Get Profit And Loss Form in PDF

Get Profit And Loss Form in PDF

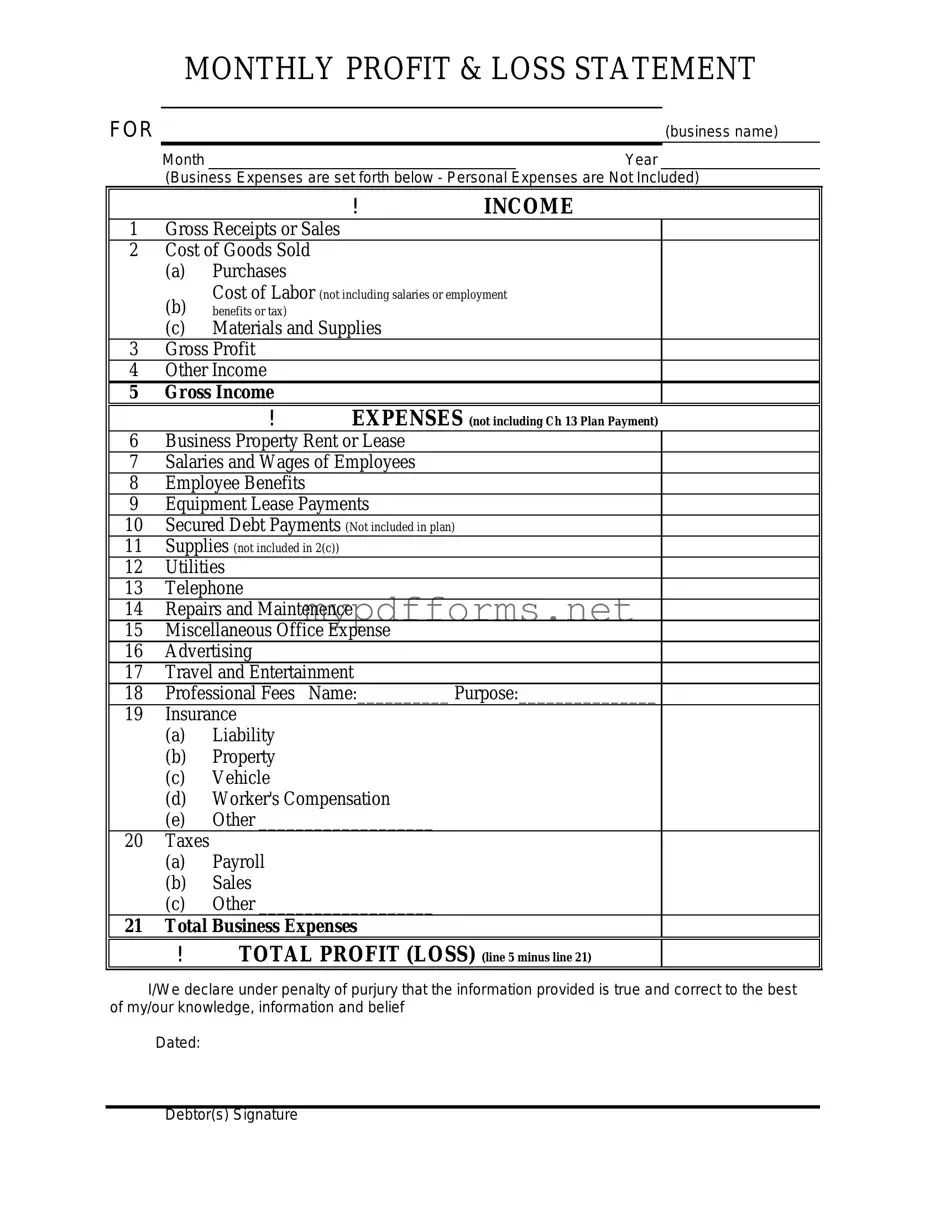

The Profit and Loss form, often referred to as the P&L statement, serves as a crucial financial document for businesses of all sizes. It provides a snapshot of a company's revenues, costs, and expenses over a specific period, typically a month, quarter, or year. This form not only helps in assessing the overall financial health of a business but also plays a vital role in strategic decision-making. By detailing income sources and outlining various expenses, the P&L statement enables business owners and stakeholders to identify trends, manage budgets, and evaluate profitability. Additionally, it can highlight areas where cost reductions may be possible or where revenue growth is needed. Understanding how to read and interpret this form is essential for anyone looking to gain insights into a company's operational efficiency and financial performance.

When filling out a Profit and Loss form, it's important to be accurate and thorough. Here are some dos and don'ts to keep in mind:

What Is W9 Form - It helps identify whether you are subject to certain tax reporting rules.

For those exploring the intricacies of property transfers, the comprehensive North Carolina bill of sale document is indispensable. This form not only simplifies the exchange process but also serves to protect both buyer and seller. For more information, consider reviewing the guidelines on the Bill of Sale associated with your transaction needs.

Indirect Signature Required - FedEx retains the right to use discretion regarding safety and security during delivery.

Dmv 262 - The power of attorney does not allow completion of the odometer section.

When filling out and using the Profit and Loss form, consider the following key takeaways:

Filling out the Profit and Loss form is an important step in tracking your business’s financial performance. This document helps you summarize your income and expenses over a specific period. By completing this form accurately, you can gain insights into your profitability and make informed decisions for your business. Follow these steps to ensure you fill out the form correctly.

What is a Profit and Loss form?

A Profit and Loss form, often referred to as a P&L statement, is a financial document that summarizes the revenues, costs, and expenses incurred during a specific period of time, usually a fiscal quarter or year. This form provides insights into a business's ability to generate profit by increasing revenue and reducing costs.

Why is the Profit and Loss form important?

The Profit and Loss form is crucial for several reasons. It helps business owners understand their financial performance, allowing them to make informed decisions. Investors and lenders also rely on this document to assess the viability and profitability of a business before committing funds. Furthermore, it serves as a tool for tracking financial trends over time.

What are the key components of a Profit and Loss form?

The main components of a Profit and Loss form include:

How often should a Profit and Loss form be completed?

Businesses typically prepare a Profit and Loss form on a monthly, quarterly, or annual basis. The frequency can depend on the size of the business and its financial needs. Smaller businesses may find monthly reports beneficial for tracking performance closely, while larger organizations may focus on quarterly or annual reports.

How can I use the Profit and Loss form to improve my business?

By regularly reviewing the Profit and Loss form, you can identify trends in revenue and expenses. This analysis can highlight areas where costs can be reduced or revenue can be increased. For example, if you notice a consistent decline in gross profit, it may be time to reevaluate pricing strategies or reduce operational costs.

What is the difference between gross profit and net profit?

Gross profit is the amount remaining after subtracting the cost of goods sold from total revenue. It reflects the efficiency of production and sales. Net profit, on the other hand, is the final profit after all expenses, including operating expenses, taxes, and interest, have been deducted. It provides a more comprehensive view of a business's profitability.

Can I prepare a Profit and Loss form myself?

Yes, many business owners prepare their own Profit and Loss forms, especially in small businesses. However, it is essential to ensure accuracy and completeness. Utilizing accounting software can simplify the process. Alternatively, consulting with a financial professional can provide additional insights and help ensure that the form meets all necessary standards.

What should I do if my Profit and Loss form shows a loss?

If your Profit and Loss form indicates a loss, it is important to analyze the underlying reasons. Look for patterns in expenses and revenue. Consider whether it is a temporary situation or a sign of deeper issues. Developing a plan to address these issues, such as cutting unnecessary costs or finding new revenue streams, can help stabilize your business moving forward.

The Profit and Loss (P&L) statement, also known as the income statement, is similar to the Balance Sheet. While the P&L shows revenues and expenses over a specific period, the Balance Sheet provides a snapshot of a company’s assets, liabilities, and equity at a single point in time. Together, they offer a comprehensive view of a company's financial health. The P&L focuses on performance, while the Balance Sheet emphasizes the financial position.

The Cash Flow Statement is another document closely related to the P&L. It tracks the flow of cash in and out of a business during a given period. While the P&L records revenues and expenses, the Cash Flow Statement highlights how those transactions affect cash availability. Understanding both documents is essential for assessing liquidity and operational efficiency.

The Statement of Retained Earnings complements the P&L by showing how profits are reinvested in the business. It starts with the net income from the P&L and adjusts for dividends paid out. This document helps stakeholders understand how much profit is retained for growth versus what is distributed to shareholders.

The Budget is a forward-looking document that outlines expected revenues and expenses for a future period. It serves as a financial plan, guiding decision-making and resource allocation. While the P&L reflects past performance, the Budget sets the target for future performance, making both essential for strategic planning.

The Trial Balance is a summary of all ledger accounts, including revenues and expenses. It ensures that total debits equal total credits, serving as a preliminary check before preparing financial statements. The P&L is derived from this document, which confirms the accuracy of financial data before final reporting.

The Income Tax Return is similar to the P&L in that it summarizes income and expenses for tax purposes. It reflects the net income reported on the P&L but includes specific adjustments required by tax regulations. This document is crucial for compliance and tax planning, making it an important counterpart to the P&L.

The Financial Forecast is a projection of future revenues and expenses, similar to the Budget but often more detailed. It uses historical P&L data to predict future performance based on various scenarios. This document is vital for assessing potential growth and preparing for market changes.

The Sales Report provides detailed insights into revenue generation, focusing on sales performance over a specific period. While the P&L summarizes overall revenues, the Sales Report breaks down sales by product, region, or channel. This granularity helps businesses identify trends and make informed decisions.

Understanding the implications of financial documentation is crucial for any business, and for those managing personal affairs, a similar attention to detail is necessary when dealing with legal matters. For instance, the Illinois Power of Attorney form is essential for individuals wanting to designate someone to handle decisions on their behalf, covering various aspects from financial to healthcare. For those looking to ensure their decisions are in trusted hands, completing an Illinois Power of Attorney form is a crucial step. To access such resources, individuals can visit Illinois Forms.

The Expense Report details all expenses incurred during a specific period, similar to the expense section of the P&L. It categorizes costs, helping businesses monitor spending and identify areas for cost reduction. This document is essential for maintaining financial discipline and ensuring accuracy in the P&L.

The Profit and Loss form is a key document for understanding a business's financial performance over a specific period. Alongside this form, several other documents can provide additional insights into the financial health of a business. Below is a list of related forms and documents commonly used in conjunction with the Profit and Loss form.

These documents collectively provide a more comprehensive understanding of a business's financial situation. By reviewing them together, stakeholders can make informed decisions regarding operations and strategy.

Understanding the Profit and Loss (P&L) form is essential for evaluating a business's financial health. However, several misconceptions can lead to confusion. Here are seven common misconceptions:

Many believe that the P&L form solely reflects profit. In reality, it also details revenues, expenses, and net income, providing a complete picture of financial performance.

While a positive net income is a good sign, it does not account for cash flow issues or debts. A comprehensive analysis of financial health requires looking beyond just the net income.

These two documents serve different purposes. The P&L focuses on revenues and expenses over a period, while the cash flow statement tracks the actual cash inflows and outflows.

Some expenses may not be included in the P&L, such as capital expenditures. Understanding what is included and excluded is crucial for accurate financial analysis.

This form is vital for businesses of all sizes. Small businesses also need to track their financial performance to make informed decisions.

The P&L should be regularly reviewed and updated to reflect changes in business operations, ensuring that it remains a useful tool for financial management.

While accountants prepare the P&L, business owners and managers should also understand it. Familiarity with this form empowers better decision-making.

By addressing these misconceptions, individuals can gain a clearer understanding of the Profit and Loss form and its importance in managing a business's finances.