Promissory Note Template

Promissory Note Template

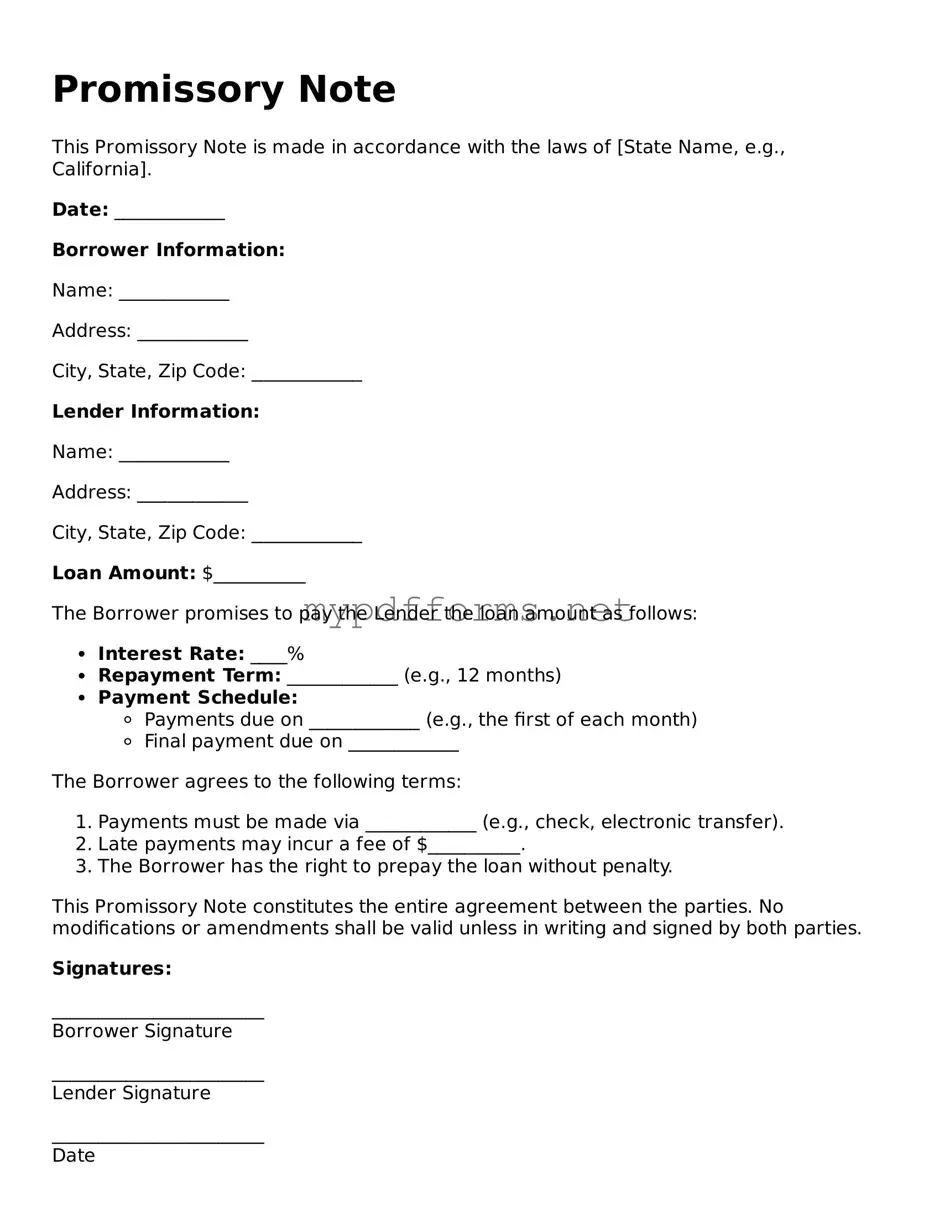

A Promissory Note is a crucial financial document that serves as a written promise to pay a specified amount of money to a designated party at a defined future date or on demand. This form typically includes essential details such as the principal amount, interest rate, repayment schedule, and any applicable fees. It may also outline the consequences of default, ensuring that both the borrower and lender understand their obligations and rights. The simplicity of the Promissory Note makes it a versatile tool for personal loans, business transactions, and real estate financing. Understanding the structure and components of this form can empower individuals and businesses to navigate their financial agreements more effectively, fostering transparency and accountability in lending practices.

When filling out a Promissory Note form, it's important to follow certain guidelines to ensure the document is valid and effective. Here are some key dos and don'ts to consider:

By adhering to these guidelines, you can help ensure that your Promissory Note is clear and enforceable. Take your time, and double-check your work before finalizing the document.

Printable Daily Cash Drawer Count Sheet - Enhances understanding of cash flow dynamics in retail.

The Minnesota Motorcycle Bill of Sale form not only serves as a vital tool for transferring ownership but also ensures that all relevant details about the motorcycle and the parties involved are clearly documented. To help facilitate this process, you can find a free template at https://motorcyclebillofsale.com/free-minnesota-motorcycle-bill-of-sale, making it easier for both buyers and sellers to complete the transaction smoothly.

Erc Forms - The report includes a review of both interior and exterior items in need of attention.

When filling out and using a Promissory Note form, several key points should be considered to ensure clarity and enforceability. Below are essential takeaways:

Following these guidelines can help create a clear and enforceable Promissory Note, minimizing the risk of misunderstandings or legal issues in the future.

Once you have the Promissory Note form in hand, it's time to complete it accurately. This form will need to be filled out with specific information that outlines the terms of the loan agreement. Follow the steps below to ensure you fill it out correctly.

After completing the form, ensure that both parties keep a copy for their records. This document serves as a formal agreement and should be treated with care.

A promissory note is a written promise to pay a specified amount of money to a designated person or entity at a defined time or on demand. It serves as a legal document that outlines the terms of the loan, including the principal amount, interest rate, repayment schedule, and any penalties for late payment.

Individuals and businesses commonly use promissory notes. They are often utilized in personal loans, business loans, or when borrowing money from family or friends. The note provides both the lender and borrower with clear terms regarding the loan agreement.

A well-drafted promissory note should include the following key information:

Yes, a promissory note is a legally binding document. Once signed by both parties, it can be enforced in court if the borrower fails to repay the loan as agreed. This makes it important for both parties to understand the terms before signing.

Yes, a promissory note can be modified if both the borrower and lender agree to the changes. It is advisable to document any modifications in writing to ensure clarity and maintain a record of the updated terms.

If the borrower defaults, the lender may take legal action to recover the owed amount. This could involve filing a lawsuit or seeking a judgment against the borrower. The specific actions taken will depend on the terms outlined in the promissory note and applicable laws.

While it is not strictly necessary to have a lawyer draft a promissory note, consulting one can be beneficial. A legal professional can help ensure that the document complies with state laws and adequately protects the interests of both parties.

Yes, a promissory note can be transferred to another party, a process known as "negotiation." The original lender may sell or assign the note to someone else, who then assumes the rights to collect payments. This transfer typically requires the borrower to be notified.

A loan agreement is a document that outlines the terms of a loan between a lender and a borrower. Like a promissory note, it specifies the amount borrowed, the interest rate, and the repayment schedule. However, a loan agreement often includes additional clauses that address the rights and responsibilities of both parties, collateral requirements, and default conditions. While a promissory note serves primarily as a promise to pay, a loan agreement provides a more comprehensive framework for the transaction.

To ensure a successful transaction, it is crucial to utilize the proper documentation, such as the comprehensive Maryland Trailer Bill of Sale form available online. This document can streamline the transfer process, providing necessary legal protection for both the buyer and seller. For more details, you can visit the Trailer Bill of Sale form page.

A mortgage is another document that shares similarities with a promissory note. In a mortgage, the borrower pledges real estate as collateral for the loan. The promissory note in this case represents the borrower's promise to repay the loan amount, while the mortgage secures the lender's interest in the property. Both documents work in tandem; the mortgage provides the lender with a legal claim to the property if the borrower defaults on the promissory note.

A personal guarantee is a document that an individual signs to assume responsibility for a debt. This is similar to a promissory note because it represents a commitment to pay. In cases where a business takes out a loan, a personal guarantee may be required from the business owner. If the business defaults, the lender can pursue the individual for repayment, just as they would with a promissory note.

An IOU is a simple acknowledgment of a debt. It is less formal than a promissory note but serves a similar purpose by indicating that one party owes money to another. An IOU typically lacks the detailed terms found in a promissory note, such as interest rates and repayment schedules. However, both documents signify a debt obligation and can be used to track informal loans between individuals.

A credit agreement outlines the terms under which credit is extended to a borrower. Similar to a promissory note, it details the amount of credit, interest rates, and repayment terms. Credit agreements are often used in business contexts and can involve revolving credit lines. While a promissory note focuses on a specific loan amount, a credit agreement may cover multiple transactions and provide more flexibility in borrowing.

A bond is a formal debt security issued by corporations or governments. It is similar to a promissory note in that both represent a promise to repay borrowed money. However, bonds are typically sold to investors and may have longer maturities. Unlike a promissory note, which is often a private agreement, bonds are publicly traded and can be bought and sold in the financial markets.

A lease agreement is a document that allows one party to use property owned by another party in exchange for payment. While it primarily pertains to the rental of property, it can resemble a promissory note in that it involves a promise to pay a specified amount over time. Both documents establish a financial obligation, though a lease agreement also includes terms related to the use and maintenance of the property being leased.

A Promissory Note is a crucial document in financial transactions, but it often works in conjunction with other forms. Each of these documents serves a specific purpose, ensuring clarity and protection for all parties involved. Below is a list of commonly used forms alongside the Promissory Note.

Understanding these additional documents can enhance your grasp of the financial landscape surrounding a Promissory Note. Each form plays a vital role in ensuring that all parties are protected and informed throughout the lending process.

Understanding the Promissory Note form is crucial for anyone entering into a loan agreement. However, several misconceptions can lead to confusion. Below is a list of common misunderstandings about this important document.

By addressing these misconceptions, individuals can better navigate the complexities of promissory notes and ensure that their loan agreements are clear and enforceable.