Attorney-Verified Loan Agreement Document for Texas

Attorney-Verified Loan Agreement Document for Texas

In the realm of financial transactions, understanding the Texas Loan Agreement form is crucial for both lenders and borrowers. This document serves as a legally binding contract that outlines the terms of a loan, ensuring that all parties are on the same page. It typically includes essential elements such as the loan amount, interest rate, repayment schedule, and any applicable fees. Additionally, it details the rights and responsibilities of each party, providing clarity on what happens in the event of default. With specific provisions tailored to Texas law, this form addresses unique state requirements, making it vital for anyone involved in lending or borrowing within the state. As you navigate through this agreement, it's important to pay close attention to the fine print, as it can significantly impact your financial future. Understanding these components can empower you to make informed decisions and foster a smooth lending process.

When filling out the Texas Loan Agreement form, attention to detail is crucial. Here are seven essential dos and don'ts to guide you through the process:

Promissory Note Florida Pdf - Includes stipulations regarding assignment of the loan rights.

Promissory Note Template New York - Each key term within the agreement should be clearly defined to avoid confusion.

Understanding the Illinois 20A form is essential for anyone facing an eviction situation in Will County. This legal document notifies defendants about pending forcible entry actions and signals the initial steps of the eviction process. To effectively manage such proceedings, one must be well-informed about the necessary responses and requirements. For additional assistance, you can refer to the Illinois Forms, which provide detailed information on filling out the form and navigating the subsequent steps.

Free Promissory Note Template California - The agreement provides documentation of the loan for future reference.

When filling out and using the Texas Loan Agreement form, there are several important points to keep in mind. These takeaways will help ensure that the process is smooth and that both parties are protected.

By keeping these key takeaways in mind, both lenders and borrowers can navigate the loan agreement process more effectively and with greater confidence.

Filling out the Texas Loan Agreement form is a straightforward process that requires attention to detail. Ensure you have all necessary information at hand before you begin. This will help streamline the completion of the document and ensure accuracy.

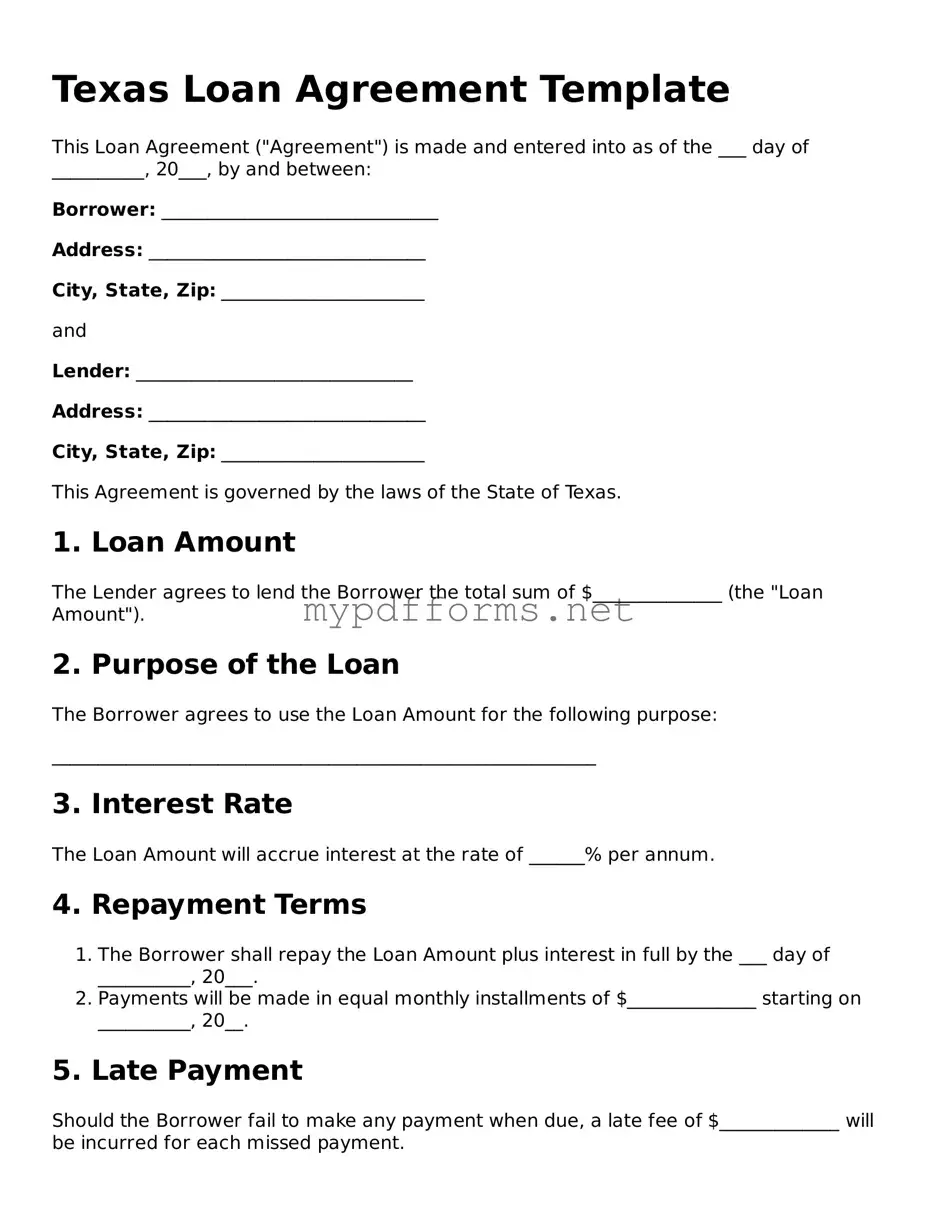

A Texas Loan Agreement is a legal document that outlines the terms and conditions of a loan between a lender and a borrower in the state of Texas. It specifies the amount borrowed, the interest rate, repayment schedule, and any collateral involved. This agreement protects both parties by clearly defining their rights and responsibilities.

Key components of a Texas Loan Agreement typically include:

Yes, a Texas Loan Agreement is legally binding once both parties sign it. This means that both the lender and the borrower are obligated to adhere to the terms outlined in the agreement. If either party fails to comply, the other party may seek legal remedies.

While it is not legally required to have a lawyer draft a Texas Loan Agreement, it is advisable. A lawyer can ensure that the agreement complies with Texas laws and addresses any specific concerns or complexities of your situation. This can help prevent disputes in the future.

Yes, a Texas Loan Agreement can be modified after it is signed, but both parties must agree to the changes. It is best to document any modifications in writing and have both parties sign the amended agreement. This helps maintain clarity and avoids misunderstandings.

If a borrower defaults on a Texas Loan Agreement, the lender has several options. These may include charging late fees, accelerating the loan (demanding full payment), or pursuing legal action to recover the owed amount. The specific consequences should be outlined in the agreement itself.

The Texas Loan Agreement form shares similarities with a Promissory Note. Both documents outline the terms under which a borrower agrees to repay a loan. A Promissory Note specifically details the borrower's promise to pay a specified amount, including interest, by a certain date. This document can stand alone or be part of a larger agreement, such as a Loan Agreement, which may include additional provisions regarding collateral or default. Both documents serve to protect the lender's interests while providing clarity to the borrower regarding their obligations.

Another document akin to the Texas Loan Agreement is the Security Agreement. This document is often used in conjunction with a loan agreement when collateral is involved. A Security Agreement details the assets that will secure the loan, providing the lender with a claim to those assets if the borrower defaults. Like the Loan Agreement, it outlines the terms of the loan but focuses more on the collateral aspect, ensuring that both parties understand the implications of securing the loan with specific assets.

The Texas Loan Agreement is also similar to a Mortgage Agreement. Both documents involve borrowing money, typically for the purchase of real estate. A Mortgage Agreement specifically refers to a loan secured by real property, while a Loan Agreement can apply to various types of loans. Both documents require the borrower to adhere to repayment terms and may include provisions for foreclosure in the event of default. The Mortgage Agreement is often more detailed in terms of property rights and obligations.

A Credit Agreement is another document that parallels the Texas Loan Agreement. This type of agreement is typically used in business financing. It outlines the terms under which a lender extends credit to a borrower, including interest rates, repayment schedules, and covenants that the borrower must adhere to. While the Texas Loan Agreement may focus on a single loan, a Credit Agreement often encompasses a revolving line of credit, providing more flexibility to the borrower.

In the realm of vehicle transactions, having the appropriate documentation is crucial for both parties involved. The Florida Motor Vehicle Bill of Sale serves as an indispensable tool in this process, providing a structured format to ensure the transfer of ownership is clear and legally sound. For more information on this essential document, you can visit https://floridapdfform.com, which offers a comprehensive guide and template for creating your Bill of Sale.

The Texas Loan Agreement can also be compared to an Installment Agreement. This document outlines a payment plan for a loan, breaking down the total amount into smaller, manageable payments over time. Like the Loan Agreement, it specifies the interest rate and repayment schedule. The key difference lies in the payment structure; an Installment Agreement typically involves regular payments of principal and interest, while a Loan Agreement may allow for various repayment options.

A Lease Agreement shares similarities with the Texas Loan Agreement, particularly when it comes to financing options for purchasing equipment or property. Both documents establish terms for payment and use of the asset. In a Lease Agreement, the borrower (lessee) pays to use an asset for a specified period, while in a Loan Agreement, the borrower owns the asset outright after repayment. Both agreements protect the lender's interests and outline the consequences of default.

Lastly, the Texas Loan Agreement is similar to a Forbearance Agreement. This document is used when a borrower is struggling to make payments. A Forbearance Agreement allows the borrower to temporarily pause or reduce payments without facing immediate penalties. While the Texas Loan Agreement establishes the original terms of the loan, the Forbearance Agreement modifies those terms to accommodate the borrower's current financial situation, ensuring both parties have a clear understanding of the new terms.

When entering into a loan agreement in Texas, several other documents often accompany the Texas Loan Agreement form. These documents help clarify the terms of the loan and protect the interests of both the lender and the borrower. Below is a list of commonly used forms and documents that you may encounter.

These documents work together to create a clear understanding of the loan terms and responsibilities. Having them organized and accessible can make the loan process smoother for everyone involved.

Understanding the Texas Loan Agreement form is crucial for anyone involved in lending or borrowing money in the state. However, several misconceptions can lead to confusion and potential legal issues. Here are seven common misconceptions:

Awareness of these misconceptions can help individuals navigate the complexities of loan agreements more effectively. Always seek professional advice when in doubt.