Owner Financing Contract Template

Owner Financing Contract Template

Owner financing has become an increasingly popular option for buyers and sellers in real estate transactions, offering flexibility and potential financial benefits. The Owner Financing Contract form serves as a crucial document in this process, outlining the terms and conditions under which the seller provides financing to the buyer. Key components of the form include the purchase price, interest rate, payment schedule, and the duration of the loan. It also specifies the responsibilities of both parties, including property maintenance and insurance requirements. Additionally, the form addresses what happens in the event of a default, ensuring that both parties understand their rights and obligations. This contract not only facilitates a smoother transaction but also helps to protect the interests of both the buyer and the seller throughout the financing period.

When filling out an Owner Financing Contract form, it's essential to approach the task with care. Here are five things you should do and five things you should avoid.

What Is a Personal Guarantor - Some businesses may find it difficult to operate without providing personal guarantees.

Buyer's Agent Termination Letter Sample - Ensures all parties are clear on the cancellation.

The New York Real Estate Purchase Agreement form is a legally binding document that outlines the terms and conditions under which a piece of real estate will be sold and purchased. It details everything from the price to the responsibilities of both the buyer and the seller. For more information and to access the form itself, you can visit https://nyforms.com/real-estate-purchase-agreement-template. Understanding this form is essential for anyone looking to navigate the complexities of buying or selling property in New York.

Purchase Agreement Addendum - Mitigate misunderstandings with clear and documented changes.

When using the Owner Financing Contract form, keep the following key points in mind:

When preparing to fill out the Owner Financing Contract form, it's essential to gather all necessary information about the property, the buyer, and the seller. This form will help outline the terms of the financing agreement, ensuring that both parties are clear on their obligations and rights. Follow these steps carefully to complete the form accurately.

Once you have completed the form, review it carefully for any errors or missing information. This contract is a crucial document that protects both parties, so accuracy is key. After verification, provide copies to all involved parties and keep one for your records.

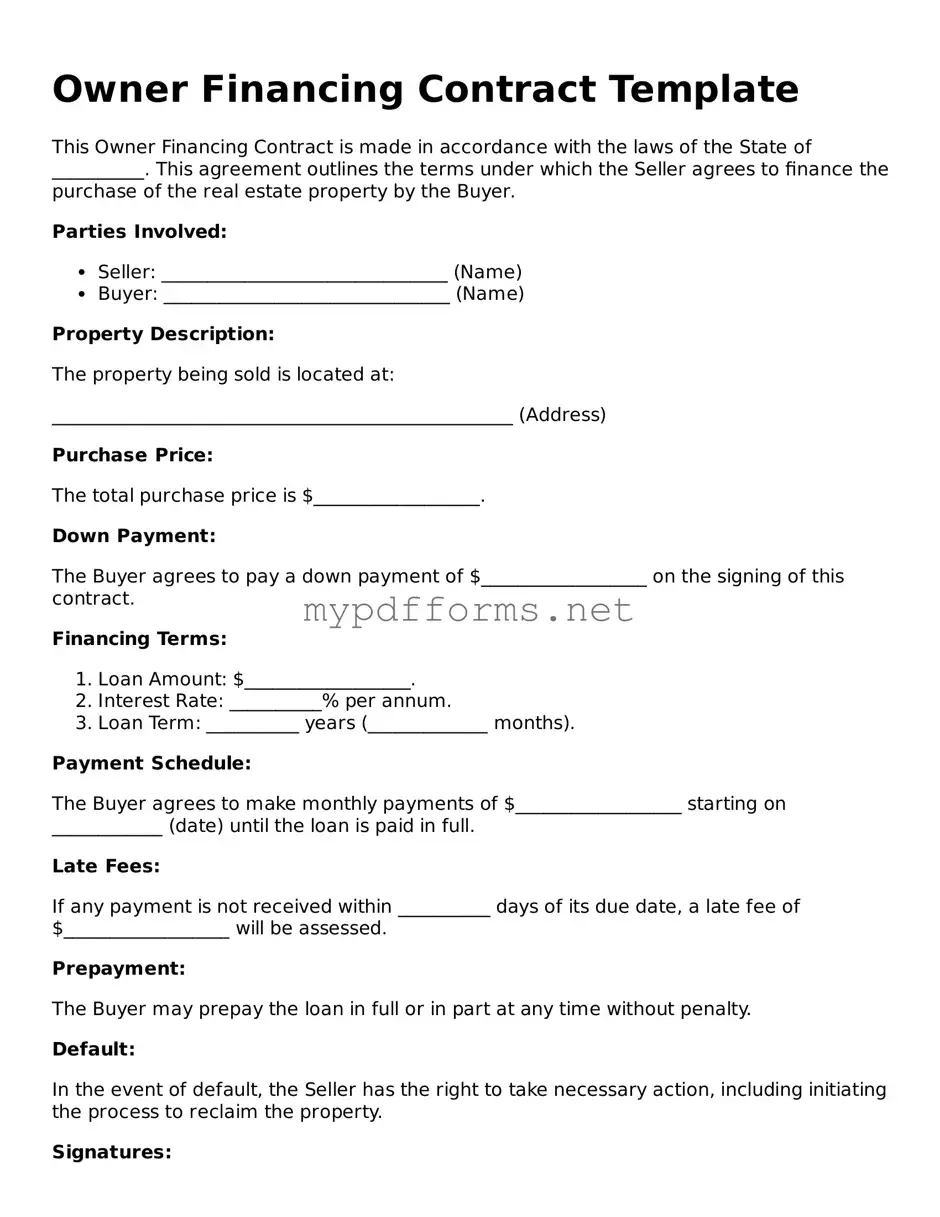

An Owner Financing Contract is an agreement between a seller and a buyer in which the seller provides financing to the buyer to purchase the property. Instead of the buyer obtaining a traditional mortgage from a bank or financial institution, the seller allows the buyer to make payments directly to them. This arrangement can be beneficial for both parties, as it can facilitate a quicker sale and provide the buyer with more flexible financing options.

Both buyers and sellers can benefit from Owner Financing. Buyers who may struggle to qualify for a traditional mortgage due to credit issues or lack of sufficient down payment can find this option appealing. Sellers, on the other hand, can attract a larger pool of potential buyers, expedite the sale process, and may even receive a higher sale price. Additionally, sellers can earn interest on the financed amount, providing them with a steady income stream.

Several key terms should be clearly outlined in an Owner Financing Contract. These include:

It’s important for both parties to discuss these terms thoroughly to ensure clarity and mutual agreement.

Yes, there are risks involved for both buyers and sellers. Buyers may face the risk of losing their investment if they default on payments. Sellers, on the other hand, might encounter challenges if the buyer fails to make payments or damages the property. It is crucial for both parties to conduct due diligence and consider legal advice to mitigate these risks. Properly drafted contracts can help protect both parties’ interests.

Yes, an Owner Financing Contract can be modified after it is signed, but both parties must agree to any changes. It is advisable to document any modifications in writing to avoid misunderstandings in the future. This may include changes to payment amounts, due dates, or other terms. Consulting with a legal professional can help ensure that modifications are made correctly and are enforceable.

The Owner Financing Contract is similar to a Lease Purchase Agreement. In a Lease Purchase Agreement, a tenant has the option to buy the property after a specified lease period. Like owner financing, this arrangement allows the buyer to occupy the home while making payments, but it also includes a rental component. This can be beneficial for buyers who may not be ready to secure a mortgage immediately but want to lock in a purchase price and work towards ownership.

Another document that shares similarities is the Land Contract, also known as a Contract for Deed. In this arrangement, the seller retains the title to the property until the buyer has paid the full purchase price. Similar to owner financing, the buyer makes regular payments to the seller, but they do not receive ownership until the contract terms are fulfilled. This option can provide flexibility for buyers who may face challenges in obtaining traditional financing.

A Promissory Note is also related to the Owner Financing Contract. This document outlines the borrower's promise to repay the loan under specific terms, such as interest rate and payment schedule. In owner financing, the promissory note serves as a key component, detailing the financial obligations between the buyer and seller. It provides legal assurance to the seller that the buyer is committed to fulfilling their payment obligations.

The Mortgage Agreement is another document that shares characteristics with owner financing. A mortgage agreement is a formal loan document that secures the loan with the property as collateral. While owner financing does not typically involve a bank, the principles are similar in that the seller holds a security interest in the property until the buyer pays off the loan. This agreement protects both parties by clarifying the terms of the financing arrangement.

The Installment Sale Agreement is also comparable to the Owner Financing Contract. This agreement allows the buyer to make payments over time while taking possession of the property. Like owner financing, the seller retains some rights until the purchase price is fully paid. This type of arrangement can be appealing to buyers who prefer to spread out their payments rather than securing a large loan upfront.

A Real Estate Purchase Agreement is another relevant document. This contract outlines the terms and conditions of the sale between the buyer and seller. While it can involve traditional financing, it can also accommodate owner financing terms. Both documents serve to protect the interests of both parties, ensuring that all aspects of the transaction are clearly defined.

In navigating the complexities of real estate transactions, it is crucial for buyers and sellers to familiarize themselves with various legal documents, including the Colorado PDF Forms, which provide essential resources like the Real Estate Purchase Agreement. This understanding not only equips them with the knowledge to make informed decisions but also aids in ensuring that all terms and obligations are clearly outlined, thereby minimizing any potential ambiguities in the contractual relationship.

Finally, a Seller Financing Addendum can be similar to the Owner Financing Contract. This addendum is often attached to a standard purchase agreement to specify the terms of seller financing. It outlines the interest rate, payment schedule, and other relevant details. This addendum allows for flexibility in negotiations and can make the transaction more appealing to buyers who may not qualify for traditional loans.

When engaging in an owner financing agreement, several additional documents are often necessary to ensure clarity and protection for both parties involved. These documents support the terms outlined in the Owner Financing Contract and help facilitate a smooth transaction.

Having these documents in place is crucial for protecting the interests of both the buyer and the seller. They provide a clear framework for the transaction and help prevent misunderstandings or disputes in the future.

Owner financing can be a beneficial option for both buyers and sellers, but several misconceptions can lead to misunderstandings. Here are ten common misconceptions about the Owner Financing Contract form:

This is not true. While owner financing can help buyers with less-than-perfect credit, it is also a viable option for buyers with good credit who prefer more flexible terms.

In reality, any property owner can offer financing. This includes individual homeowners who want to sell their property.

While it does require some paperwork, the process can be straightforward. Clear terms and communication can simplify the transaction significantly.

Most sellers will expect some form of down payment. This shows the buyer's commitment and helps mitigate the seller's risk.

Owner financing is legal in all states, though specific regulations may vary. It is essential to understand local laws to ensure compliance.

In fact, many aspects of the financing terms can be negotiated. This includes interest rates, payment schedules, and other conditions.

Owner financing can be used for both residential and commercial properties, providing flexibility for various types of transactions.

A written contract is crucial to protect both parties. It outlines the terms and conditions, ensuring clarity and reducing potential disputes.

Many buyers and sellers choose owner financing as a strategic option rather than a last resort. It can be beneficial for both parties under the right circumstances.

Sellers can still maintain some level of control, especially if they include clauses that protect their interests, such as late payment penalties or default terms.