Promissory Note for a Car Template

Promissory Note for a Car Template

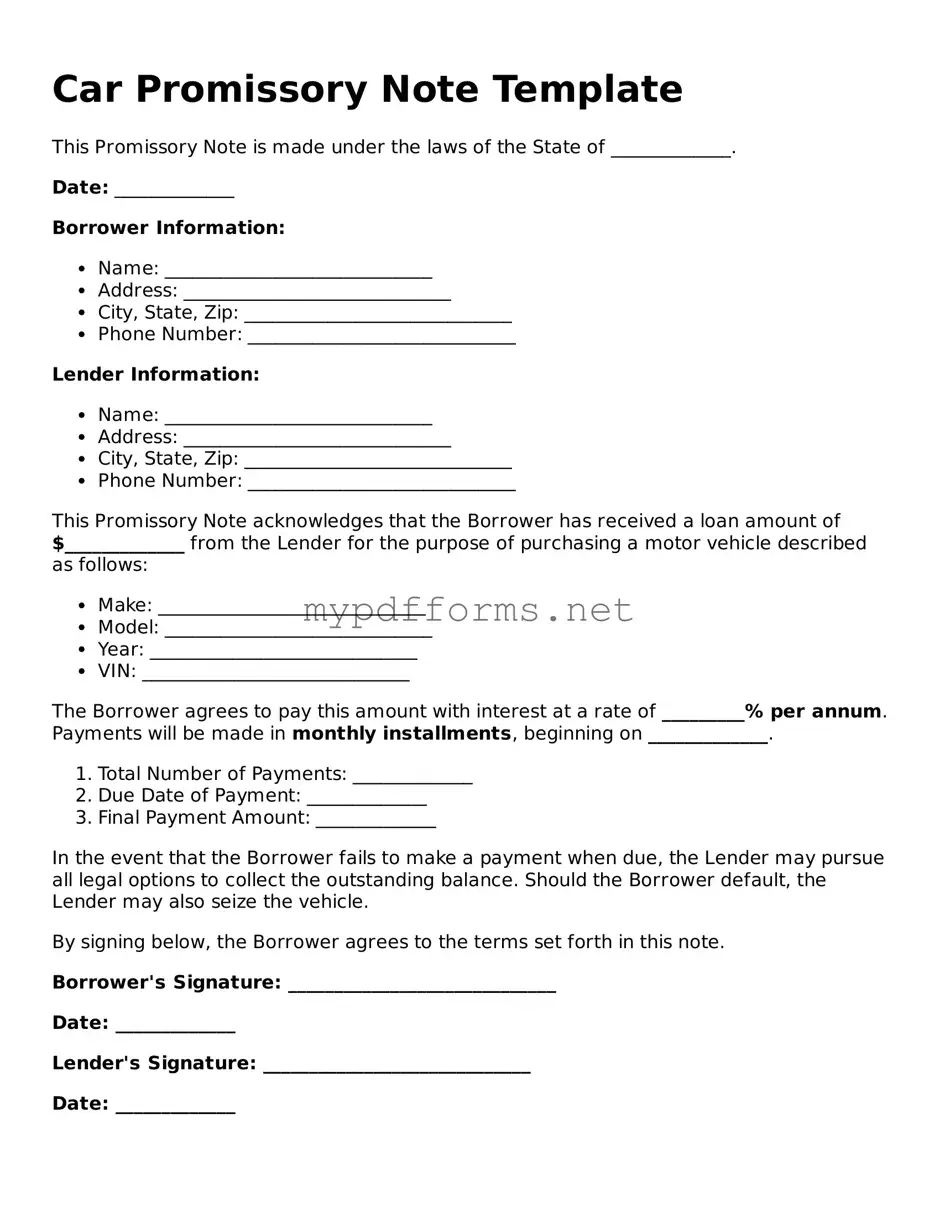

The Promissory Note for a Car serves as a vital document in the process of financing a vehicle purchase. This legally binding agreement outlines the borrower's commitment to repay the loan amount, including any applicable interest, within a specified timeframe. Typically, the form includes essential details such as the names and addresses of both the borrower and lender, the total loan amount, and the interest rate applicable to the loan. Additionally, it specifies the payment schedule, including the frequency of payments and the due dates. Importantly, the document may also contain provisions for late fees and consequences in the event of default. By clearly delineating these terms, the Promissory Note provides both parties with a framework for their financial relationship, ensuring transparency and accountability throughout the duration of the loan. Understanding the nuances of this form can help borrowers navigate their obligations while protecting the lender's interests.

When filling out the Promissory Note for a Car form, it's essential to ensure accuracy and clarity. Here’s a list of things you should and shouldn’t do to avoid potential issues.

Following these guidelines will help ensure that your Promissory Note is filled out correctly and efficiently. Attention to detail is crucial in this process.

Satisfaction and Release Form - This form showcases responsible financial behavior upon completion of payments.

In addition to the essential details provided, it's important to remember that an Alabama Promissory Note form can be easily found online, making it more accessible for those looking to formalize their loan agreements. For more information on this crucial document, visit https://alabamapdfs.com/, where you can access everything needed to proceed with your financially binding agreement.

When you're dealing with a Promissory Note for a Car, understanding the ins and outs of the form can make a big difference. Here are some key takeaways to keep in mind:

By following these key points, you can ensure that your Promissory Note for a Car is clear, fair, and legally sound. Understanding the details can help both the borrower and lender feel secure in their agreement.

After obtaining the Promissory Note for a Car form, you are ready to begin the process of filling it out. This document is essential for outlining the terms of the loan agreement for your vehicle purchase. Carefully follow the steps below to ensure that all necessary information is accurately provided.

Once the form is completed, review it carefully to ensure that all information is correct. It is advisable to keep a copy for your records, as well as to provide one to the other party involved in the transaction. This will help maintain clarity and accountability throughout the loan period.

A Promissory Note for a Car is a written agreement between a borrower and a lender. This document outlines the terms under which the borrower agrees to repay the loan used to purchase a vehicle. It includes details such as the loan amount, interest rate, repayment schedule, and any penalties for late payments.

This form is typically used by individuals who are financing a vehicle purchase through a private lender or seller rather than a traditional financial institution. It is suitable for both buyers and sellers who want to formalize the loan agreement and protect their interests.

To complete the Promissory Note for a Car, the following information is generally required:

If the borrower fails to make payments as agreed, the lender may have the right to take legal action to recover the owed amount. This could include repossessing the vehicle, depending on the terms outlined in the Promissory Note. It is important for both parties to understand their rights and obligations before entering into this agreement.

A car loan agreement is similar to a promissory note in that both documents outline the terms of a loan for purchasing a vehicle. A car loan agreement typically includes details such as the loan amount, interest rate, repayment schedule, and any collateral involved. While a promissory note serves as a promise to repay the borrowed amount, the car loan agreement provides a more comprehensive overview of the lender's and borrower's rights and responsibilities. Both documents are legally binding and aim to protect the interests of both parties involved in the transaction.

Understanding the essentials of a comprehensive Promissory Note template can significantly enhance your financial dealings. This document not only outlines the specifics of the repayment terms but also safeguards the interests of both the lender and the borrower throughout the loan process.

A lease agreement for a vehicle shares similarities with a promissory note as it also involves a financial commitment related to the use of a car. In a lease agreement, the lessee agrees to make regular payments for the right to use the vehicle for a specified period. Like a promissory note, the lease outlines the payment terms, including the amount and due dates. However, unlike a promissory note, a lease does not involve ownership transfer at the end of the term, making it a distinct but related financial document.

A mortgage note is another document akin to a promissory note, as it represents a borrower's promise to repay a loan, typically for real estate. While the promissory note for a car focuses on vehicle financing, a mortgage note details the terms of a home loan, including the loan amount, interest rate, and repayment schedule. Both documents serve as legal evidence of the debt and are enforceable in court. They also establish the consequences of default, ensuring that the lender has recourse if the borrower fails to meet their obligations.

An installment agreement can also be compared to a promissory note, as it involves a borrower agreeing to repay a loan in regular payments over time. This type of agreement is often used for various types of purchases, including cars, furniture, or appliances. The installment agreement outlines the total amount financed, the payment schedule, and any applicable interest rates. Like a promissory note, it serves as a commitment from the borrower to fulfill their payment obligations, providing both parties with a clear understanding of the terms involved.

When financing a car purchase, several important documents accompany the Promissory Note. Each document plays a vital role in ensuring clarity and legal compliance throughout the transaction. Here are four key forms often used alongside the Promissory Note:

Each of these documents works together with the Promissory Note to create a clear and comprehensive framework for the car financing process. Understanding these forms can help facilitate a smoother transaction and ensure all parties are informed and protected.

When dealing with the Promissory Note for a Car form, several misconceptions can lead to confusion. Here are six common misunderstandings:

Understanding these misconceptions can help individuals navigate the process of using a Promissory Note for a Car more effectively.