also clarifies the borrower's responsibilities. By using a well-structured Promissory Note, parties can minimize misunderstandings and ensure that all terms are agreed upon before any funds are exchanged.

When filling out the New York Promissory Note form, it's essential to be careful and precise. Here’s a helpful list of things you should and shouldn't do:

Free Promissory Note Template Florida - It is important to keep a copy of the promissory note for personal records.

The Maryland Mobile Home Bill of Sale document is essential for any seller to ensure a proper and legal transfer. Learn how to efficiently use this form by visiting our resource on the indispensable documentation of the Mobile Home Bill of Sale for your needs. indispensable documentation of the Mobile Home Bill of Sale

Loan Agreement Template Texas - A promissory note can be transferred to another party through endorsement.

When filling out and using the New York Promissory Note form, keep the following key takeaways in mind:

By following these guidelines, you can effectively fill out and utilize the New York Promissory Note form, ensuring clarity and protection for all parties involved.

Filling out the New York Promissory Note form is an important step in formalizing a loan agreement. After completing the form, both parties should review it carefully to ensure accuracy. Once the form is filled out, it may need to be signed in front of a notary public, depending on specific requirements.

A promissory note is a written promise to pay a specified amount of money to a designated person or entity at a particular time or on demand. It serves as a legal document that outlines the terms of the loan, including the amount borrowed, interest rate, payment schedule, and any penalties for late payment.

In New York, a promissory note is essential for both lenders and borrowers. It protects the lender's rights by providing a clear record of the loan agreement, while also giving the borrower a structured repayment plan. This document can help avoid misunderstandings and disputes in the future.

A typical New York promissory note includes:

While it is not legally required to have a lawyer draft a promissory note, it can be beneficial. A lawyer can ensure that the document complies with New York laws and accurately reflects the intentions of both parties. However, many templates are available online for those who prefer to create one independently.

Yes, a promissory note is a legally binding contract. Once both parties sign it, they are obligated to adhere to its terms. If either party fails to meet their obligations, the other party may take legal action to enforce the agreement.

Yes, a promissory note can be modified, but both parties must agree to the changes. It is advisable to document any modifications in writing and have both parties sign the amended note to avoid confusion later on.

If a borrower defaults on a promissory note, the lender has several options. They may initiate collection efforts, charge late fees, or take legal action to recover the owed amount. The consequences of default can be serious, including damage to the borrower’s credit score and potential legal repercussions.

A promissory note is a financial document that outlines a borrower's promise to repay a loan. It is similar to a loan agreement, which also details the terms of borrowing. A loan agreement typically includes the loan amount, interest rate, repayment schedule, and any collateral involved. Unlike a promissory note, which is a simple promise to pay, a loan agreement can be more complex, covering additional legal obligations and rights of both parties. Both documents serve to protect the lender's interests while providing clarity to the borrower regarding their repayment responsibilities.

A mortgage is another document that shares similarities with a promissory note. In a mortgage, the borrower secures a loan for real estate, and the property itself serves as collateral. The promissory note is often part of the mortgage package, where it specifies the borrower's promise to repay the loan. While the mortgage outlines the rights of the lender to foreclose on the property if payments are not made, the promissory note focuses solely on the repayment promise. Both documents work together to establish the terms of the loan and the consequences of default.

A personal guarantee can also be compared to a promissory note. In this case, an individual agrees to be responsible for a loan taken out by a business. This guarantee provides the lender with additional security. Like a promissory note, a personal guarantee is a commitment to pay back the borrowed amount. However, it extends beyond the business's assets, holding the individual personally accountable. Both documents help lenders assess risk and ensure repayment, but a personal guarantee adds a layer of personal responsibility.

A loan application is another document that shares some characteristics with a promissory note. While a promissory note is a commitment to repay, a loan application is the initial request for funds. The application collects information about the borrower’s financial situation, including income, credit history, and existing debts. This information helps lenders decide whether to issue a loan. Although the two documents serve different purposes, they are interconnected in the lending process, with the application leading to the creation of a promissory note if the loan is approved.

An installment agreement is similar to a promissory note in that it outlines a payment plan for repaying a debt. This document specifies the total amount owed, the number of payments, and the due dates. While a promissory note is a straightforward promise to pay, an installment agreement breaks down the repayment into smaller, manageable amounts. Both documents aim to facilitate repayment but do so in different formats. An installment agreement may offer more detailed terms regarding payment schedules than a standard promissory note.

A forbearance agreement can also be compared to a promissory note. In a forbearance agreement, a lender allows a borrower to temporarily pause or reduce payments due to financial hardship. This document outlines the new terms of repayment during the forbearance period. While a promissory note establishes the original repayment terms, a forbearance agreement modifies those terms to accommodate the borrower’s situation. Both documents are essential in managing debt and ensuring that borrowers can continue to meet their obligations under changing circumstances.

In the realm of motorcycle transactions, the importance of using a Minnesota Motorcycle Bill of Sale cannot be overstated, as it serves as a formal record that facilitates a seamless transfer of ownership. For those looking to understand this essential document further, comprehensive resources can be found at https://motorcyclebillofsale.com/free-minnesota-motorcycle-bill-of-sale/, ensuring clarity on the vital elements involved in the sale.

Lastly, a deed of trust is another document that bears similarities to a promissory note. A deed of trust is used in real estate transactions to secure a loan, with a third party holding the title until the loan is repaid. The promissory note, in this case, serves as the borrower's promise to repay the loan. While the deed of trust provides the lender with security over the property, the promissory note focuses on the borrower's commitment. Both documents work together to facilitate the lending process and protect the lender’s interests.

A New York Promissory Note is a crucial document used to outline the terms of a loan between a borrower and a lender. Along with this note, several other forms and documents are often utilized to ensure clarity and protection for both parties involved. Below are some commonly associated documents.

Utilizing these documents alongside the New York Promissory Note can help create a clear framework for the loan transaction. This clarity benefits both the borrower and the lender, reducing the potential for misunderstandings and disputes in the future.

Understanding the New York Promissory Note form can be tricky, and there are several misconceptions that often arise. Here’s a breakdown of eight common misunderstandings:

By clarifying these misconceptions, you can better navigate the process of creating and using a New York Promissory Note effectively.