Attorney-Verified Promissory Note Document for Texas

Attorney-Verified Promissory Note Document for Texas

In the realm of personal and business finance, a Texas Promissory Note plays a crucial role in facilitating loans and establishing clear terms between lenders and borrowers. This straightforward yet powerful document outlines the specifics of the loan agreement, including the principal amount, interest rate, repayment schedule, and any applicable fees. By providing a written record, the note helps protect both parties and ensures that everyone understands their rights and responsibilities. Furthermore, it may include provisions for late payments, default scenarios, and the legal recourse available in case of non-compliance. Understanding the nuances of this form is essential for anyone considering borrowing or lending money in Texas, as it not only serves as a binding contract but also fosters trust and transparency in financial transactions.

When filling out the Texas Promissory Note form, consider the following guidelines to ensure accuracy and compliance.

Free Promissory Note Template California - The note is a crucial document in the chain of evidence if disputes occur.

Free Promissory Note Template Florida - A promissory note is a written promise to pay a specified amount of money to someone in the future.

When engaging in a motorcycle transaction in Illinois, it is vital to utilize the appropriate legal documentation to ensure a smooth process. The Illinois Motorcycle Bill of Sale serves this purpose effectively, providing a comprehensive record of the sale. For individuals looking to secure this essential document, further information can be found at https://motorcyclebillofsale.com/free-illinois-motorcycle-bill-of-sale.

New York Promissory Note - It serves as a legal contract between a borrower and a lender.

Ensure that all parties involved are clearly identified. This includes the borrower and the lender. Their names and contact information should be accurate to avoid any confusion.

Specify the loan amount. Clearly state the total amount being borrowed to prevent any misunderstandings later on.

Include the interest rate. If applicable, outline the interest rate for the loan. This detail is crucial as it affects the total amount to be repaid.

Define the repayment terms. Clearly outline when payments are due and the method of payment. This helps both parties understand their obligations.

Sign and date the document. Both the borrower and lender must sign the Promissory Note for it to be legally binding. Ensure that the date of signing is also included.

Once you have your Texas Promissory Note form ready, it's time to fill it out accurately. This step is crucial as it sets the foundation for your agreement. Make sure to have all necessary information at hand before you start.

After completing the form, review it carefully to ensure all information is accurate. Once confirmed, both parties should keep a signed copy for their records. This helps to avoid misunderstandings in the future.

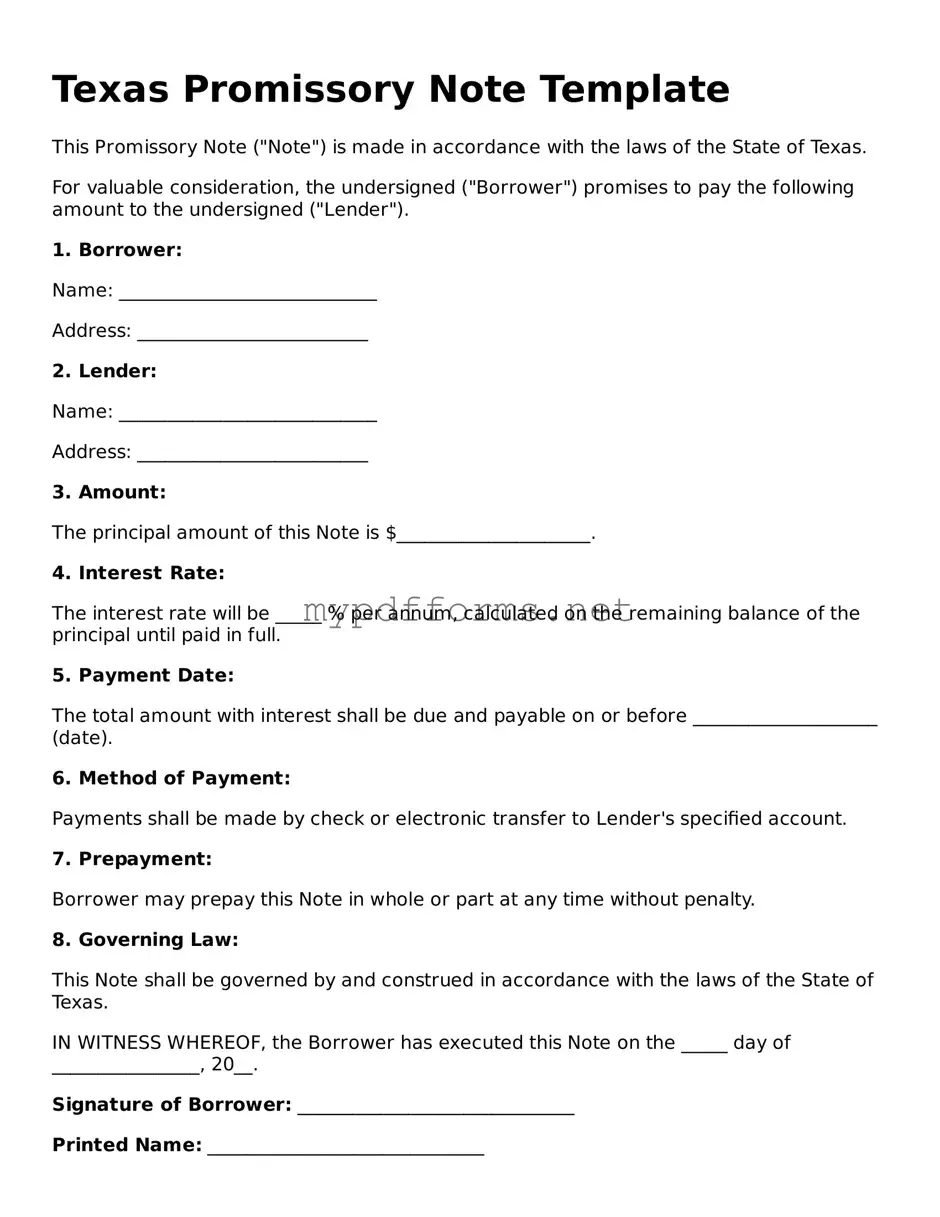

A Texas Promissory Note is a legal document that outlines a borrower's promise to repay a specific amount of money to a lender under agreed-upon terms. This document serves as a formal acknowledgment of the debt and includes details such as the loan amount, interest rate, repayment schedule, and any applicable penalties for late payments.

Any individual or business in Texas can use a Promissory Note. Whether you are lending money to a friend, financing a small business, or entering into a more formal loan agreement, this document provides clarity and legal protection for both parties involved.

A comprehensive Texas Promissory Note typically includes the following information:

Yes, a properly executed Texas Promissory Note is legally binding. Once both parties sign the document, it creates a contractual obligation. If the borrower fails to repay the loan as agreed, the lender has the right to take legal action to recover the owed amount.

While it is not mandatory to hire a lawyer to draft a Texas Promissory Note, doing so can be beneficial. A legal professional can ensure that the document complies with Texas laws and adequately protects your interests. For simple loans, templates are available, but personalized advice can help avoid potential pitfalls.

Yes, a Texas Promissory Note can be modified if both parties agree to the changes. It is advisable to document any modifications in writing and have both parties sign the updated agreement. This helps prevent misunderstandings and ensures that the new terms are enforceable.

The Texas Promissory Note is similar to a Loan Agreement, which outlines the terms and conditions of a loan between a lender and a borrower. Both documents specify the principal amount, interest rate, repayment schedule, and any penalties for late payments. However, a Loan Agreement typically includes more detailed provisions regarding the rights and responsibilities of both parties, as well as collateral requirements, if applicable. This makes the Loan Agreement a more comprehensive document compared to the straightforward nature of a Promissory Note.

A Security Agreement also shares similarities with a Texas Promissory Note. Both documents involve the borrowing of funds, but a Security Agreement specifically grants the lender a security interest in the borrower's property as collateral for the loan. While the Promissory Note focuses on the promise to repay the borrowed amount, the Security Agreement details the collateral and the lender's rights in case of default. This adds an additional layer of protection for the lender.

The Texas Promissory Note is akin to an IOU, which is a simple acknowledgment of a debt. An IOU states that one party owes a specific amount to another party, but it generally lacks the detailed terms found in a Promissory Note. While an IOU can serve as a basic record of a debt, it does not usually include information about interest rates, repayment schedules, or legal recourse, making it less formal and less enforceable in court.

A Loan Modification Agreement is another document that bears resemblance to the Texas Promissory Note. This agreement is used when the original loan terms need to be changed, often due to financial hardship. Both documents involve the original loan, but the Loan Modification Agreement specifically alters the terms, such as the interest rate or repayment period. In contrast, the Promissory Note remains static unless explicitly modified.

When navigating through the various financing agreements and contracts, it's essential for businesses to also be aware of the statutory requirements they must meet, such as those associated with unclaimed property. To assist in this process, the Illinois Forms are available, providing necessary documentation to report unclaimed assets in compliance with state laws, ensuring that businesses remain informed and compliant while managing their financial obligations.

A Lease Agreement can also be compared to a Texas Promissory Note in terms of payment obligations. Both documents establish a financial commitment, but a Lease Agreement specifically pertains to the rental of property. It outlines the terms of occupancy, including rent payments, duration of the lease, and maintenance responsibilities. While a Promissory Note focuses on a loan, a Lease Agreement is centered on the terms of use and payment for the property.

The Texas Promissory Note is similar to a Personal Guarantee, which is often used in business transactions. A Personal Guarantee involves an individual agreeing to be responsible for a debt if the primary borrower defaults. Both documents establish a financial obligation, but a Personal Guarantee adds a personal liability component, ensuring that the lender has recourse against the individual, not just the business entity.

Lastly, a Credit Agreement resembles the Texas Promissory Note in that it details the terms of borrowing funds. A Credit Agreement typically applies to a line of credit or revolving credit account, outlining the borrowing limits, interest rates, and repayment terms. While both documents create a legal obligation to repay borrowed funds, a Credit Agreement often includes more complex terms regarding the use of credit and repayment flexibility, which may not be present in a standard Promissory Note.

When engaging in a loan agreement in Texas, the Promissory Note is a crucial document. However, it often works in conjunction with other forms and documents that help clarify the terms and provide additional protections for all parties involved. Below is a list of commonly used forms that complement the Texas Promissory Note.

Each of these documents plays a vital role in the lending process, providing clarity, security, and legal backing for both lenders and borrowers. Understanding these forms can empower individuals to navigate financial agreements more effectively.

There are several misconceptions about the Texas Promissory Note form that can lead to confusion. Understanding these can help ensure that the document is used correctly. Here are eight common misconceptions:

Understanding these misconceptions can help individuals navigate the use of promissory notes more effectively. Always consider consulting with a professional if there are any questions or concerns.